What is Debt?

Debt is money that one person or entity owes to another.

🤔 Understanding debt

People and companies often need money they don’t have. If they borrow that money, the amount they owe back is known as debt. Debt is usually paid back with interest, essentially the price a person or institution charges for the borrowing of money. The most common type of debt is a loan, such as a mortgage or student loan. Other forms include lines of credit and corporate or municipal bonds. Some forms of debt require collateral, or an asset that can be seized if you default. Debt often gets a bad rap, but there are both good and bad forms of debt.

Federal student loans are one of the most common forms of debt in the United States. Students and parents who need to borrow money to pay for college or graduate school can take out loans from the federal government or private lenders. Those loans turn into debt that the borrowers must repay.

Takeaway

Taking on debt is like renting money...

The lender lets you use the money for now, and in exchange you make a legal commitment to give it back later as agreed — with regular payments for the privilege of using it. Also, just as you might have to put down a security deposit on an apartment to give the landlord peace of mind in case you skip out on the last month’s rent, a lender may require collateral so that they are not left holding the bag if you can’t repay the loan.

New customers need to sign up, get approved, and link their bank account. The cash value of the stock rewards may not be withdrawn for 30 days after the reward is claimed. Stock rewards not claimed within 60 days may expire. See full terms and conditions at rbnhd.co/freestock. Securities trading is offered through Robinhood Financial LLC.

- What are different examples of debt?

- What is good debt and bad debt?

- What are typical debt levels?

- Which online tools can help you see the impact of your debt?

- How can you find all your debt in collections?

- What is the first step to managing debt?

- What else can people do to manage debt?

- What is debt consolidation?

What are different examples of debt?

Debt comes in many forms. Some are available to individuals, and others are only available to corporations. Here are a few examples:

- Loans are money lent directly from a lender to a borrower, usually to be paid back by a certain deadline with interest. Some loans, like mortgages and auto loans, have an asset (the car or house) that secures the loan and can be seized if you fail to pay. Home equity loans, which allow you to borrow against the value of your home, minus your outstanding mortgage, are also secured by the home. Other types of loans, like student loans and personal loans, are unsecured, which means there’s no asset provided as security.

- Revolving debt allows you to borrow money up to a limit and pay it back as you go. Examples include credit cards, home equity lines of credit, and personal lines of credit.

- Medical debt accrues if you can’t pay your bills, either from a routine visit to the doctor or an unexpected injury or illness. Medical debt usually doesn’t come with interest, but the provider can refer it to a collection agency if you don’t pay.

- Bonds issued by companies or governments typically pay investors a fixed interest rate over a set term in exchange for borrowing money from the bond holder.

What is good debt and bad debt?

It may sound like a bad thing to owe money, but sometimes borrowing is a smart move. “Good debt” can help you build your earnings and wealth down the road. For example, taking out a mortgage can help you build equity in a home, while a student loan can help you earn a degree that may help increase your earning potential. Meanwhile, “bad debt” pays for things that don’t create value in the long term. That includes high-interest credit card balances, a personal loan taken to pay for a vacation, or short-term payday loans that often come with sky-high interest rates. When you’re tempted to borrow money, you may want to consider whether you’re making an investment that will move you forward or getting mired in debt that will hold you back.

