Historical cicadas and a review of recession chances

Historical cicadas and a review of recession chances

Deep in an IG scroll, I came across a clip from recent SNL featuring two “cicadas” stopping by the Weekend Update desk. The cicadas were repping the emergence of two specific broods (Brood XIX and XIII) this summer across 17 states in the Midwest and Southeast—something that hasn’t happened in 221 years. The actors playing cicadas bragged about how loud and lit their “party in the stump” would be. 😆 Thanks to these large crunchy insects, summer will be noisy for many (at least for several weeks).

It made me think about how economists and strategists may occasionally have the same behavior. Coming out to make noise about their view and then go back underground, especially if they aren’t quite accurate. As a client facing person most of my career, I appreciated those that came back to tell us why their predictions may not have happened—and what they thought now.

So I was happy to have a colleague recently ask me outright: “do you still think there could be a recession?” (in reference to this post).

The short answer is yes—in the consumer sectors of the market. But it’s taking longer than I thought it would.

For context, in September 2023, I wrote about where we could potentially see a recession, noting: 1) higher rates were going to be felt sooner rather than later AND 2) discretionary spending could fall as inflation remained sticky while consumer companies would not have the pricing power to maintain earnings.

Where I think we are now:

While higher rates created some initial cracks in 2023 (regional banks posting losses from longer term bonds including one bank failure), the noise, like the ones from cicadas, is starting to slowly build up—from commercial real estate worries to the frozen housing market to rising credit card balances.

We are seeing a spending slowdown play out in the retail sector now. From Walmart to Target to fast food companies like McDonald’s, they all noted a softening in demand in their earnings reports and are lowering prices given the slowing demand from consumers.

Why is this taking longer?

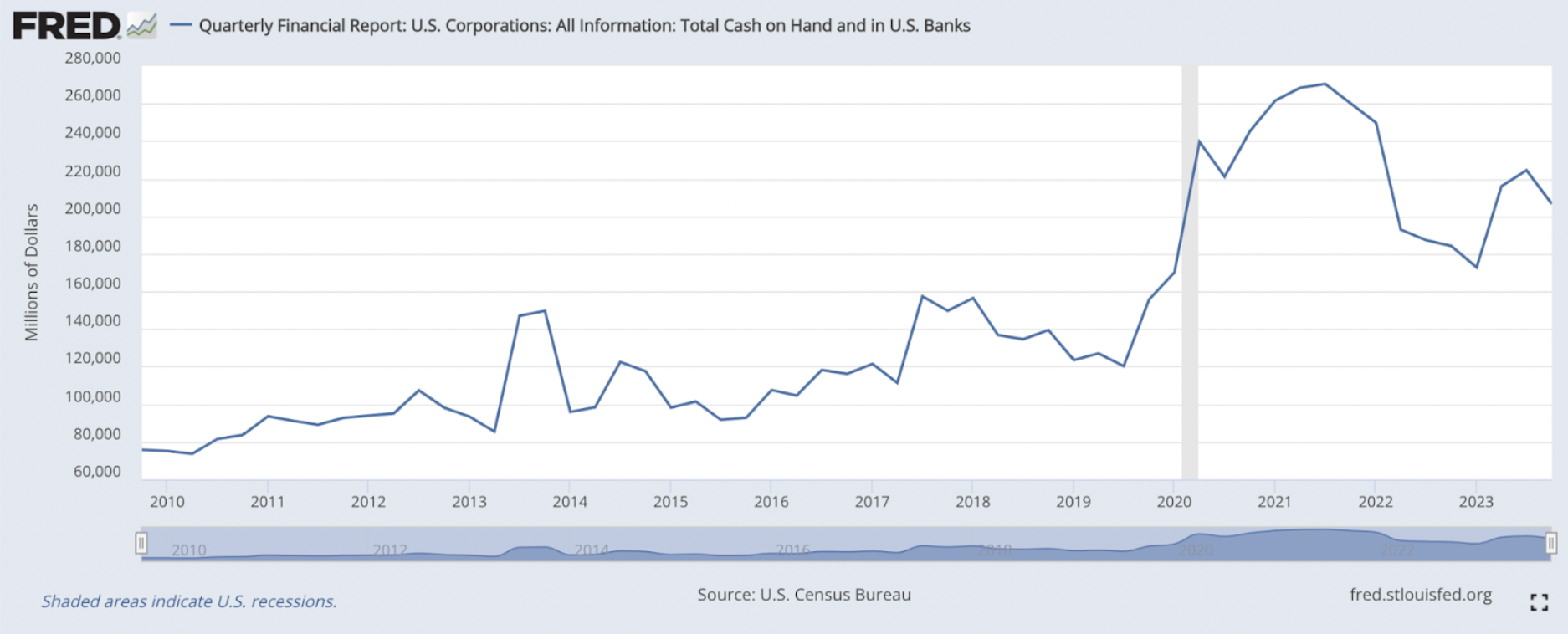

Companies still have a lot of cash on hand.

