The company you keep: the potential for a recession next year

The company you keep: the potential for a recession next year

Watch the company you keep. When I heard this as a kid, my mind always went to the negative side of that statement. I internalized not being friends with so-called troublemakers. But what I didn’t consider back then was the positive side of it—that being in a group with rising stars could lift me too. I was reminded of this realization watching a video clip of Coach K on X, sharing his mom’s advice to “make sure you get on the right bus… and only get on a bus that’s driven by a good person.”

Similarly, the direction of market prices often drives sentiment—meaning when prices rise, investors more often feel the economy is doing well and vice versa. I see it as especially true for those benefiting from a rise in prices. And, in my experience, those not benefiting state everything that is wrong with it and wait it out—continuing to not benefit.

As I’ve discussed in past posts, you’ve seen that happen this year. At the start of the year, economists and strategists called for more downward pressure and a recession. You saw them hold their ground, calling out risks with the consumer, in real estate, and high market valuations that would end this year in demise, until around mid-year. Now that markets are still higher, and we are not in a recession, many softened their stance or outright changed their mind.

Maybe just in time to watch a mild one start to actually unfold. Now that we can see a “soft-landing” scenario in sight, I’ve started to believe all the work and talk the Fed has done to curtail inflation and the other anti-debt forces, like the rise in the 10-year treasury yield and the likely higher r* could start to actually threaten growth.

It’s an accepted principle that it takes time for higher rates to affect growth (and thus inflation). In 1995, the San Francisco Fed published a paper citing the impact from monetary policy is the highest two years after changes in policy (though in one model, it was in the 3rd year). Many have tried to say that the impact from higher rates on growth should be quicker than in the past, so it would have made its way through the economy already if it was going to. But I don’t believe it. It just takes time for higher rates to work through the places where money is borrowed.

What might be different this time, however, is that interest rates may have started to feel higher five months before the Fed actually started raising them. The San Francisco Fed takes a measure of financial variables and formulates them into a “proxy funds rate.” This proxy rate, according to the SF Fed, “can be interpreted as indicating what federal funds rate would typically be associated with financial market conditions if these conditions were driven solely by the funds rate.” That’s a mouthful, so put simply, this rate interprets things such as guidance where the Fed sees rates heading and their balance sheet operations, to come up with what rates feel like, not just what they are (vibe rates?).

Below is a chart of the actual funds rate in blue and the proxy rate in red. Around November 2021, the proxy rate started rising while the actual Fed funds rate stayed around 0%. The Fed didn’t start increasing rates until March 2022. And today, the proxy rate is nearly 7% vs. the actual Fed rate of around 5.5%, thanks to tough talk by the Fed Chair DJ Powell last week and QT*.

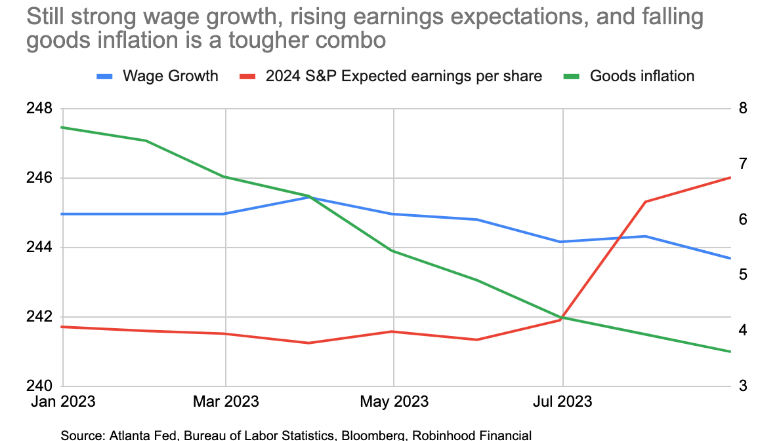

We are nearing the 2 year anniversary of the proxy rate rising—and closer to the estimated peak of impact on growth. As I looked at this, several anecdotal stories, like friends in the tech sector saying the job market is tough, and that I’m seeing more discounts in the retail space, started to become more noticeable. Add in rising earnings expectations (that make it easier to disappoint), while wage growth has stayed solid (keeping labor costs up), with less ability of companies to pass on higher prices from falling goods inflation (but energy and food inflation is still elevated) and I believe we could be heading towards a disappointing combination in 2024 (chart on all these pieces below).

While I still think we could see that much-talked about goldilocks-like soft landing in the near term, it's the world in several months from now I am more worried about.

Of course, I’m not definitive on this yet, so I’ll continue watching to see what bus the markets get on—and the company it keeps.

*QT = quantitative tightening. This describes the Fed not buying any bonds for themselves and letting old ones they bought mature without re-purchasing new ones. Opposite to the period from 2009 to 2020 when they actively bought bonds driving interest rates very low.