Another look at the housing market

Another look at the housing market

Sometimes when you’ve been going nonstop, you get to a point where your body commands you to sleep. It’s like you’ve finally reached the edge of your awake/asleep line and there’s no stopping you from crossing it. You could almost sleep anywhere.

I’ve thought about the awake/asleep line a lot lately, and how it’s like slow-moving economic data that suddenly speeds up once a threshold is crossed. In particular, data on the housing market can be like that.

Back in September 2022, I wrote about the housing market and just how extreme it got over the last few years — even compared to the build up from 2006 to 2008. For context, in this most recent housing cycle (2012 to 2022), the trough-to-peak increase in home values was 8% per year, spurred by a significant drop in mortgage rates. At the time, I thought housing prices would fall, but would take time to do so… and that it would vary by region.

In the spirit of keeping it real, I thought I would check in on the housing market relative to my views… and not to spoil the conclusion but, I have the same opinion — prices will continue to fall, albeit slowly.

Now, I give you the housing market since our last update in three charts:

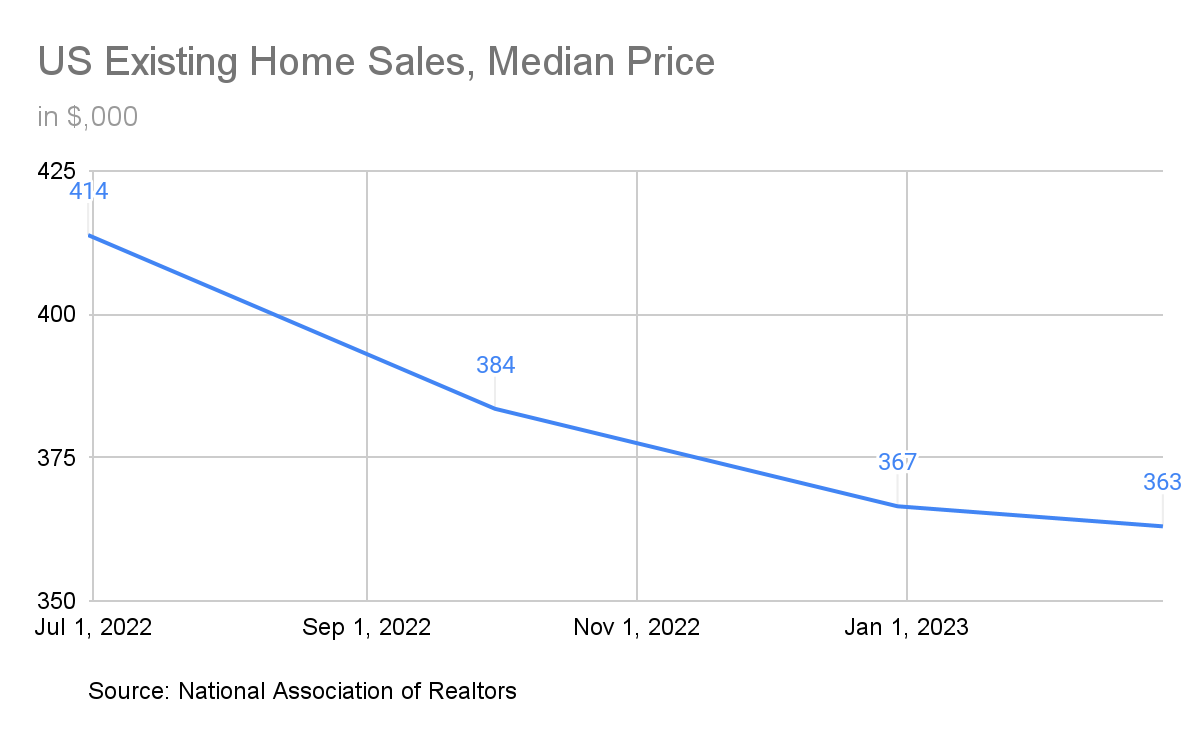

Home prices have begun to fall on a national basis.

