Terms and conditions: our outlook for 2024

Terms and conditions: our outlook for 2024

I saw a social media post the other day saying they’d like to read the terms and conditions of 2024 before agreeing to them. That kind of skeptical humor is my jam. And I like to apply it to my own analysis of the markets.

We’re halfway through December, so it’s about time to do as many strategists across the US and world have done—share an outlook for 2024. In the spirit of skepticism, I am laying this out as a series of terms and conditions. The terms of the markets come with conditions in which they may come true.

These terms and conditions outline the economy’s and market’s rules and regulations for the use of them in 2024. We reserve the right to amend these terms and conditions as the markets change and new data is published. This is a longer than average note so we thank you in advance for reading it.

Sections below:

US Economy: Cautious

Interest rates/Bonds: Volatile, but about the same as today

US stocks: Cautious for now

Other parts of the market

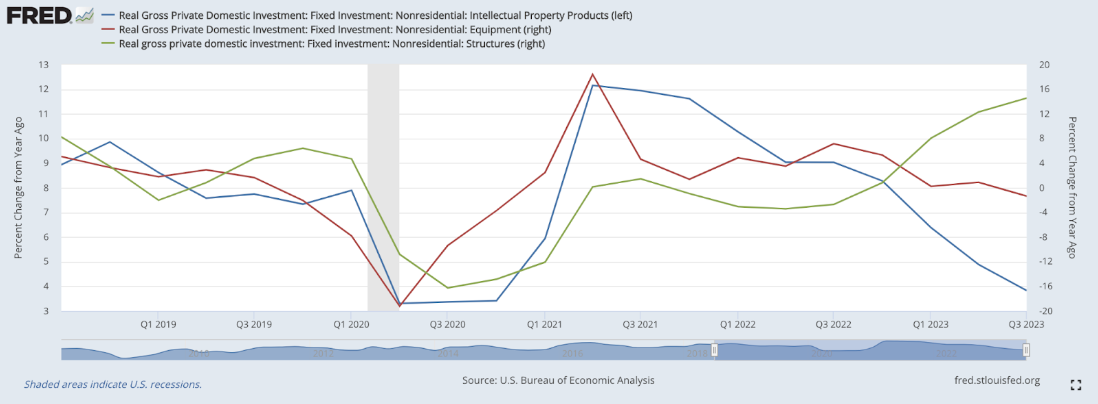

US Economy: 🟡 Cautious. With the amount the Fed has hiked rates since March 2022, from 0% to 5.25%, historically, this would have already driven the US into a slow economy. But we don’t have that yet. I don’t think that means the transmission from tighter monetary policy to a slower economy is broken. In fact, most business capital spending, and even the housing market, two areas typically sensitive to changes in interest rates, have been contracting. It’s just that the slowing has been slowed down (?) by accommodative fiscal policy from the Federal government—in the form of the CHIPS Act and Inflation Reduction Act. You can see in the chart below real business investment has been falling (red and blue lines) except in structures (the green line). That’s because these Federal programs have provided billions of dollars to US projects, particularly in the form of funds for new warehouses, factories, labs, and other production for tech.

