What is a Credit Default Swap?

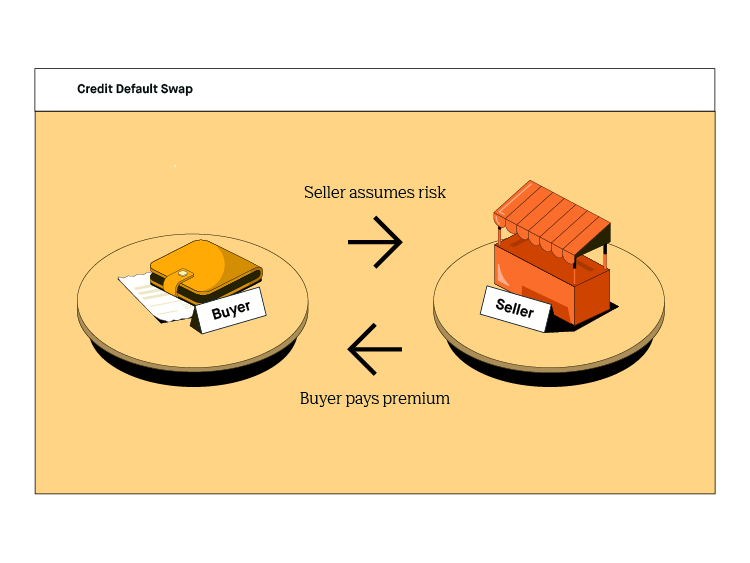

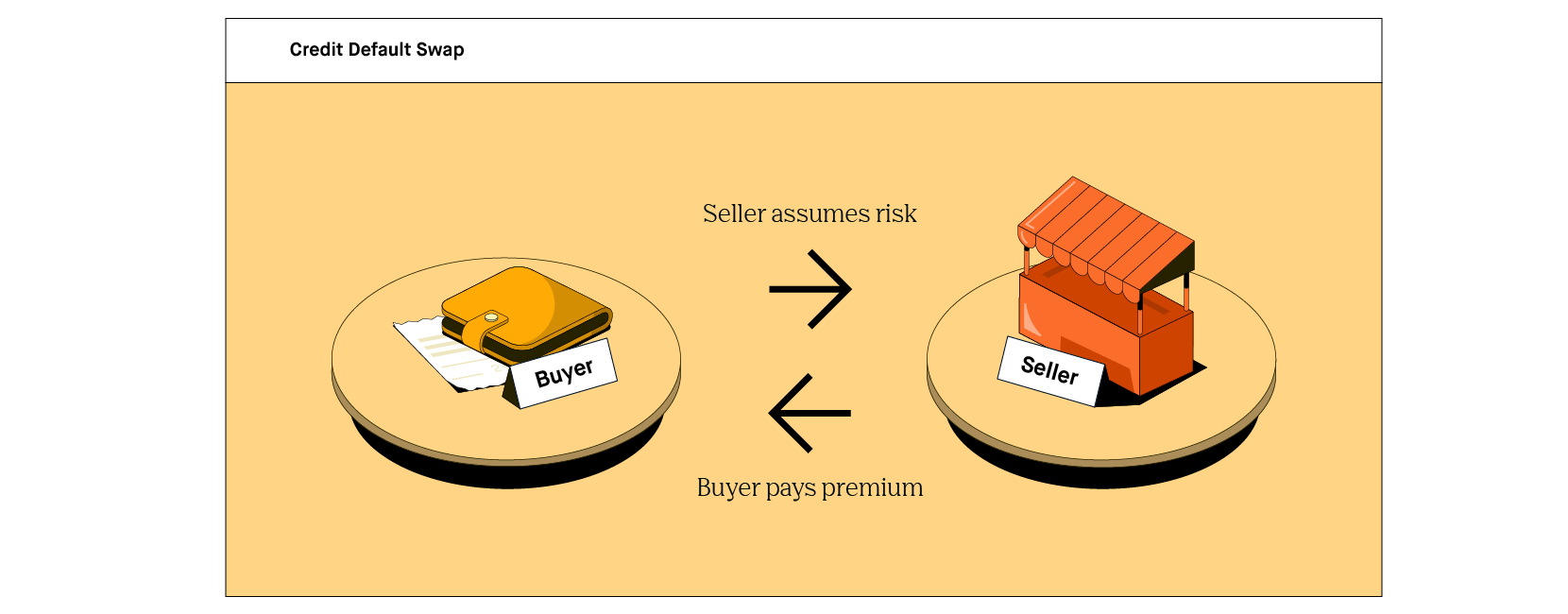

A credit default swap is a financial contract involving three parties, where the seller of the contract pays the buyer of the contract if someone who owes them money stops making payments on that debt.

