What is a Roth 401(k)?

A Roth 401(k) is an employer-sponsored retirement account that you can contribute to with after-tax income and receive employer contributions.

🤔Understanding Roth 401(k)s

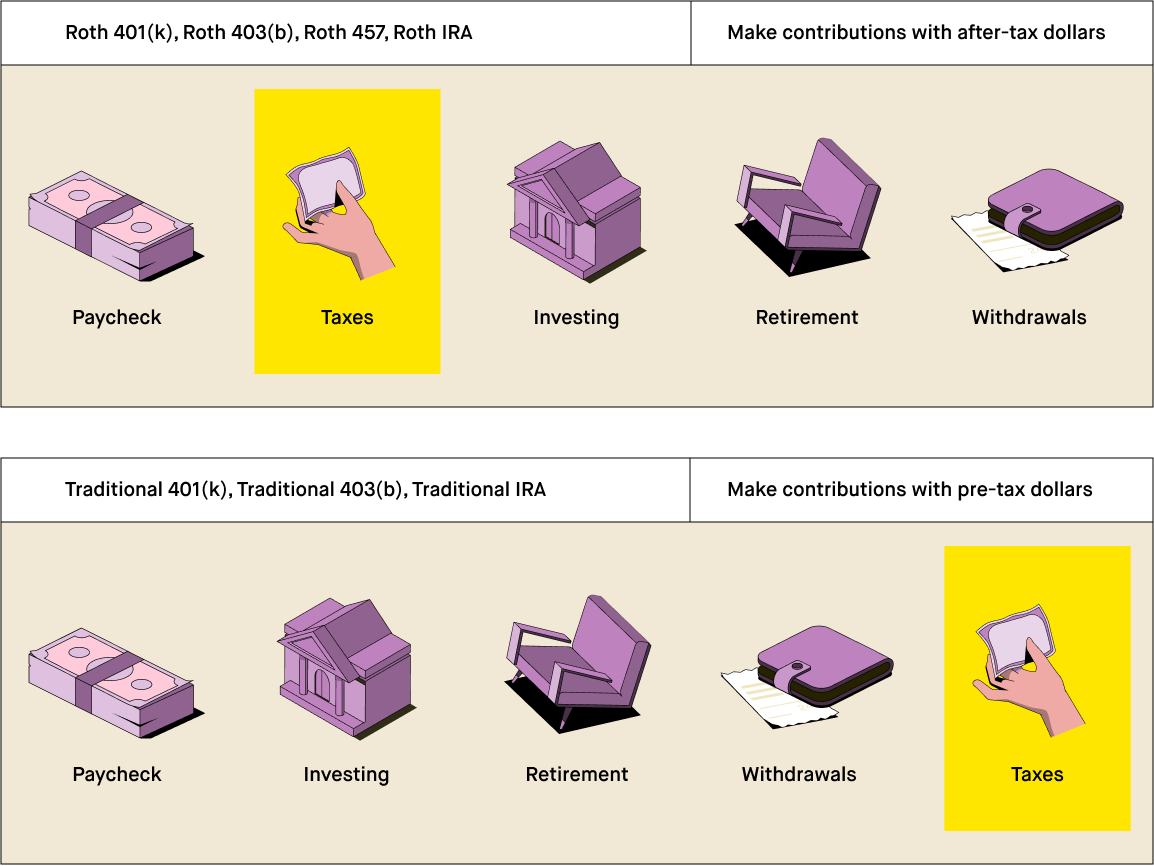

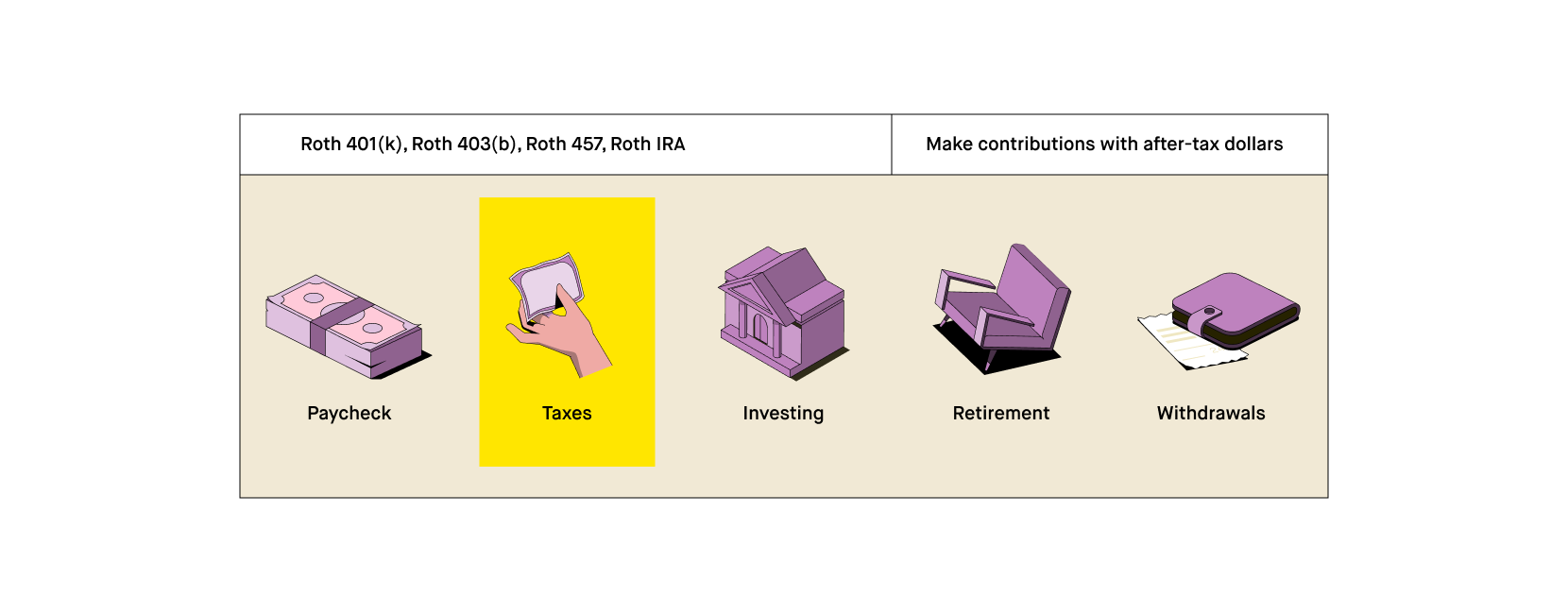

A Roth 401(k) is an employer-sponsored retirement plan that you can contribute to with after-tax dollars. It is like a combination of a traditional 401(k) and a Roth IRA. As with a Roth IRA, you pay taxes up front. Withdrawals in retirement are generally tax-free. The tax rule might sound like a bad deal at first glance, but it might be advantageous if you think you’ll be in a higher tax bracket when you begin to withdraw from your retirement account. Roth 401(k)s have many similarities to traditional 401(k), such as the contribution limit and the potential ability to receive matching contributions from your employer.

Let’s say Beth earns $3,000 per month and decides to contribute to her company’s Roth 401(k) plan. She contributes 10% of her salary, for a total of $300 per month. Beth has already paid taxes on the money before making her 401(k) contribution, meaning the $300 takes up a more significant chunk of her paycheck. But because she’s paid income tax on the money before putting it into her retirement account, any potential investment returns will grow tax-free (there are some minimum conditions), and she won’t have to pay taxes on it when she begins to withdraw from her account when she retires. She’s paying a little extra now to potentially save herself money in the long run.

Takeaway

Traditional and Roth 401(k)s are like vegetable farming…

With a traditional 401(k) plan, you pay taxes on the harvest. With a Roth 401(k), you pay taxes on the seeds. It’s not necessarily the case that one option is better than the other. Each farm will have to make that decision for themselves.

