What is a Spread?

In finance, the spread is the difference between two similar measurements, such as stock prices, yields (the percentage that you stand to earn on an investment), or interest rates.

🤔 Understanding a spread

In finance, the term “spread” can have different meanings, depending on the context. But generally, the spread is the gap between two measurements (e.g., rates, yields, or prices). Spreads can vary depending on what you are trading. For example, a stock’s bid-ask spread is the difference between a stock’s bid and ask price. With bonds, the spread could compare yield (how much you stand to earn on an investment).

Take the fictitious company Mikey’s Mustard Corp. Say that the current bid price (what traders are willing to buy it for) is $10.50, and say the current ask price (what traders are willing to sell it for) is $10.75. The bid-ask spread for Mikey’s Mustard Corp. is the difference between these prices, or $0.25.

Takeaway

A spread is like standing two kids back-to-back to see who’s taller...

By doing this you will get a sense of one’s height relative to the other, just as you may want to compare the bid/ask prices of a stock or the attributes of a given bond. And, as kids may grow at different rates, the spread — the difference between two rates, yields, or prices — may change over time.

New customers need to sign up, get approved, and link their bank account. The cash value of the stock rewards may not be withdrawn for 30 days after the reward is claimed. Stock rewards not claimed within 60 days may expire. See full terms and conditions at rbnhd.co/freestock. Securities trading is offered through Robinhood Financial LLC.

What are the different types of spreads?

There are different kinds of spreads across different trading markets. Some of the most common spreads discussed in finance are:

