What is a Money Market Account?

A money market deposit account is a type of bank account that combines the flexibility of a checking account with the interest-earning power of a savings account.

🤔 Understanding money market accounts

Money market accounts combine features of checking and savings accounts. They’re more flexible than a savings account, but they also let you earn more interest than a checking account. To compensate, they typically have higher minimum balances. They are primarily designed for people who have larger amounts of money to deposit, but who need more flexibility than a savings account.

Let’s use the fictional Neighborhood Bank as an example.

Neighborhood Bank’s checking account has no minimum balance and offers .10% interest on balances under $10,000. Balances over $10,000 earn .5%. The bank’s savings account has no minimum balance and offers 1.75% interest regardless of the balance. The money market account offers .90% on balances up to $15,000 and 1% interest on balances over that amount. Neighborhood Bank charges a $25 a month fee if your money market account balance falls below $5,000.

On top of the interest rate, the money market account comes with a debit card and checking account that you can use to access your cash easily. Neighborhood Bank’s savings account doesn’t offer the same flexibility. Instead, you’d need to move your money to a checking account to access it.

Takeaway

A money market account is like a hybrid car…

Like a hybrid car combines aspects of gas-powered and electric vehicles, money market accounts combine aspects of checking and savings accounts.

New customers need to sign up, get approved, and link their bank account. The cash value of the stock rewards may not be withdrawn for 30 days after the reward is claimed. Stock rewards not claimed within 60 days may expire. See full terms and conditions at rbnhd.co/freestock. Securities trading is offered through Robinhood Financial LLC.

- What is a money market account, and how do they work?

- What are the pros and cons of money market accounts?

- Can you lose money in a money market account?

- How do I know if a money market account is right for me?

- Is a money market account a transaction account?

- What are the alternatives to money market accounts?

- Where can I get a money market account?

What is a money market account, and how do they work?

A money market deposit account is a type of bank account that offers aspects of both checking and savings accounts. They’re generally designed for people who have larger balances that they want to use to generate interest while retaining the flexibility to make purchases as needed.

