Assumptions can get you in trouble

Assumptions can get you in trouble

It’s easy to make assumptions.

At breakfast the other day, we were given what the server claimed was the last bottle of sriracha in the restaurant. Like the shortages of sunflower oil that started last year, several at the table assumed it had something to do with pepper supplies blocked by the war in Ukraine (which doesn’t make sense due to where peppers are usually grown).

It was actually down to a dispute the maker of the famous sriracha with the green-capped bottle had with its pepper supplier several years back. The company has struggled with their pepper supply chain ever since. Now you can find the sauce for $18/bottle on Amazon—talk about inflation. And all because of one disagreement.

It shows you how intertwined a single human relationship or decision can be to profits and economic conditions for the rest of us. The just-announced bankruptcy of Yellow, the trucking company, was also a tangled web, which could have an impact on the economy, inflation and, by relation, us.

I first read about the risk of their demise in conjunction with their negotiations with the Teamsters labor union. My mind immediately (and incorrectly) surmised that union demands led to a risk of strike, which in turn drove the company’s customers to flee, stressing their already weathered financials. While the negotiations likely didn’t help, there is much more to the (hi)story.

In short:

While the company started nearly 100 years ago, the long haul unionized shipping business was born in 1951, and grew through acquisitions over the years. Their success was based on lower rates than competitors and “less-than-truckload” capabilities (which allows for smaller quantities to fill in gaps) to large retailers, like Walmart and Amazon.

In 2003, they acquired Roadway, another unionized trucking firm, to increase competitiveness… but never combined their networks, limiting cost savings. When the 2008 GFC hit and demand fell sharply, they just couldn’t manage the operations with these higher costs.

This decision haunted them for years and they flirted with bankruptcy several times, getting bail outs from the union workers (through lower benefits and pay) and the US government.

Perhaps they assumed they had plenty of time to eventually integrate or assumed their growth would always be enough for the cost savings to not matter. Yet, with interest rates higher now, demand falling post-pandemic, and workers wanting to be compensated more, the company decided to fold a few days ago. Just like the sriracha, this could also hurt us as consumers. With Yellow being the lower cost provider, shipping costs could end up a bit higher. Now transportation is only about 6% of the common measure of inflation (CPI), so it may not be reflected in that aggregate data, but it could be felt by us all in slightly higher consumer prices.

There are other companies out there that made incorrect assumptions. Many banks assumed interest rates would be low forever, causing asset losses for them when they went up. Others assumed life would be lived exactly as it was before, after a global pandemic, like office real estate companies, and even the brand Tupperware which still relied on in-person sales and cheap funding.

