Growing up from 0% interest rates

Growing up from 0% interest rates

While cleaning out old toys this weekend, I got to witness a moment I won’t forget. After my daughter brought up an old dollhouse to be given away, something she got as a gift when she was two, she put it down on the ground and played with it for a couple minutes. In that moment, I watched her say goodbye to it in her own way, and to her younger childhood all at once. I felt like I was in Toy Story.

You might have spent your childhood counting down the days until you’re an adult and could do whatever you want. And, equally, as a parent, I’ve spent some days counting when my own kids would be independent. But in this case, both of us, with different perspectives, revered the transition. The market is in transition too. It’s looking to grow up from the 0% interest days and find its independent self. The question is whether it will take an economic recession (beyond the market recession we had last year) to see it through.

So far, there is evidence we are not there yet:

Earnings season, which is almost done with S&P 500 companies, was stronger than expected. Of the companies reporting, 75% had actual revenues that were above estimates (greater than the 5-year average of 69% and 10-year average of 63%, per Factset).

Employment and jobs are stable, with unemployment still low. Last Friday’s employment report showed employment rose +253,000 month-over-month (m/m) in April, though there were downward revisions to the previous two months (totaling -149,000). Average hourly earnings were up +0.5% m/m and 4.4% year-over-year (y/y)—an increase from the previous month.

Speaking of which, and as I shared last week,

Core inflation, and wage inflation, still remains higher than the Fed would like. Put together, that means it continues to be likely the Fed needs to keep interest rates higher for longer. And the market still doesn’t believe it. The general intention of keeping rates higher is to slow growth, in order to slow inflation. That could push us into recession, but it's not a foregone conclusion.

But,

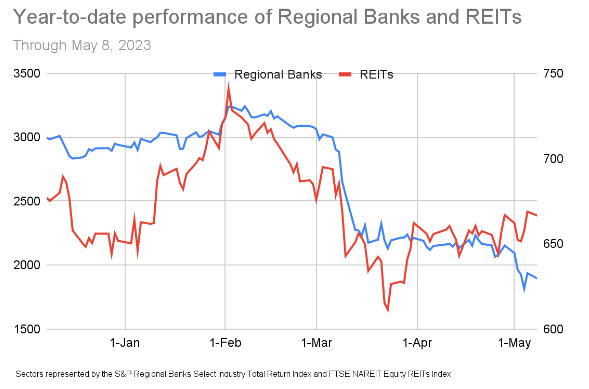

Interest rate-sensitive sectors are the most in transition. Banks and Real Estate Investment Trusts (REITs) have performed terribly this year, with higher rates and stresses in both sectors. During earnings season, they also did the worst against the expectations for their earnings, with over 30% missing or only meeting expectations. However, these were also the three sectors with positive revenue growth vs. the whole market tracking to negative revenue growth. They just weren’t positive enough to overcome expectations.

And the transition in these sectors will eventually have an effect on growth. On Monday, May 8, the Fed released its Senior Loan Officer Opinion Survey. In nearly every category, lending standards were tighter (meaning there are more criteria to meet, and higher costs, for loans). This includes loans to businesses, commercial real estate and households (mortgages, autos, etc.). Demand for all of them has also waned, with higher rates. Whether or when the slowdown makes it to employment data will signal the seriousness or if it’s closer to the end than the beginning.

This all should inevitably lead to weaker growth, which is the natural part of an economic transition. But like our own personal transitions, they usually end up with some material growth once it’s over.

Source: Factset, Robinhood Financial, Bloomberg, Federal Reserve