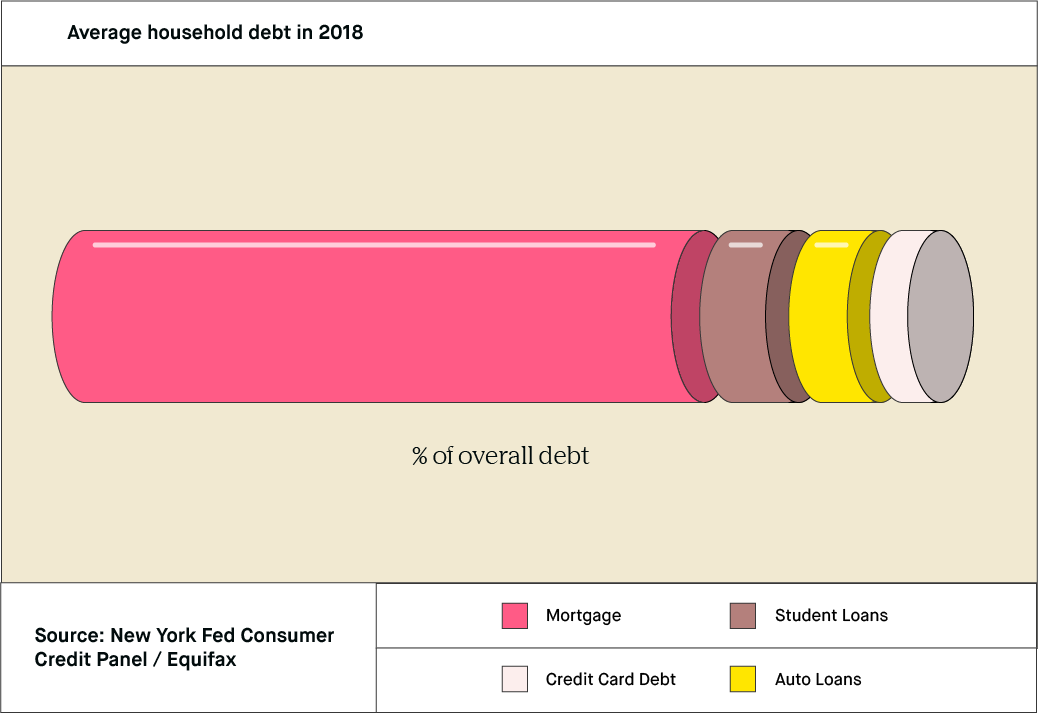

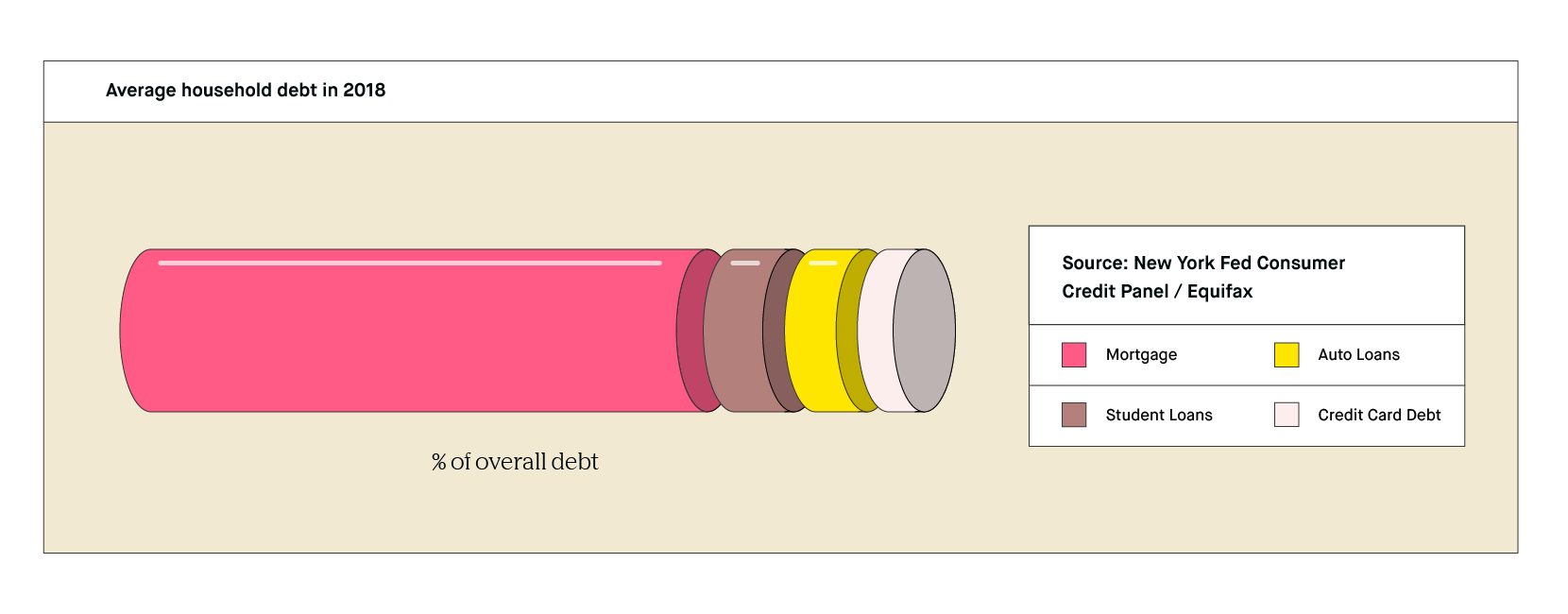

What are typical debt levels?

As a whole, American consumers have more outstanding debt today than ever before, owing nearly $14T combined. The majority of that, $9.4T, consists of mortgages. More than three-fourths of families have some kind of debt, and the average amount is around $123,000, according to the most recent Federal Reserve data (2016). But knowing if your own debt is sustainable comes down to your unique financial situation. Holding “bad debt,” like credit card debt or payday loans, is almost always a financial obstacle because you’re likely paying super-high interest rates. On the other hand, having a mortgage or student loan at a monthly payment that’s affordable for you may be just fine. Keep in mind that lenders consider the amount of debt you have relative to your income when deciding whether to give you a loan and at what terms.