🤔 Understanding a credit default swap

When a creditor lends money to a borrower, there is always a risk that the borrower won’t pay the money back, leaving the creditor without the income they expect, and sometimes even without the money that was originally loaned. A credit default swap, or CDS, protects creditors from this risk by paying them in the event that a borrower stops paying, or defaults. When a person or entity defaults on a loan, the seller of the CDS pays the buyer an agreed-on amount. In exchange for this assurance, the buyer pays the seller a premium, an ongoing fee for the duration of the contract.

To understand how credit default swaps work, you only have to look at their origins: a real-world example that involves two well-known companies.

In 1994, J.P. Morgan gave Exxon a $4.8B loan to cover up to $5B in damages stemming from the Exxon Valdez spill. The bank then transferred the credit risk (i.e. the obligation to pay if the loan went into default) to the European Bank of Reconstruction and Development (‘EBRD’).

As part of the deal, J.P. Morgan agreed to pay a fee to the EBRD. In turn, the EBRD promised to make a payout if Exxon defaulted. Just like that, the modern credit default swap was born.

Takeaway

A credit default swap is like insurance for debt...

Everyone who loans large amounts of money faces the possibility that they may not be paid what they’re owed. ” To keep themselves from stressing about that problem too much, lenders may turn to credit default swaps. By guaranteeing payment to a lender when a borrower defaults, credit default swaps help manage the risk of lending money, sort of like insurance. (But not exactly like it. More on that in a minute.)

New customers need to sign up, get approved, and link their bank account. The cash value of the stock rewards may not be withdrawn for 30 days after the reward is claimed. Stock rewards not claimed within 60 days may expire. See full terms and conditions at rbnhd.co/freestock. Securities trading is offered through Robinhood Financial LLC.

- How do credit default swaps work?

- How did credit default swaps contribute to the 2008 financial crisis?

- What are the pros of credit default swaps?

- What are the cons of credit default swaps?

- What is a CDS price (spread), and how is it calculated?

- What is a sovereign CDS?

- What is a CDS index?

- Credit default swaps vs. insurance

How do credit default swaps work?

A credit default swap is a derivative, a financial contract between two parties based on the value of an asset, or something one of them owns. But credit default swaps have several unique features that make them different from other derivatives:

- The buyer of a credit default swap typically makes periodic payments to the seller until the maturity date, meaning the end of the contract, or until a credit event is triggered. If a default or another specified credit event occurs on the underlying debt, not only does the seller of the CDS compensate the buyer, but he or she also takes ownership of the loan.

- Sometimes a CDS can be settled by cash, instead, which means that the buyer receives the difference between the par value, or the amount paid back at maturity, and the current value.

How did credit default swaps contribute to the 2008 financial crisis?

Like most other derivatives, credit default swaps can be used by investors who don’t own the asset but want to profit by taking a position in it (or against it). This is called a naked credit default swap. With a naked CDS, you don’t have to own the debt to buy a contract. This policy leaves speculators free to bet on credit events they have no stake in, guessing that a particular party might default on a loan—or not. For example, you could have a trader at Goldman Sachs betting on a CDS that covers $500 million worth of debt issued by Bank of America. This practice has led some critics to call the credit default swap market a “casino” and became a significant point of contention during the late 2000s financial crisis.

Whether or not the CDS market is Caesar’s Palace 2.0, one thing is certain; it contributed to the 2008 financial crisis in a big way.

Before the crisis, there was about $45 trillion worth of debt covered by credit default swaps. As more and more borrowers defaulted on their loans, sellers found themselves unable to fund the payouts they owed to buyers. By the end of the crisis, the total amount of debt covered by credit default swaps had shrunk to $26.3 trillion.

The effect of this can be illustrated by looking at the example of the Lehman Brothers Investment Bank. Lehman Brothers had $400 billion worth of debt covered by credit default swaps, but its insurer, American Insurance Group (AIG), couldn’t deliver the payouts when they were due. The end result was that Lehman Brothers absorbed the cost of the defaults themselves, and ended up declaring bankruptcy.