- Bid-ask spread

- Yield spread

- Option-adjusted spread

- Z-spread

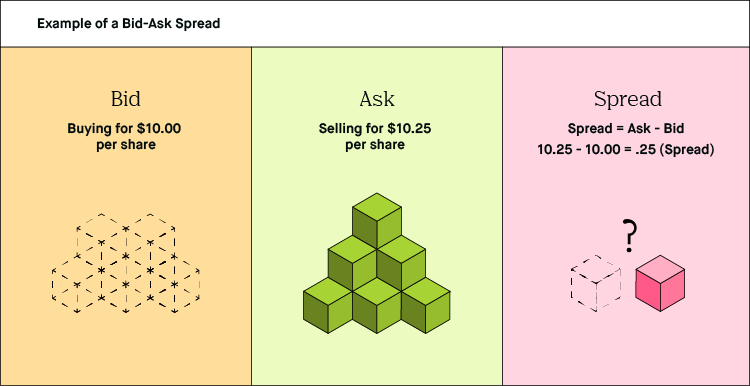

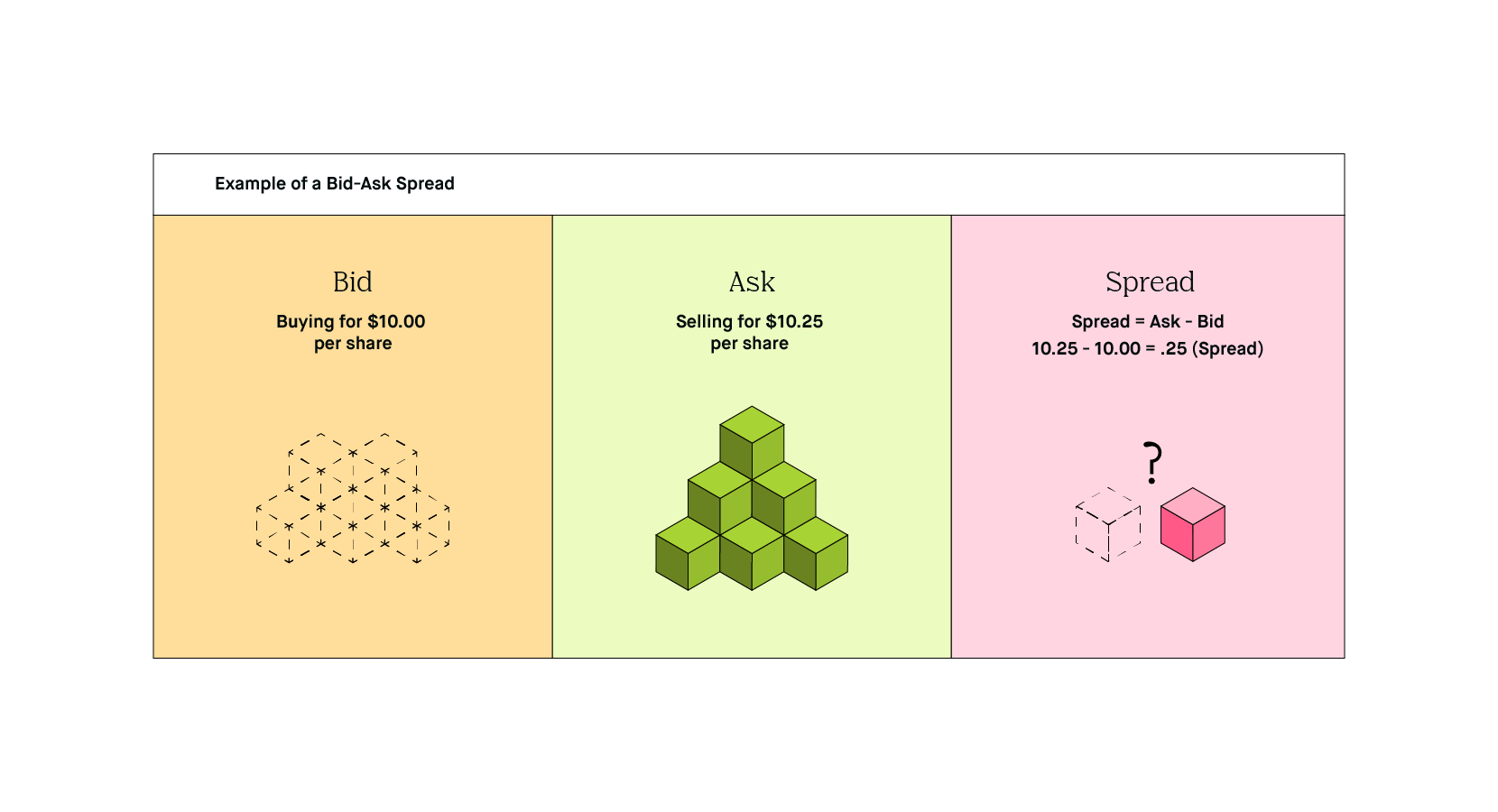

Bid-Ask Spread

The bid price is the highest price that a buyer is willing to pay for a security. On the opposite end, the ask price is the lowest price a seller is willing to accept for a security. The difference between the bid price and the ask price is called the bid-ask spread.

The stock market, futures contracts, options, and foreign exchange currencies all have bid-ask spreads. Investors can use bid-ask spreads to measure a stock’s liquidity (how quickly you can buy and sell the stock) as larger spreads typically indicate less liquid assets.

Yield Spread

A yield spread is also known as a credit spread for bonds. It measures the difference between two bonds that have the same maturity.

Yield spreads help investors weigh different qualities of two debt products. Let’s say you are comparing a U.S. Treasury bond with a corporate bond. As of November 28, 2019, the 10-year U.S. Treasury bond yields 1.75%. On the other hand, let’s say the 10-year corporate bond of the fictitious company Jenn’s Jams yields 5.00%. The yield spread would be 5.00% - 1.75% = 3.25%.

However, corporate bonds are riskier than government bonds. So, an investor would consider both the risk and the yield spread when choosing which bond to invest in.

Option-Adjusted Spread

An option-adjusted spread (OAS) is the difference between the price of a security with an embedded option (an option connected to a security that affects its redemption) and the cost of that security without the option. An embedded option can negatively affect the value of a security. For example, an embedded option may give the bond issuer the right to pay off their debt early, before the bond can reach maturity. If this happens, the investor may lose out on interest payments, which drops the overall value of the investment.

The option-adjusted spread separates the security from the embedded option. It helps investors evaluate whether the security is worthwhile at a given price.