Which online tools can help you see the impact of your debt?

Debt can sometimes feel like a burden that’s too big to tackle. But there are online tools that can help you break down your debt and understand what it would take to pay it off. There are loan calculators to help estimate how much you would owe in different scenarios. Other calculators can help project how long it will take you to pay off credit card debt. There are even simulators that can show how different debt scenarios impact your credit score. Owing a lot of money on your credit cards, paying your bills late, missing payments, or not paying the minimum due, are all things that can impact your credit score.

How can you find all your debt in collections?

If you don’t pay your debt consistently, the company you owe can hire a debt collector whose job is to try to get the money from you. If the debt collector fails, the collection agency might sue you to try and recoup the funds. Note that debt collectors must follow strict rules, including not cursing or threatening you, only calling between 8 a.m and 9 p.m., and not lying to you.

If you want to find out which collection agency holds your debt, you can try asking the original company or lender you owed. Otherwise, you can check your credit report with one of the three major credit bureaus — Equifax, Experian, or TransUnion — which should list the name and number of the agency. Make sure the amount the collector is saying you owe matches what’s on your credit report.

What is the first step to managing debt?

The first step to tackling debt is often making a budget. Start by writing down all the money you bring home each month after taxes. Next, note everything you spend in a typical month. Don’t forget to include:

- Housing costs, such as rent or a mortgage payment

- Utilities, such as gas and electricity, your phone bill, and Internet service

- Food, including groceries and eating out

- Transportation costs, like gas, train tickets, or a bus pass

- Minimum payments on outstanding debt, like a car loan, credit card bill, or medical bill

- Other costs, like entertainment, toiletries, etc.

If your expenses, including debt payments, are higher than your income, you may need to find a way to spend less or earn more. That can mean trimming costs for things like going out and shopping, or making more money through a side hustle. The more cash you bring in or free up, the more you can put toward your debt to help eliminate it faster and reduce the amount you pay in interest.

What else can people do to manage debt?

You can try reaching out to the companies you owe money to and explain why you’re struggling to pay your bill. They may be able to put you on a payment plan that would allow you to tackle your debt with an affordable monthly payment.

If you owe a lot on a credit card with a high interest rate, doing a balance transfer might be an option. That means moving your balance from an existing card to a new one that charges no interest rate, or a low one, for a certain period of time. (Note that credit card companies will usually charge a percentage fee of the transfer amount). Keep in mind that this is a temporary move — A much higher interest rate often kicks in if you haven’t paid the whole balance off within the introductory timeframe. Opening a new credit card may also ding your credit score slightly.

You can also come up with a plan for tackling your debt. Two of the main strategies have wintery names:

- The “snowball method” involves paying off the debts with the smallest balances first, while still paying the minimum on larger balances.

- The “avalanche method” involves paying the minimum amount on all your debts and putting any extra cash toward the highest-interest debt.

If you need help, you can reach out to a credit counselor through a nonprofit organization, credit union, university, or another reputable group (beware of ones that want to charge you a lot of money). Counselors can help you make a solid budget and come up with a repayment plan that works for you.

If you’re struggling with student loans, you may have other options. The federal government offers several income-based repayment plans that can make your monthly bill more affordable, and eventually forgiving the balance if you make regular payments. You can also request deferment or forbearance if you’ve run into a temporary hardship. In some cases, refinancing federal or private loans can give you a lower interest rate or lower monthly payment.

What is debt consolidation?

If you owe money to lots of different creditors, making payments can get overwhelming. Consolidation is one way to simplify your payments so you only need to make one per month. Consolidating doesn’t get rid of your debt; it only streamlines it. You can apply for a debt consolidation loan from a bank, credit union, or other lender. You might have to pay fees, and you may end up paying more in interest on the new loan. If you’re constantly racking up debt because of missed payments, having just one bill to pay could help you tackle your debt. But if the fees and interest rates are significantly higher, you may actually owe more and take longer to become debt-free.

Working with a credit counselor can be an alternative way to help simplify your payments. Under a debt management plan, you may be able to make just one payment to the credit counselor’s organization each month, and he or she would then pay your creditors on your behalf. That way, you could potentially pay lower fees and avoid taking on the higher interest rate that can come with consolidating.

New customers need to sign up, get approved, and link their bank account. The cash value of the stock rewards may not be withdrawn for 30 days after the reward is claimed. Stock rewards not claimed within 60 days may expire. See full terms and conditions at rbnhd.co/freestock. Securities trading is offered through Robinhood Financial LLC.