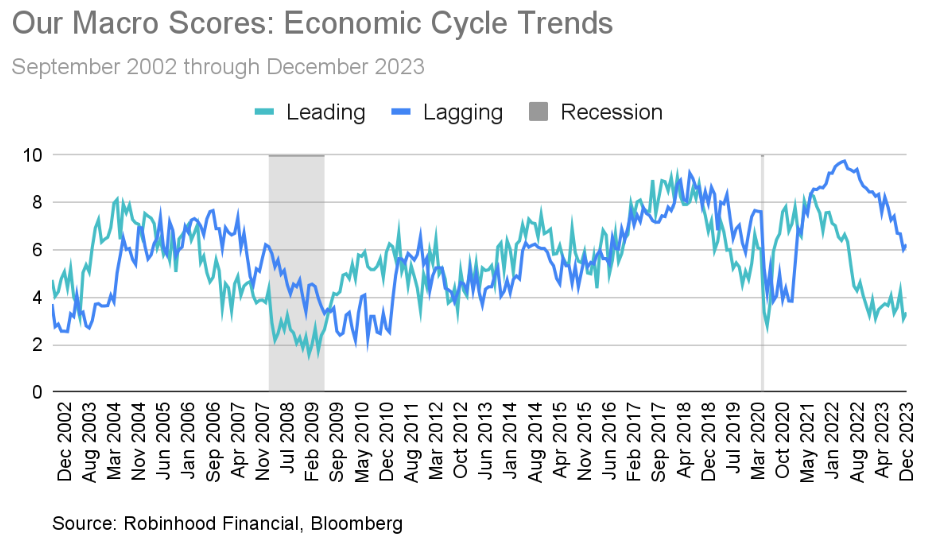

Despite these programs, I do think the slowing will continue. It’s just taking longer. So the pending recession many have been calling for, for the last year, may still come. Our own leading macroeconomic score, that aggregates a multitude of leading indicators to show us the health of the US economy, has been bouncing along the bottom for some time now (mint green line in the chart below), while the lagging indicators (blue) are very slowly falling:

The dispersion between the two lines is wider than in other times in history, which supports why there is so much debate on 2024 from an economic perspective.

Nevertheless, I believe the blue line will catch up with the mint green line next year, meaning the economy will continue to slow into a mild recession by mid-2024.

Important to note, I believe the labor market will soften some in the scenario I have painted here. This may come about as companies look to maintain their margins in the face of less revenue opportunity. But I don’t expect it to be severe.

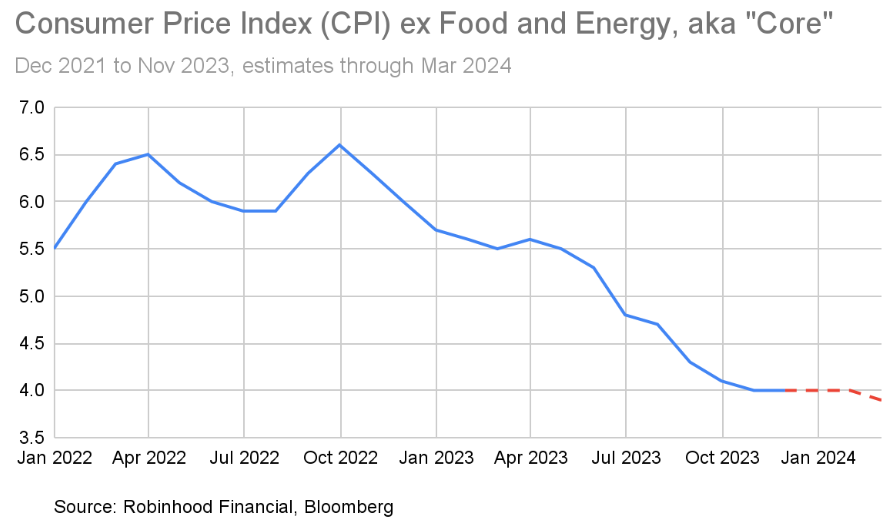

Interest rates/Bonds: 🟡Volatile but about the same as today. These matter because they impact market valuations and company metrics. As mentioned above, the Fed has regularly hiked short term interest rates, to slow down the economy in an effort to cool inflation. And they are not alone—inflation was a global phenomenon—so many central banks around the world have also raised rates to an average of 4.5% in the developed economies. And inflation is still hanging around. The November US CPI report showed core inflation stayed the same as the previous month, at +4% year-over-year, and not yet near the Fed’s target of 2%.

While core inflation has cooled from a peak of 6.6% in September (as the chart above shows), from here I think it will be tougher to get it meaningfully lower. So I believe the Fed will keep rates where they are (5.25%) until June, then cut about 1% during the 2nd half, to account for lower inflation.