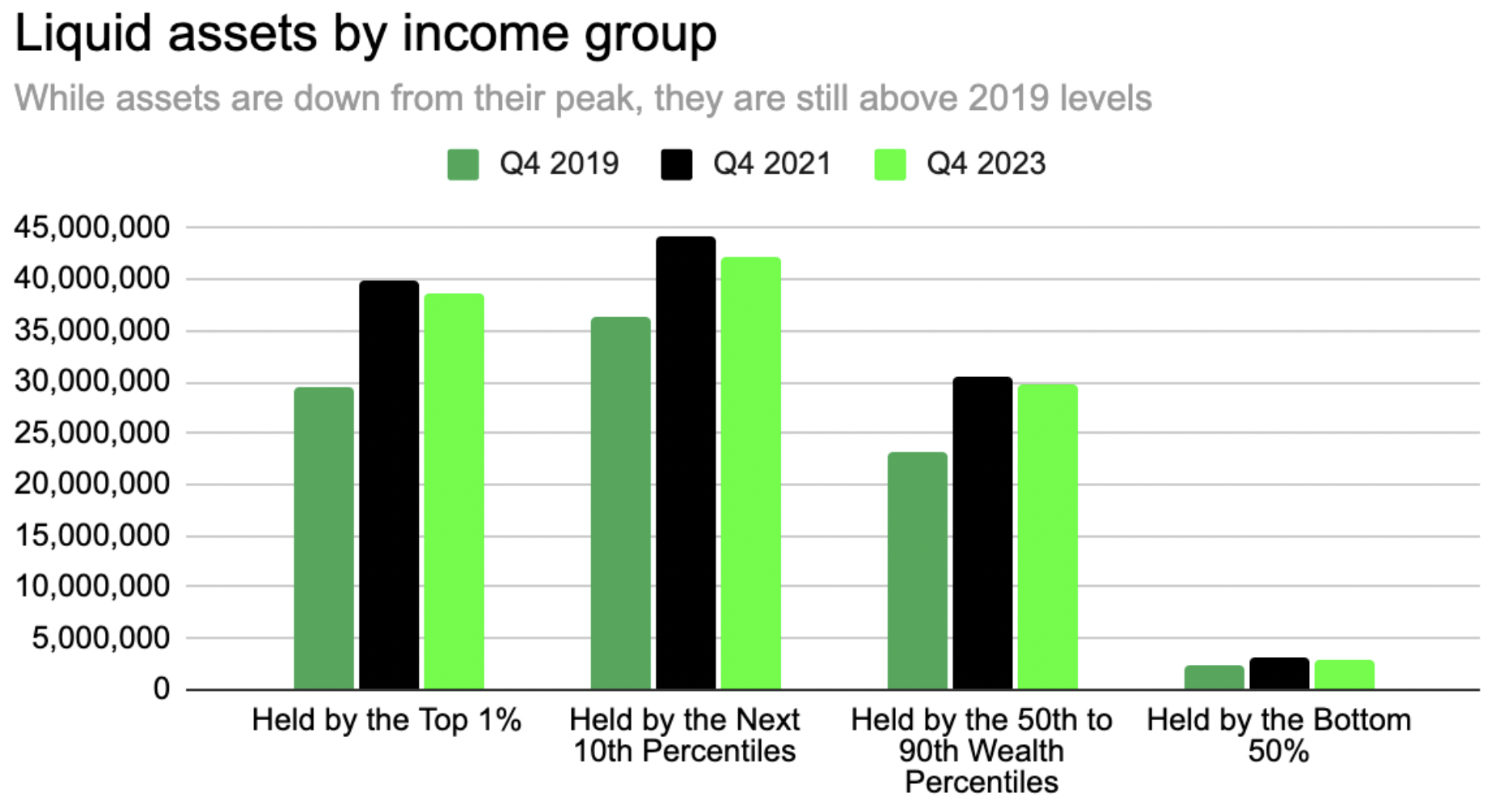

While it’s less than it was, consumers generally still have liquid assets, albeit at different levels. If they are part of the cohort that has these levels of wealth, I believe they are fatigued by inflation and being more discerning about where they spend now.

The Federal government has been handing out cash: Between the $50b CHIPS Act, which multiples investment in the tech and science industries, and the Inflation Reduction Act, which provides, $391 billion worth of funding, tax incentives, grants, and subsidies towards energy while aiming to cut the deficit (has not been successful on this part yet), there are extra funds in the economy. While these are noble in intention, the spending exacerbates the spending already out there, and our deficit, which makes it tougher to see lower inflation levels.

The longer inflation is here, the longer rates are higher and consumers get fatigued, which I believe they are now. So a recession may still be in the cards—-in the consumer sectors—but it’s been a slower roll out. Just not quite as long as it takes a cicada to come back out.