If the security’s cash flow is not affected by future interest rates, then the option-adjusted spread is the same as the zero-volatility spread.

Z-Spread

Z-spread (zero-volatility spread) is also known as the yield curve spread. It helps investors calculate a bond’s current value plus its cash flow at particular points on the Treasury yield curve (a graph that shows how much money you’ll get back on a Treasury fixed-income security).

The Z-spread tells the investor the spread over the entire Treasury yield curve instead of at one point in time.

What is a spread risk?

There are two types of spread risks.

True Spread Risk

The true spread risk is the probability that an investment loses market value. A loss in market value may happen because the bond issuer makes financial mistakes that impact the bond’s credit rating (the bond’s grade that measures its risk of default). These credit ratings are issued by agencies, such as Moody’s, Standard & Poor’s, and Fitch Ratings.

Generally, as the credit rating of an existing bond goes down, the value of the bond goes down, too.

Credit Spread Risk

A credit spread, or yield spread, helps compare the yields of two bonds that have different credit ratings, but the same due date.

Lower-quality bonds have a higher risk that the bond issuer will default or fail to pay you back. The upside is that riskier bonds typically come with higher yields (the percentage of interest that you receive on your investment) because they need to compensate the investor for the increased risk.

On the other hand, high-quality bonds have a higher credit rating because they have a lower chance of default. In other words, it is a safer investment that more people would likely be interested in. As a result, the lower the default risk, the lower the yield.

The spread risk indicates if the risk that the yield spread (the difference in potential profit) is not high enough to justify investing in the riskier bond.

How do you make a spread trade?

A spread trade is also known as a relative value trade. This investment strategy is where a trader buys one security while selling a related security at the same time. The two opposing trades ideally produce a spread (a net trade with a positive value).

Here are a few spread trading strategies.

Pairs Trading Strategy

Pairs trading is also known as “statistical arbitrage.” This strategy tries to have zero net risk (market neutral) by hedging the market.

With the pairs trading strategy, you would use computer models and analysis to buy and sell two highly correlated securities (securities that tend to move together). The computer program analyzes how closely correlated two securities have been in the past. It then tries to find a temporary price imbalance between the two related securities (when the two correlated stocks are temporarily out of sync). The trader capitalizes on this imbalance and hopes to make a profit when the prices reconverge (mean reversion).

All investments carry risk. No one can predict stock or market movements.

Convertible Arbitrage Strategy

A convertible security is a type of security that can change into another form. For example, a convertible preferred stock can turn into a company’s common stock.

The convertible arbitrage strategy is where a trader buys or sells a convertible security and the other security (i.e., the company’s common stock) at the same time to profit off a price difference. The trader hopes to take advantage of the price imbalance between these two securities until they reconverge.

All investments carry risk. No one can predict stock or market movements.

Fixed-Income Arbitrage Strategy

The fixed-income arbitrage strategy takes advantage of temporary price differences in bonds and other interest rate securities. An investor may try to sell an overpriced security while buying an underpriced related security. An investor is attempting to profit from these unexpected price differences when the price gap closes.

All investments carry risk. No one can predict stock or market movements.

Spread Trading Risks

Although a market-neutral strategy with zero net risk sounds appealing, spread trading is not bulletproof — It can be risky.

First, an investor needs to know how to identify two highly correlated pairs of securities. That means you’ll need to know how to use and read the computer model and algorithm to find your pair. Second, timing is essential. Your pair needs to be liquid (how fast you can buy and sell the security) so that you can act when the price gap disappears. Finally, there is no guarantee that the prices will reconverge, or it could take a long time for the costs to correlate again.

All investments carry risk. No one can predict stock or market movements. Always consider investment objectives.

New customers need to sign up, get approved, and link their bank account. The cash value of the stock rewards may not be withdrawn for 30 days after the reward is claimed. Stock rewards not claimed within 60 days may expire. See full terms and conditions at rbnhd.co/freestock. Securities trading is offered through Robinhood Financial LLC.