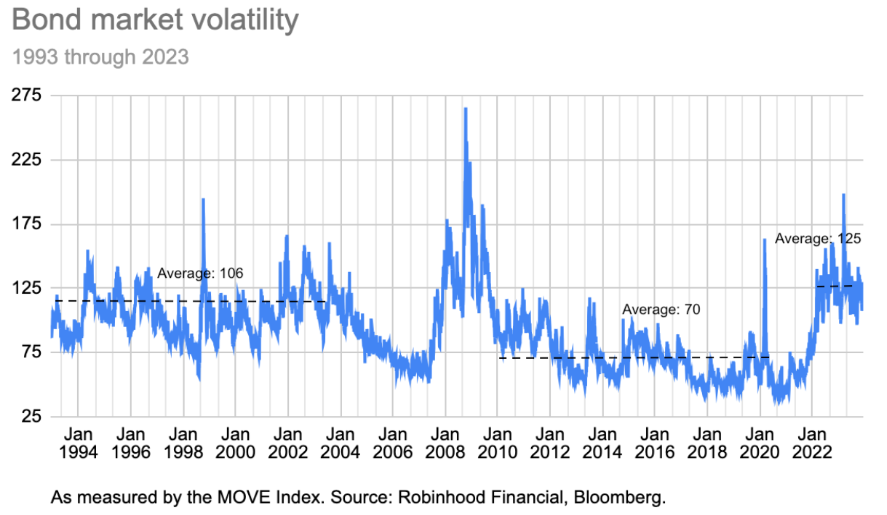

As for longer term interest rates, such as the 10 year treasury rate, they have been on a wild ride this past year—from a low of 3.3%, up to 5%, and now at 4.2%. The MOVE Index, which measures the volatility, or swings, in the bond market, has been elevated, averaging around 125. To put that number in context, from 2010 through 2021 the MOVE Index averaged 70. But, this was during extraordinary fiscal stimulus and near 0% interest rates. Looking at the 1993 to 2003 period, the average level was 106. See all that in the chart below.

So like most things, what’s “normal” is relative and the current swings in interest rates are probably more common in history, while the previous decade was the actual outlier. I expect bond volatility to stay normally elevated, in the 100 range.

And I expect longer term interest rates to also stay elevated for the first half of 2024. While you’ll see below that I expect a softening economy, which should lead to lower inflation and lower interest rates (and historically have), there are two forces at work that have never been this strong before:

The amount of borrowing the US government needs to do. Based on data from the Treasury, the US will need to re-borrow $2.6 trillion in maturing notes and bonds alone. That doesn’t account for new borrowing needed. And this “supply” comes at a time when normal buyers of this debt are going away. According to the Federal Reserve, the Fed, foreign investors, and US banks were all previously buyers of US debt, without much regard to price, holding around 75% of outstanding US debt at the peak. Today, that is closer to 55%.

The Fed is doing quantitative tightening (QT). For years, they bought treasury bonds to keep rates low and stimulate the economy (aka quantitative easing), owning nearly $9 trillion at the peak. They have started unwinding this, which acts as a headwind to interest rates going lower.

All this is to say, I expect the 10 year to stay within a range of 4% to 5% for much of 2024, even if the Fed cuts rates around the midpoint of the year.

