The Labor Day scaries

The Labor Day scaries

As summer comes to an end, a little sadness is understandable. The warmest season in the Northern Hemisphere arrives with excitement for higher temps (initially), swimming, travel, and no school. But the season is fleeting.

Before we know it, sweatshirts will be necessary and winter will be here. But, we’ve still got September. The transition month for not only the weather but also to get back to the grind. The markets and economy are no different.

This week will probably still be a bit quieter. Outside of several “sell-side” conferences, put on by various banks that focus on particular sectors, such as Citi’s Global Tech conference, the calendar is relatively quiet. However, next week there are several moments to watch that could eventually cause volatility in markets and sentiment.

September 12: The House is back in session and they have quite a bit to do, particularly around the budget, which is not fully worked out yet.

September 13: The August US CPI drops. With the rise in oil prices over the last month, it’s expected headline inflation, which includes energy and food prices, will be higher—but core prices, that exclude these categories, will fall. The latter is what DJ Powell cares more about when making interest rate decisions.

September 14: The United Auto Workers contract is set to expire, which means the auto companies could be seeing a labor strike in their future.

This is on top of the fact that September is just historically not a great month. While that is not a hard and fast rule, an investor can keep that in mind.

The other thing to keep in mind is the current consensus narrative (aka sentiment or vibe):

The US economy has absorbed interest rate hikes by the Fed fairly well and it seems a near term recession is likely not in the cards.

The drivers of falling inflation so far—falling oil prices, improvements in supply chains—are likely done. Without them, it’s now more important that shelter/housing prices and the cost of “core services” starts falling.

For shelter, most look at more real-time data such as from Zillow and believe this is already in play. Even if it doesn’t feel like it everywhere across the country. The services piece falling is a risk and really relies on employment and wage growth softening. Last week’s employment report showed we are heading that way. Wages were a touch lower and unemployment a bit higher (3.8% from 3.5%), stemming from increased participation. This is the most positive way you can see a higher unemployment rate—from more people looking for a job.

So I am of the mind that the Fed is done hiking.

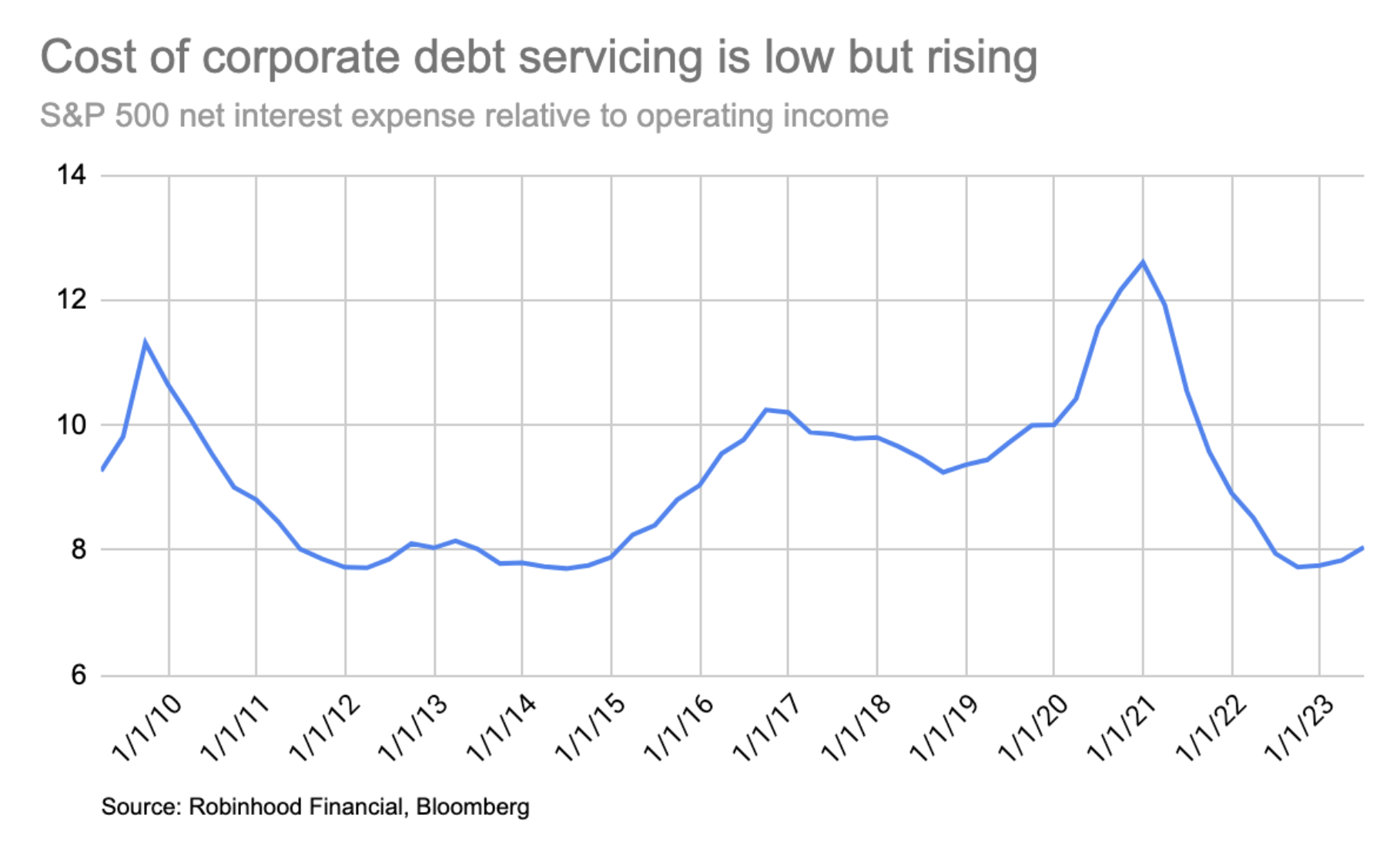

But with consensus still sort of positive on the economy, I am keeping my senses up. The markets often fall when expectations are better than reality. Of note, interest rate hikes have lagging effects depending on where you look. Eventually, companies’ borrowing costs will be reset higher, as their bonds mature and they issue new ones. The chart below shows the cost for the average company in the S&P 500 to “service” their debt relative to their income, since 2009.

The same goes for commercial real estate loans (already in play) and consumer debt (car loans, mortgages). Oh, and the US government as well.

This all means the growth we’ve continued to see, and the falling inflation we’ve experienced so far could be faced with some headwinds in the future. There is still a chance we make it through… but this week’s Monday scaries wouldn’t let me consider that.