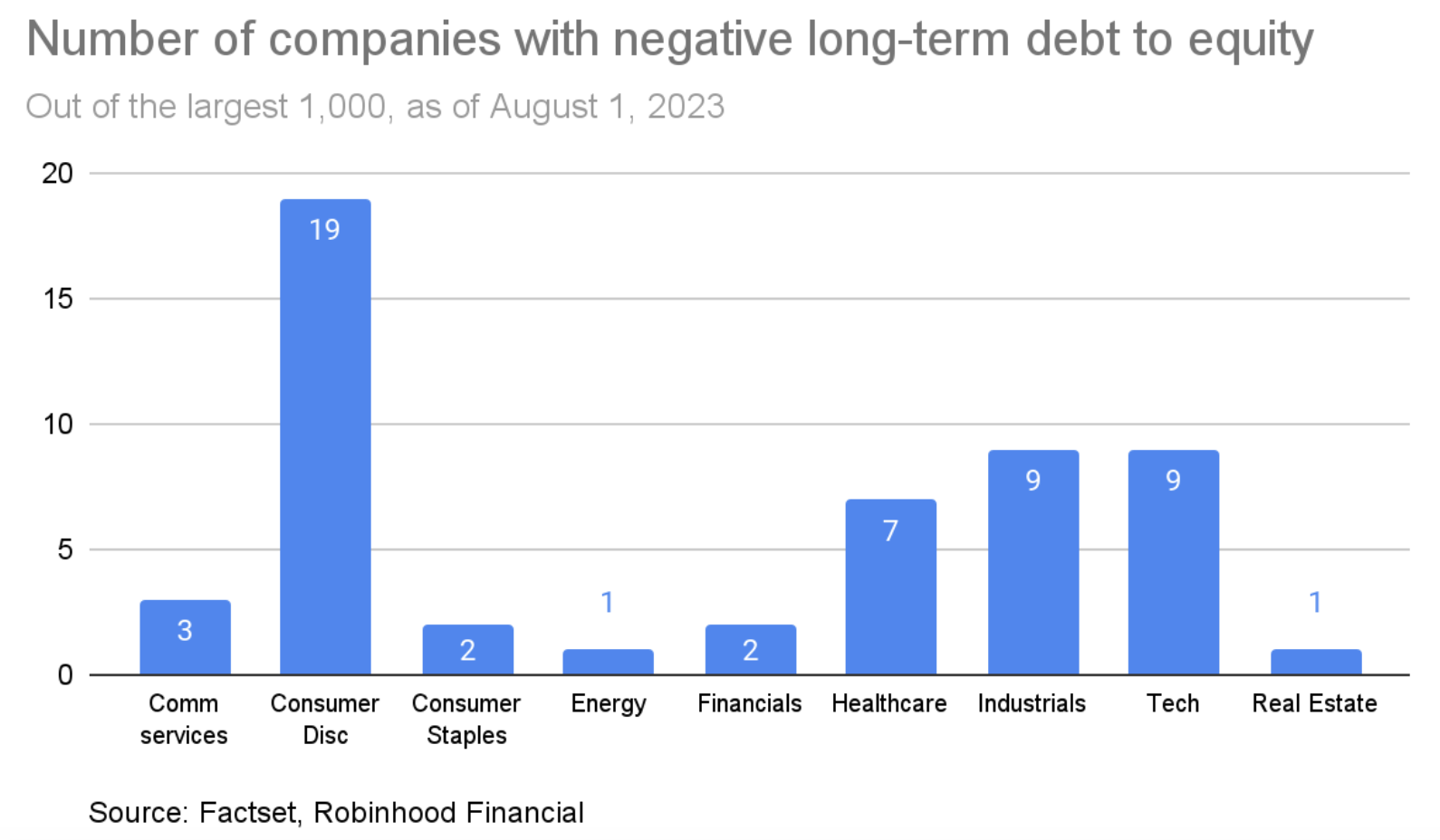

What could be next in this realm? I don’t foresee a broader-based issue right now, but suspect there are individual companies that could struggle sooner rather than later. So I looked through the largest 1,000 companies for those that had similar balance sheet characteristics as Yellow—and maybe even other similarities like sector or a union employee base. In particular, I analyzed long-term debt relative to equity. Of the 1,000, 53 companies had negative debt to equity*, meaning their debt levels were higher, while their equity was valued below zero. As you can see from the chart below, 35% of those are consumer companies.

Included within this list of 53 is a more traditional mattress company, a movie theater, a traditional car rental company, hotels—and an industrial airplane parts supplier . It’s no wonder the consumer discretionary sector has had the most bankruptcy filings year-to-date according to S&P Global—the way of life and cheap-funding-forever assumptions are easily inherent there.

As I shared in May, higher interest rates and changing ways of life mean companies that can pivot and manage risks are best positioned to be here for the long term. Those that made assumptions of future economic conditions, or were just hanging on in a low interest-rate environment, will find it harder to thrive in a higher-rate environment (since funding is less easy to find and credit conditions are tighter).

So try not to make assumptions about forever when picking your own stocks—or really anything else in life.

*Some ways a company can have “negative equity” on their balance sheet: 1) The company has a huge amount of debt (aka over-leveraged). 2) They did a ton of stock buybacks. The company may repurchase its common stock from shareholders, resulting in a reduction of equity. 3) They made dividend payments they really couldn’t afford. This is when a company paid more in cash dividends than it had in cash profits. 3) They created provisions for expected future debt they know they will take on.