New customers need to sign up, get approved, and link their bank account. The cash value of the stock rewards may not be withdrawn for 30 days after the reward is claimed. Stock rewards not claimed within 60 days may expire. See full terms and conditions at rbnhd.co/freestock. Securities trading is offered through Robinhood Financial LLC.

- What is the history of Roth 401ks?

- How does a Roth 401(k) plan work?

- How much can I contribute to my Roth 401(k) in 2021?

- What are the advantages and disadvantages of a Roth 401k?

- What is the difference between a Roth 401k vs. a traditional 401k vs. a Roth IRA?

- Which is the best type of retirement account?

- Can you contribute to both a Roth 401k and a Roth IRA?

What is the history of Roth 401ks?

Traditional 401(k) plans date back to 1978 when Congress passed the Revenue Act of 1978. In that bill, Congress added Section 401(k) to the Internal Revenue Code. Congress initially created the section to apply to deferred compensation, and employers quickly adopted it for tax-advantaged retirement accounts that we now know as 401(k) plans. The Internal Revenue Service (IRS) updated the 401(k) rules in 1981 to allowed employees to contribute to their 401(k) plans through salary deductions.

Roth 401(k) plans didn’t appear until many years later. In 2001, Congress passed the Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA). President George W. Bush signed the bill into law. The bill was a huge piece of tax reform that made changes to the tax brackets and tax rates, among other things. The act also created the Roth 401(k) and allowed employers to begin offering these plans to their employees on January 1, 2006.

As of 2019, about 50% of employers that sponsor a retirement plan for their employees offer a Roth 401(k), according to one study. Large employers with more than five hundred employees are most likely to offer a Roth 401(k) plan — 61% do as of 2019 — while only about 44% of those who employ between five and ninety-nine employees do.

