What is Subrogation?

Subrogation is when one party (usually an insurance company) claims the legal right of another party to seek reimbursement for losses they have paid.

🤔 Understanding subrogation

Subrogation is a legal right held by entities such as insurance carriers to recover their loss for damages caused by a third party. After compensating the insured for damages under the insurance policy, the insurer can try to recover their own losses. Subrogation allows them to step into the shoes of their policyholders and grants them the same legal rights as the injured party to pursue a loss. Many insurance policies include a subrogation clause, where you give your insurer permission to file such a lawsuit. Insurance companies take on a certain amount of risk with each customer they take on, and subrogation is one way they balance out that risk.

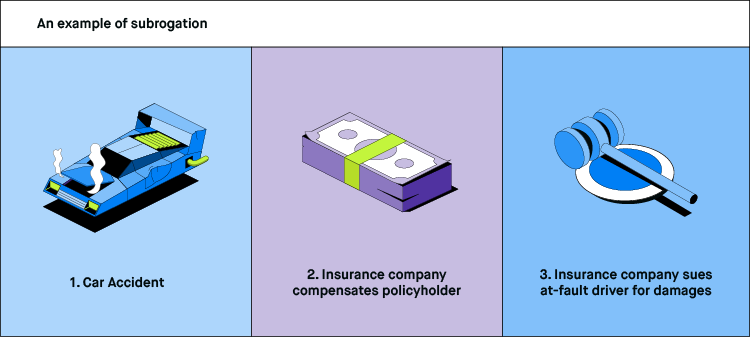

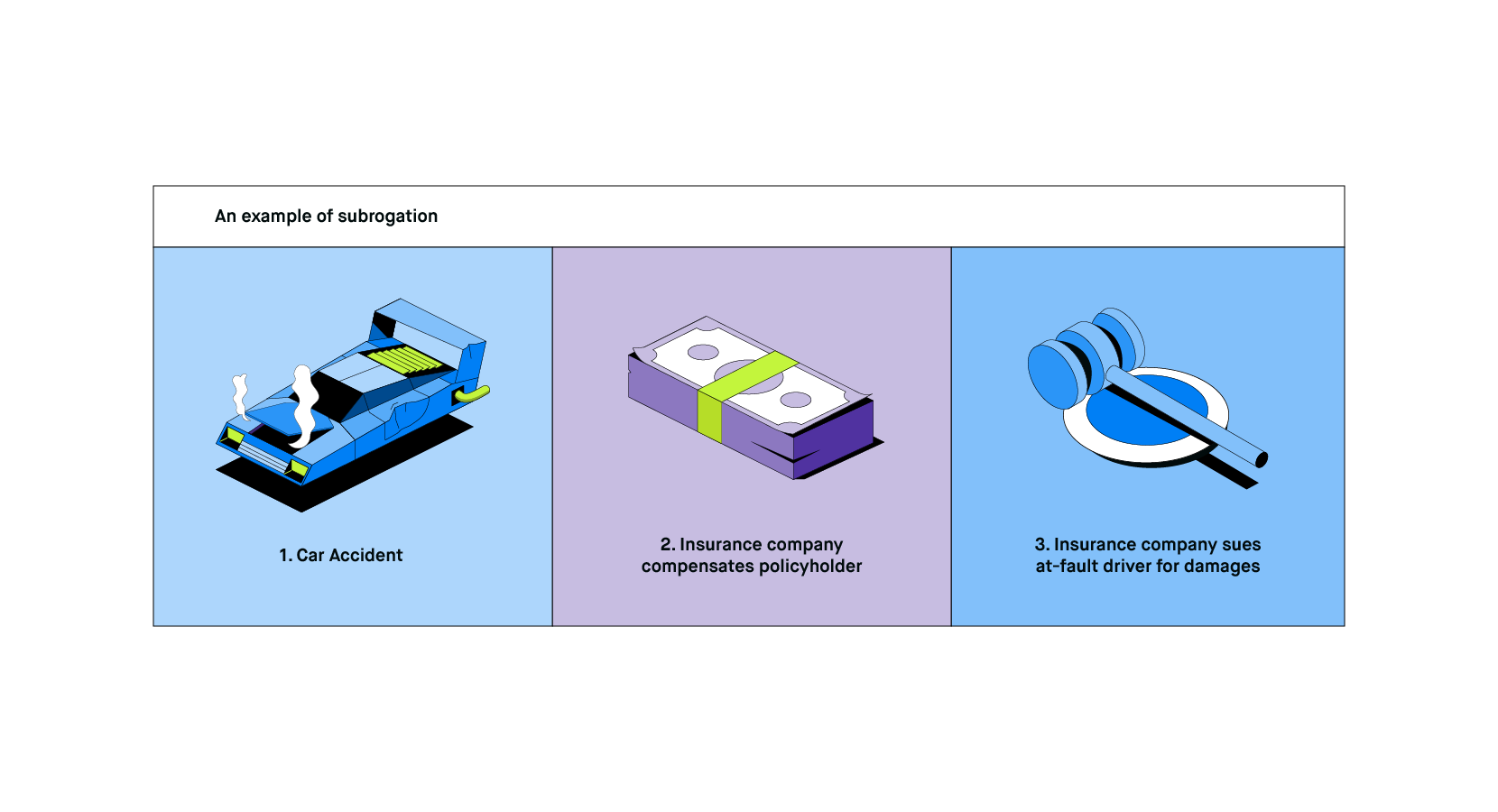

Let’s say you’re in a car accident. Your car is totaled, and your insurance company pays you $20,000 to replace your vehicle. A driver running a red light caused the accident that totaled your car. After compensating you, your car insurance company uses their right of subrogation to sue the other driver (or more likely their insurance company) to recover the insurance company’s lost $20,000.