What are the pros of credit default swaps?

Despite their tattered reputation, credit default swaps have big upsides for lenders.

Debt, including bonds and mortgages, always comes with some risk. In general, the longer the amount of time until the debt is repaid, the greater the risk. Although lenders accept the risk of default every time they issue a loan, it’s natural that they would want to protect themselves against it.

Credit default swaps offer that protection. In exchange for a small recurring premium, the buyer earns the right to compensation should a borrower default on their debt.

What are the cons of credit default swaps?

Most of the cons of credit default swaps come in the form of risk. Both the buyer and the seller of a CDS face certain risks that could leave them without the income or protection they expected.

The most significant risk of credit default swaps is the seller of the CDS defaulting at the same time as the borrower of the underlying debt. If that occurs, then the buyer is left without a payment on either their loan or the CDS built on that loan. In this situation, the buyer loses money both from payment on the loan and whatever they’ve paid out to the seller in premiums.

A related risk comes from a major downturn in the overall credit market. If a downturn like this happens, defaults are likely to rise, leading to a surge in credit default swaps having to be exercised, or paid off. If a single seller has written many credit default swaps in such a situation, then they likely won’t be able to make the payments they owe to all their buyers. This is what happened during the 2008 crisis.

Credit default swaps also pose risks to sellers. Because the payout usually exceeds the premium the seller collects, the seller stands to lose money if the borrower defaults. Additionally, the seller could lose premiums if the CDS contract were canceled before maturity, or if the buyer stopped being able to pay the premiums they owed.

What is a CDS price (spread), and how is it calculated?

If you’re going to spend money to protect against the risk of loaning money, you need to know the cost of that protection. This is where the concept of a CDS spread comes into play.

A CDS spread is the annual total cost of premiums the buyer must pay to the seller over the life of the contract, expressed in basis points, or a hundredth of a percent (0.01%). The spread is calculated using the size of the debt and the total cost of the premiums over the length of the contact. For example, if a seller charges a $50,000 for coverage on $10 million worth of bonds, then the spread is 50 basis points. Knowing the CDS spread helps potential buyers decide if a CDS is a smart investment.

What is a sovereign CDS?

In addition to seeking protection on corporate debt, or debts owed by companies, investors may be interested in a CDS that covers government, or “sovereign,” debt.

A sovereign credit default swap operates mostly like any other CDS. One difference between sovereign and corporate CDS contracts is that sovereign contracts have certain credit events that don’t apply to corporations. For example, a payout on a sovereign CDS may be triggered by a moratorium (a temporary suspension of payments). The reason for this is that defaults on sovereign debt are rare, so investors seek protection for different credit risks.

What is a CDS index?

A credit default swap index is a derivative based on a ‘basket’ of credit default swaps (i.e., a number of credit default swaps grouped together). CDS indices are generally less risky than individual swaps because they include a variety of many different securities. Indices are also usually easier to convert to cash (or “more liquid”) than individual CDS contracts.

Credit default swaps vs. insurance

Credit default swaps are often compared to insurance,’ (Hey, we did it, too.) They do have a lot in common, including premium payments and compensation triggered by negative events. However, a credit default swap is not an insurance contract. Here’s how they’re different:

- The buyer of a credit default swap does not need to make a ‘claim’ to be compensated. If the borrower defaults, compensation happens automatically.

- The credit default swap market is far less regulated than the insurance market.

- Insurance providers are required to keep enough money in the bank to cover claims, but swap sellers are not required to do the same. That makes credit default swaps much riskier than insurance for buyers.

- Insurance buyers have to disclose all known risk factors, like pre-existing medical conditions, to the seller. CDS buyers are not obligated to do anything like that, which also increases the risk to the seller.

- An insurance policy can usually be canceled easily and cheaply; canceling derivatives, including swaps, can be expensive. You’ll need to pay to back out of a CDS contract.

New customers need to sign up, get approved, and link their bank account. The cash value of the stock rewards may not be withdrawn for 30 days after the reward is claimed. Stock rewards not claimed within 60 days may expire. See full terms and conditions at rbnhd.co/freestock. Securities trading is offered through Robinhood Financial LLC.