Sell in May and go where?

Sell in May and go where?

With the debt ceiling nearly out of the way (a deal struck last weekend so now it has to go through Congress), I heard someone say “that was a close shave.” I immediately pictured a barber with a razor and started thinking about the other sayings we use. “Bigger fish to fry,” “no pain, no gain,” and “living rent free,” among many, help us succinctly communicate meaning. They work because they quickly conjure up a mutually understandable picture or feeling.

But where did they come from? The origin depends on how old they are. New phrases can be traced back to just a few years ago, typically from social media. Older ones are often misattributed because they originated too long ago to know the exact person or publication it started with.

One such market-related version of a common saying is “sell in May and go away.” Where did that start? Is there merit to it? And if you do act on it, do you ever come back?

I did some research on this and found that its origins could be traced back to the wealthy stock market participants in the UK from centuries past. In fact, the second part of that phrase is “...come back on St. Leger’s Day,” referring to a horse race. The St. Leger Stakes, which started in 1776, is a well-known horse race in England, like the US’ Kentucky Derby, taking place in mid-September every year. The adage references how British investors, aristocrats, and bankers would sell their shares in May, relax and enjoy the summer months “on holiday,” and return to the stock market in the Fall, after the St. Leger Stakes. The phrase has since been widely adopted in the US for years—as some investors forgo investing between Memorial Day and Labor Day.

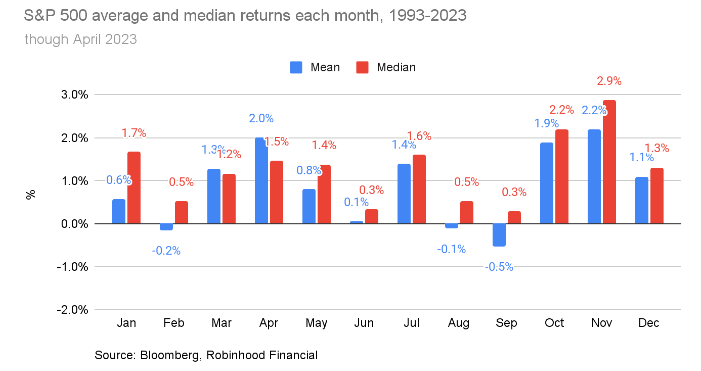

Looking solely at the historical S&P 500 data, it’s not just folklore. We gathered the average and median returns of each month of the year, going back 20 years (to 2003), and since I tend to be skeptical, also 30 years (to 1993). We found the summer seasons do tend to make up the smallest percentage of a calendar year’s return (for the 30 year period, the average returns from June through September were only 8% of the average calendar year return), and the worst average month was September.

However, we also observed that July was a historically strong month. While the 20 year chart looks a little different, the conclusions are directionally the same.

Taking the data at face value though, assuming you want to buy low and sell high, a more accurate statement could be “sell in July and go away, come back after Labor Day.” Of course, it doesn’t fully rhyme so it’s less catchy.

For those that believe in efficient markets, this observed anomaly is tougher to explain. The reasons for it are often chalked up to rampant portfolio rebalancing in June and September. In addition, some leading stock indices are rebalanced around these times, creating trades without investment reasoning—both of which tend to force sales of stocks that have gone up in value and buys of stock that have not (all else equal). Or perhaps, spring weather drives optimism that doesn’t continue in the summer months. I know from my own anecdotal experience that vacation schedules, particularly in August, have led to less trading volume and liquidity, which can easily weigh on share prices, or create lackluster markets at best.

But if one does choose to consider this strategy, there are other factors to know. They include:

The need for perfect timing: The trouble of selling everything and going back in is the need for the right timing on both sides. It’s not just one decision, it’s two (sell and buy), which means you have to get both right to make it all work well.

The nuisance of taxes: If you sell a stock or portfolio that has gains in it, you will realize these gains, which could lead to an unpleasant tax bill the following year. This could wipe out any benefit good summer investment timing may have provided. And if so, you might as well have stayed invested. One could look to this strategy in their retirement account, but that’s really a place where getting invested in a diversified way, and staying invested for the long term, is best suited.

So while there is something to this market adage and approach, it’s not right for everyone, or necessarily in every year. But it can be fun to say, just like “buy the dip” and “the trend is your friend” are, or my personal favorite—because it applies to so many things in life—“better late than never.”