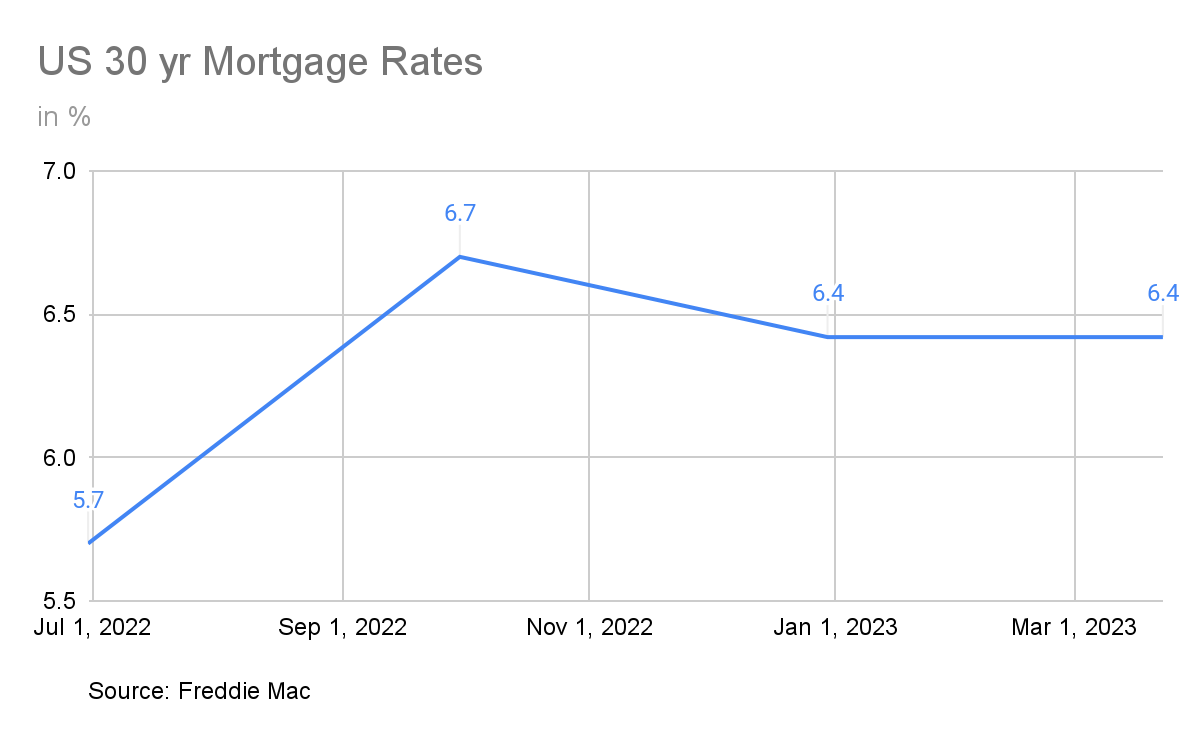

Mortgage rates have stayed around the 6.5% mark — about 40% higher than one year ago.

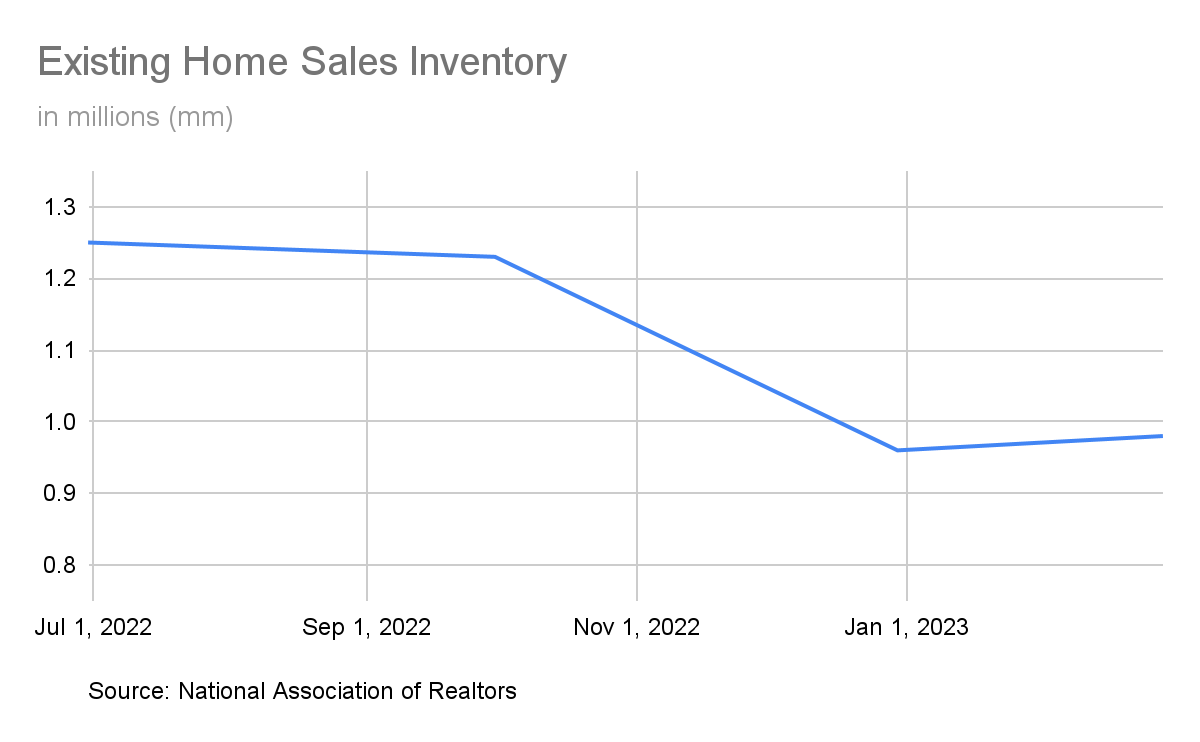

Why have home prices still been somewhat resilient? It’s a number of factors, but if people have low mortgage rates already locked in, they are less likely to sell/move and take on a higher mortgage rate (speaking from personal experience!). And you can see inventory of homes for sale has stayed low as a result:

Keep in mind, the 20-year inventory average is 2.3M; while inventory has been 1.5M or lower since 2020.