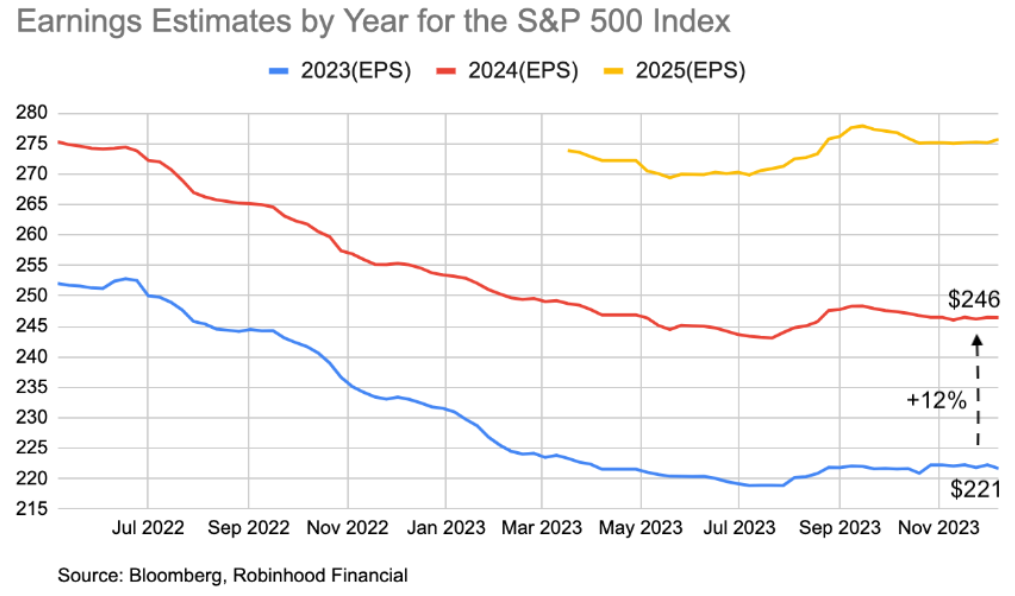

US stocks: 🟡Cautious for now. As I shared in September and above, broadly speaking, I believe the effects of higher interest rates are still making their way through the economy. Add in expectations of higher than average earnings growth (that make it easier to disappoint), wage growth that has stayed solid (keeping labor costs up) and a lesser ability of companies to charge higher prices to their customers due to falling goods inflation and you’ve got a disappointing combination for 2024. In particular because, despite this backdrop, earnings for companies in the S&P 500 Index are currently expected to grow by a healthy 12%, vs the 15 year average growth rate of 6.5%.

Even if you can believe that the earnings expectations are fair, a simple application of a fair valuation multiple of 16 to 18 times (in line with the long term averages) to S&P 500 earnings of $246 per share, gets to an S&P level of 4,000 to 4,430. Since we crossed 4,630 at the time of this writing, it looks like the US stock market is not exactly a deal.

I am currently in the camp that earnings for the S&P 500 in 2024 will be less robust than expected, ending closer to up 6%. And as a result, I believe we could see a correction in US stocks from current levels down to around 4250 in the first half of the year (down about -8%).

But some of my favorite market sayings are “the market is not the economy” and “it’s a market of stocks, not a stock market”. I like them because time and again, I’ve seen individual companies do well in a down market and, typically, the markets get over a slow economy much faster than the economy itself does. The companies we are more focused on with our initially cautious outlook are those that have:

good profitability,

lower than average debt on their balance sheets and

a business that is not easily replicable due to their product, niche or customer base

It’s a combination of quality and growth, but at reasonable valuations. Many end up in tech services. And once a better 2025 comes more closely into view, in the 2nd half of the year, I expect the markets, in a lower short-term rate environment, to rally, breaking the highs of 2021 to 4800.

And by the way, it’s typical to see the markets be more volatile, like I describe above, in an election year.

Thoughts on other parts of the market: This is already long, so I’m gonna summarize my thoughts on some other areas here and use future posts to share more.

Japanese equities: I continue to like the stock market here. After decades of deflation and slow growth, they are having a better go at it. Their central bank expects to soon end their “negative interest rate policy” (NIRP), which they have had in place for many, many years. Of course it’s not without risk as they have one of the oldest populations in the world. You can read more here.

Emerging Market equities: This area includes stocks from countries like China and Brazil. They have been lagging the last few years as higher US rates have hurt their currencies while Covid disruptions lingered. As a result, they have broadly cheap valuations. I see a case for a more tactical, shorter term, trade here as in the near term, they could rally from rate hikes being done in the US and even potential stimulus in places like China. There are still risks there stemming from political differences and the negative effect a stronger dollar typically has on emerging countries. So, it’s not something I am very interested in longer term, right now.

Based on all of this, what is one to do? This may sound boring, but know what your goals are, and especially know your time horizon. If it’s short term (like less than at least 3 years), then looking at higher yielding places to save cash might be the way to go. But if you are investing for the longer term, then being diversified and ready to add more during points in the year may not be a bad idea. Oh and enjoy the rest of 2023, before it’s time to accept the new year.

Risks to this outlook include inflation falling further than expected, interest rates falling faster than expected and corporate earnings doing better than expected.

We expect:

the economy will continue to slow into a mild recession by mid-2024

the Fed will keep rates where they are until June, then cut about 1% during the 2nd half, while the 10 year yield should stay within a range of 4% to 5%

a correction in US stocks down to around 4250 in the first half of the year (down about -8%), but then rally, breaking the highs of 2021 to 4800.