How does a Roth 401(k) plan work?

A Roth 401(k) is a retirement plan that allows you to contribute to your retirement savings with after-tax dollars, avoiding taxation on the potential growth of your investments inside the account during retirement. When you contribute to your Roth 401(k), you pay income tax on the money before it goes into your Roth 401(k). Then, the money has the opportunity to grow in your account, and (there are some conditions) you can later withdraw your earnings without paying taxes on them.

Your employer can also match contributions to your Roth 401(k), though this match will be in the employee’s traditional 401(k) account. A 2019 study shows that 85% of retirement plan sponsors offer some sort of match to their employees. Often this will look like your employer matching your contributions up to a certain percent. For example, imagine you make $50,000 per year at your job. Your employer offers a Roth 401(k) plan where they match your contributions up to 4% of your income. Therefore, if you contribute at least $2,000 to your 401(k) plan in a year, your employer will contribute $2,000 to your traditional 401(k).

In general, the money you contribute to your Roth 401(k) must remain in the account until you reach a certain age. Once you reach the age of 59½, you may begin to withdraw your earnings (though you must have had the account for at least five years). You don’t have to withdraw from your Roth 401(k) when you turn 59½, but you must begin to withdraw by the time you reach age 72 unless you are still working — these are the required minimum distributions. The good news is that because you paid taxes on your income before contributing it to your Roth 401(k), you don’t have to pay income taxes when you withdraw money.

If you really don’t want and don’t need to begin withdrawing from your Roth 401(k) by the age 72, it is possible to roll your Roth 401(k) into a Roth individual retirement account (IRA) and eliminate the need to withdraw. There are downsides to this option as well, though. Federal law protects 401(k) funds from creditors. An IRA might not have those same protections. Consult a tax professional before making this decision.

How much can I contribute to my Roth 401(k) in 2021?

For 2020 and 2021, the contribution limit for a Roth 401(k) is $19,500, up from $19,000 in 2019. This contribution limit does not apply to your employer’s contributions. As an employee, you can contribute the full $19,500 and still be eligible to receive an employer match.

The Internal Revenue Service (IRS) also has special contingencies for those who are nearing retirement and might need to catch up in their retirement savings. For employees age 50 and older, the contribution limit increases by $6,500. So those age 50 and over may contribute a total of $26,000 to their Roth 401(k) each year, as well as receive an employer match.

So what is the ideal amount to contribute to your Roth 401(k)? In a perfect world, everyone would be able to contribute the full $19,500 (or $26,000) that the IRS allows to gain the maximum tax benefit in retirement. But for many people, that’s too large of a financial burden. If you can’t max out your retirement contributions, aim to contribute at least as much as your employer will match. Your employer match is essentially free money, and it’s best not to squander that opportunity.

What are the advantages and disadvantages of a Roth 401k?

Advantages: Roth 401(k) plans have several advantages. One great feature of 401(k) plans across the board is the high contribution limit. These plans have an annual contribution limit of $19,500 as of 2021 (or $26,000 for those age 50 and older). This limit is quite a bit higher than individual retirement accounts (IRAs), such as the Roth IRA (which has a contribution limit of $6,000). This contribution limit also doesn’t apply to your employer’s contribution, meaning you could end up with well over the contribution limit going into your account each year.

The Roth 401(k) also has some serious tax benefits. With a Roth 401(k), you pay income taxes on your earnings before they go into your 401(k) account. At first, this might sound like a downside. But it can be very advantageous. You pay taxes on your earnings before you contribute them to your Roth 401(k), but then you’re off the hook for paying taxes later provided they are considered qualified distributions. You won’t pay income taxes on your potential earnings when you withdraw them in retirement.

The tax rules for Roth 401(k) plans are especially beneficial to anyone who anticipates being in a higher tax bracket when they retire than they are as they’re contributing to their Roth 401(k). And though it’s impossible to know whether you’ll be in a higher tax bracket after you retire, most of us will probably have fewer options for increasing our income in retirement. So the tax break could be coming at an ideal time.

Disadvantages: Roth 401(k) plans aren’t without their downsides. First, a Roth 401(k) plan might not have as many investment options as a Roth IRA. With employer-sponsored 401(k) plans, you get to direct your investment. But you can only choose from the investment options your employer has offered. With individual retirement accounts, you may have greater control over where your investment goes.

A Roth 401(k) might also be a disadvantage if you pay a higher tax rate now than you expect you will in retirement. With a Roth 401(k), you pay taxes before you contribute your earnings to your retirement plan. With a pre-tax plan like a traditional 401(k), you pay income taxes when you withdraw the money. If you’re in a lower tax bracket when you’re retired than you are now, you might pay less in income taxes down the road than you would today.