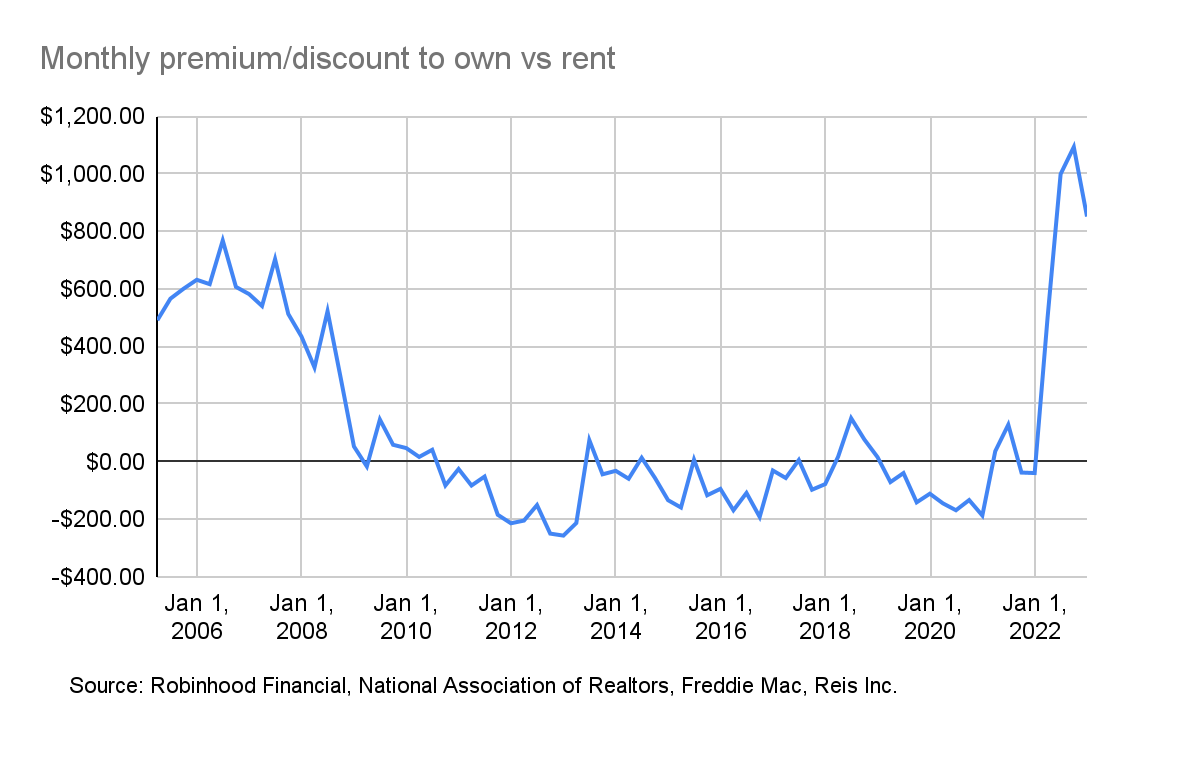

On the other side, if home prices haven’t fallen much, but mortgage rates are still elevated, housing affordability must be low — but how does that compare to renting? Using the data on existing home sale prices, mortgage rates, and an assumption of a 20% down payment requirement, we compared this to net effective monthly rent data. Unsurprisingly, on a national basis, it’s more expensive to buy than rent now:

And all of this contributes to a slower fall in prices, and lower inventory. In short, both buyers and sellers are seemingly less motivated.

But, like I also said last time, real estate is local, and the story continues to be different by region. The number of sales has dropped by less in the Midwest and South vs. the Northeast and the West — which is aligned with the general trend of leaving more expensive, bigger cities, exacerbated by Covid.

What are the risks to my view? A major one is that the job market has stayed relatively robust. Even with lower affordability, if people have jobs and income, the probability of stability remains. One more is that given there was so much buying in the 2020-2021 period of very low rates, perhaps the need to buy is much lower now, too — demand continues to just meet supply without either changing much.

But one new thought here: I believe the recent issues we’ve seen in the banking sector could make a drop in home values speed up a touch. This is because banks could make it tougher to get a mortgage due to their own desire to take on less risk, which, in turn, could slow down buyers.

One thing is for sure to me though — we are at “the line” for housing.