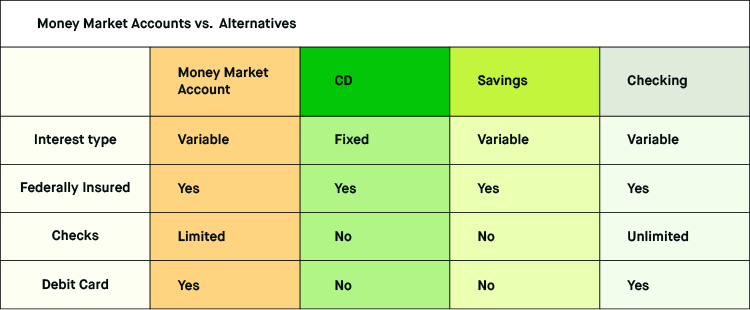

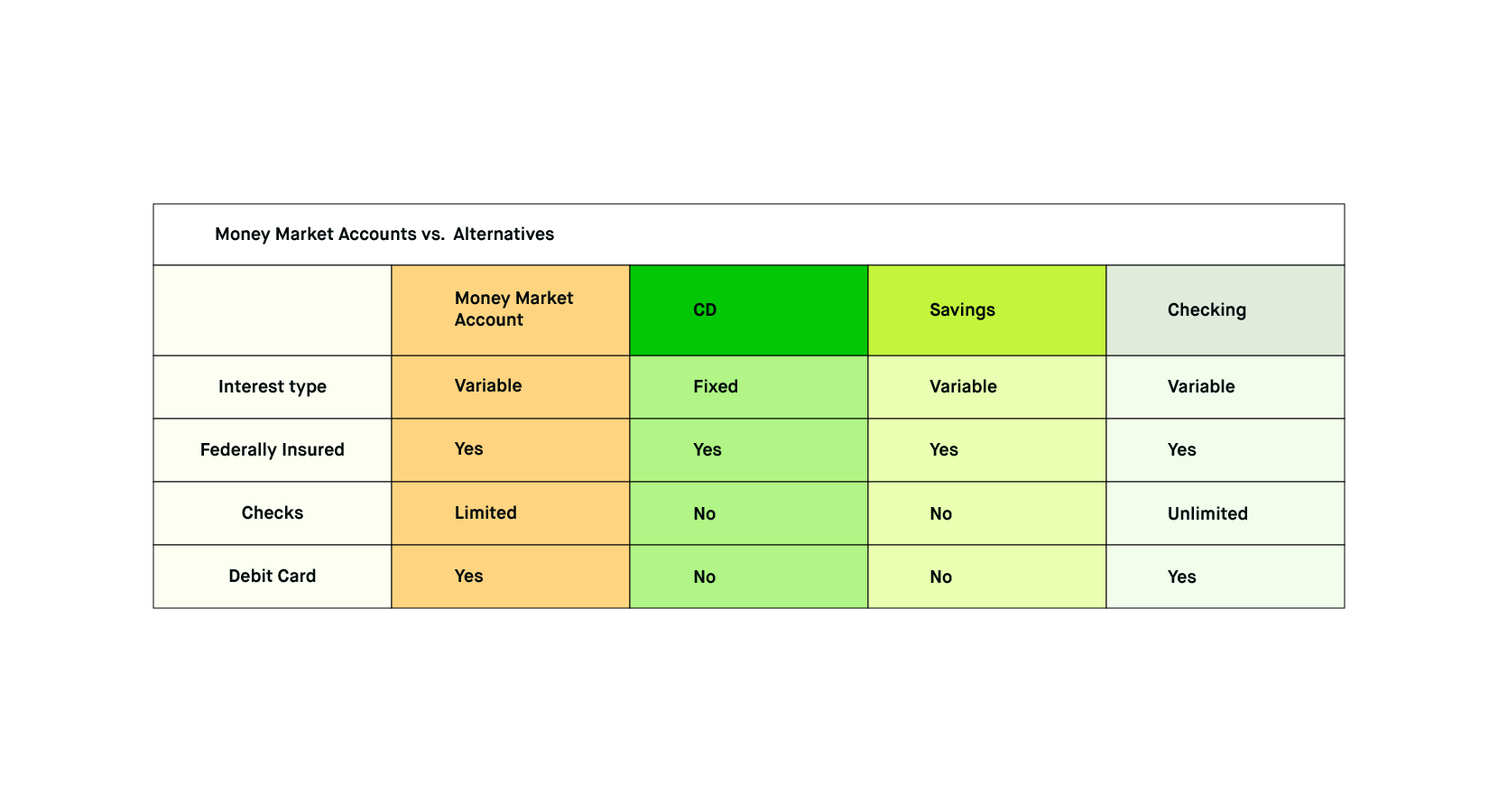

You can open the account with your financial institution of choice, whether it be a bank or credit union. You can make deposits in-person or online, through your phone, or at an ATM. Most money market accounts also give you a checkbook and debit card that you can use to make purchases.

Money market deposit accounts are insured by the Federal Deposit Insurance Corporation (FDIC), up to $250,000 per depositor per bank.

It’s important to note that a money market deposit account isn’t the same as a money market mutual fund. While a money market deposit account is secured by FDIC insurance, a money market mutual fund is a type of investment, and therefore isn’t FDIC-insured. Some banks sell money market funds in addition to money market deposit accounts, so it's important to understand which it is you're buying.

What are the pros and cons of money market accounts?

Pros: The benefit of money market accounts is that they combine many of the best features of checking and savings accounts.

Savings accounts are useful because they pay interest on the money that you deposit. That helps you grow your balance over time, even if you don’t make deposits.

Checking accounts are useful because they make it easy to spend your money when you need to, whether it be by check or debit card or online payment.

Money market accounts offer interest, so the balance that you deposit will grow. They also make it easy to spend and transfer your cash.

Cons: The drawback of money market accounts is that they don’t accomplish each task as well as a savings or checking account does individually.

Savings accounts tend to offer higher interest rates than money market accounts. That makes them a better place to store extra cash that you don’t need to spend in the immediate future.

Money market accounts also place restrictions on withdrawals and transfers that don’t exist for checking accounts, making them less flexible.

Other major cons of money market accounts are their minimum deposit requirements and fees. Many banks require minimum deposits in the thousands of dollars if you want to open a money market account. They also tend to charge higher fees than other types of bank accounts.

Can you lose money in a money market account?

Money market deposit accounts, like other bank accounts, are insured by the Federal Deposit Insurance Corporation (FDIC). The FDIC offers insurance for up to $250,000 per depositor per bank

If the bank that manages your money market account goes out of business, the FDIC will reimburse you for any lost money up to the $250,000 limit.

It’s important to remember that this insurance covers money market deposit accounts, not money market funds. Despite their similar names, money market deposit accounts and money market funds are different — and money market funds aren’t insured. Money market funds are mutual funds that hold short-term securities, like Treasury bills. They rarely lose value but are not 100% safe and aren't FDIC-insured.

How do I know if a money market account is right for me?

Banks usually design their money market accounts for a particular type of customer. If you have a significant amount of cash, a money market account might be a good choice for you. Money market accounts give you the chance to earn interest on your money while retaining the flexibility to make large purchases when you need to.

Having a large balance may also help you avoid the minimum balance requirements and fees that most banks charge for money market accounts.

If you don’t have a large amount of cash or don’t need the flexibility to make large purchases, you probably don’t need a money market account.

Is a money market account a transaction account?

Yes, a money market account is a type of transaction account. It is designed for easy spending and transfers of cash. To that end, most money market accounts offer checks that you can write against the account and a debit card that you can use for purchases or ATM withdrawals.

Unlike most checking accounts, money market accounts are limited in the number of transactions that you can make in a month.

What are the alternatives to money market accounts?

Money market accounts combine aspects of checking and savings accounts, so they are the most obvious alternatives.

To replace a money market account, you may want to open both a checking account and a savings account. You can put enough money in your checking account to cover expected, near-future expenses. The rest of your money can go to your savings account to earn interest. Having two accounts will complicate the management of your money slightly, but can help you avoid the fees and minimums that most money market accounts impose.

Where can I get a money market account?

Most banks and credit unions offer money market accounts alongside their checking and savings accounts. If you already have a bank account, it’s worth checking with your bank to see if it offers money market accounts.

If you don’t mind opening an account at a new bank, you might want to look at online money market accounts. Online banks sometimes have lower minimum deposit requirements and charge lower fees than brick and mortar banks. Given that money market accounts are known for high minimums and fees, avoiding those can eliminate some of the significant drawbacks of the accounts.

New customers need to sign up, get approved, and link their bank account. The cash value of the stock rewards may not be withdrawn for 30 days after the reward is claimed. Stock rewards not claimed within 60 days may expire. See full terms and conditions at rbnhd.co/freestock. Securities trading is offered through Robinhood Financial LLC.