Finally, Roth 401(k) plans have strict withdrawal rules. With an employer-sponsored Roth 401(k) plan, you have to begin withdrawing when you have reached age 72, but there is no required minimum distributions age for a Roth IRA.

What is the difference between a Roth 401k vs. a traditional 401k vs. a Roth IRA?

Roth 401(k) plans aren’t the only retirement savings option available. The Roth 401(k) is a newer version of the traditional 401(k) plan — think of it as the younger sibling of the traditional 401(k). The traditional 401(k) and the Roth 401(k) are very similar. The only difference between the two is when you pay taxes on your money. With a Roth 401(k), you pay income taxes on your contributions before you contribute them to your retirement account. Then you withdraw your contributions and any earnings tax-free provided they are qualified distributions. Traditional 401(k) plans are the opposite. You contribute to your traditional 401(k) plan before you pay income taxes. Then you’ll pay income taxes as you withdraw your contributions and any earnings in retirement. The rest of the rules surrounding 401(k) plans are the same — this includes the contribution limits, employer matches, and age to withdraw money for required minimum distributions.

Another option for saving for retirement is an individual retirement account (IRA). A Roth IRA, as with a Roth 401(k), requires that you pay income taxes on the money before you contribute it to your account. Then, the money grows in the account, and you won’t pay taxes on your earnings. The Roth IRA is a very different account than the 401(k). The Roth IRA is for individual retirement savings, meaning you open and run this account yourself. The contribution limits for Roth IRAs are much lower than a 401(k). As of 2021, the contribution limit is $6,000. Individuals over the age of 50 can contribute an extra $1,000 to help them catch up — this brings their total contribution limit to $7,000.

Another notable difference between Roth 401(k)s and Roth IRAs is the income restrictions. Roth 401(k)s have no income restrictions. But in the case of a Roth IRA, the income limit for contributing the maximum for singles is $124,000 in 2020 and $125,000 in 2021; for taxpayers married filing jointly it is $196,000 in 2020 and $198,000 in 2021.

That being said, you can get around these limits with what’s called a backdoor Roth IRA, where you contribute to a traditional non-deductible IRA and then immediately roll the contribution over in a Roth IRA. This conversion triggers income taxes on the appreciation of the after-tax contributions. Additionally, each conversion amount is subject to its own five-year holding period to qualify for tax-free withdrawals.

Which is the best type of retirement account?

There isn’t one type of retirement account that is inherently better than the others. They all have pros and cons. It just comes down to determining which is the best option for you.

Ideally, you would have two different types of retirement accounts — you should have a 401(k) through your employer (either traditional or Roth) and an individual retirement account. From there, you can determine whether you’d rather see the tax benefits on the front end (in which case you should choose the traditional route) or the back end (in which case you should choose the Roth option).

Can you contribute to both a Roth 401k and a Roth IRA?

The good news is, the Internal Revenue Service (IRS) allows you to contribute to more than one retirement account. Specifically, you can contribute to both an employer-sponsored account like a traditional 401(k) or Roth 401(k) while also contributing to an individual retirement account (IRA).

What’s even better is that the contribution limits on the two accounts don’t overlap at all, meaning you can max out both accounts each year. Based on the 2021 contribution limits, that means you can contribute $19,500 per year to your Roth 401(k) plan (or up to $26,000 if you are age 50 or older) and contribute up to $6,000 annually to your Roth IRA (or up to $7,000 if you’re at least 50.)

You could also elect to contribute to a Roth 401(k) plan through your employer and opt for a traditional IRA instead of a Roth IRA. What would be the benefit of this? Why not just opt for the Roth IRA? It’s likely impossible to know today what tax bracket you will fall into when you’re retired. You might be at a higher tax bracket in retirement, in which case it would be helpful to have Roth retirement accounts. But you also might be in a lower tax bracket, in which case it would be more beneficial to pay the taxes later.

Using both Roth and traditional retirement accounts allows you to diversify your retirement strategy a bit. You’ve already paid taxes on some of your retirement funds, but not all of it. So whether you fall into a higher or lower tax bracket in retirement, you’ve spread out your tax liability a bit more evenly.

Any examples provided are for illustrative purposes only and not a recommendation of a security or investment strategy. Robinhood does not provide tax advice. For specific questions, you should consult a tax professional.

Any third party links are being provided for information purposes only. Robinhood is not affiliated with and does not endorse, authorize or sponsor any of the listed websites or their respective sponsors. Robinhood is not responsible for the content of any website or the collection or use of information regarding any website’s users and/or members.

New customers need to sign up, get approved, and link their bank account. The cash value of the stock rewards may not be withdrawn for 30 days after the reward is claimed. Stock rewards not claimed within 60 days may expire. See full terms and conditions at rbnhd.co/freestock. Securities trading is offered through Robinhood Financial LLC.