Takeaway

Subrogation is like an insurance policy for insurers...

Your insurance compensates you in case of a loss, but subrogation gives them the right to recover their own losses if someone else should really be liable for the incident in question.

New customers need to sign up, get approved, and link their bank account. The cash value of the stock rewards may not be withdrawn for 30 days after the reward is claimed. Stock rewards not claimed within 60 days may expire. See full terms and conditions at rbnhd.co/freestock. Securities trading is offered through Robinhood Financial LLC. Futures trading offered through Robinhood Derivatives, LLC.

How does subrogation work?

The subrogation process usually begins when an insurance company compensates a policyholder for a loss the policyholder incurred at the hands of a negligent third party. The insured has filed a claim, and the insurer has fulfilled their end of the bargain by paying them.

But because the loss was the result of a third-party and not the policyholder, the insurance company seeks reimbursement from the at-fault party.

The subrogation process typically occurs between the insurance company of the person who incurred the loss and the insurance company of the person who caused the loss. In cases where the at-fault party doesn’t have insurance, the process would occur between the insurance company of the party who incurred the loss and the person who caused the loss.

Here are some examples of the types of insurance policies that might include a subrogation clause:

- Car insurance: Subrogation occurs when an auto insurer pays for an accident that was the fault of the other driver, not their policyholder.

- Health insurance: Subrogation occurs when a health insurance company pays for the medical bills for an injury caused by dangerous or defective products.

- Liability insurance: Subrogation occurs when the insurance company pays for a liability claim, and it is later determined that fault did not lie with the policyholder.

- Property insurance: Subrogation occurs when an insurance company pays for damage to property when a third party caused the damage.

- Workers’ compensation: Subrogation occurs when someone files a workers’ compensation claim for an injury that was due to another party’s negligence.

The subrogation process for the insured

If you’ve been in an accident where you weren’t at fault, and your insurance has compensated you, there’s not much you’ll need to do for the subrogation claim.

In this type of situation, you’ve already recovered your losses. Now your insurance company is trying to recover their losses.

The subrogation process primarily involves just the two insurance companies (or the insurance company and the negligent third party, if the party doesn’t have insurance).

You might still hear from either your insurance company or the insurance company for the third party if they need to hear your side of the story.

One other situation that can arise is if an insured party chooses to sue the third party themselves — the insurance company can then claim part of any cash settlement as part of their right of subrogation.

Waivers of subrogation

A waiver of subrogation is a contract that waives the right of an insurer to try to recover their losses when a third party is at fault.

This type of waiver is common in a construction contract or a lease. An insurer would also likely charge you an extra fee if you’ve signed this type of waiver because it puts them at a higher risk of losing money in the event of an insurance claim.

If you sign a waiver of subrogation, you sign away your right to seek damages from another party. But you’re also signing away your insurer’s right to seek damages in your place.

Why is subrogation important?

As a consumer, you might be wondering why subrogation is important and why you should care about it. After all, the subrogation process begins after you’ve already recovered your losses. So how does this benefit you?

Subrogation isn’t just financially good for insurance companies. It’s generally good for policyholders, too.

Insurance companies (and companies in all industries, for that matter) often pass their expenses along to consumers. So if insurance companies aren’t able to recover their costs when a third-party is at fault, they would pass those extra costs onto their policyholders.

So really, subrogation makes insurance cheaper.

How long does insurance subrogation take?

The amount of time it takes to settle a subrogation claim can vary quite a bit from case to case.

In very straightforward cases where the at-fault person (or their insurance company) agrees to accept fault, subrogation claims can wrap up within 30 days or so.

For more complicated claims, the process can take years. This might be the case if the parties disagree about what happened and there’s no way to prove fault one way or the other.

If the parties can’t settle the issue themselves, the situation might require litigation (where one party takes legal action against the other).

What happens if a subrogation claim is ignored?

If an insurance company is making a subrogation claim, they’ll either make a phone call or send a letter to the negligent third party (or, more likely, their insurance company).

If someone ignores a subrogation claim at first, the insurance company seeking recovery of damages will probably continue to reach out and send subrogation letters.

But if someone is facing subrogation for an accident they caused, they shouldn’t expect the insurance company to go away if they ignore them.

Eventually, depending on the amount of money in play, the insurance company might file a lawsuit against the negligent party or their insurance company.

If the case does end up in a lawsuit and the party being sued doesn’t believe they’re at fault, they’ll have the opportunity to prove that in court. Otherwise, they very well might end up having to pay damages.

How do I handle a subrogation claim?

If you’re found to be at-fault in an accident, it’s possible to end up with a subrogation claim against you. If the insurance company has paid out for a claim from their customer, they may come after you to recover their losses.

If that happens, you’ll receive a letter or phone call informing you of the subrogation claim.

These subrogation claims are most often handled between insurance companies, meaning your insurer might handle things on your end.

If you don’t have insurance, though, the claim will be against you directly. In that case, you’ll have to either prove that you weren’t actually at fault or you’ll have to pay the subrogation damages.

What subrogation mistakes should I watch out for?

Subrogation is a necessary process for insurance companies if they want to recover their loss for claims that were the fault of a negligent third party and not their policyholder. And despite the financial stakes at play, insurance companies make mistakes. Let’s talk about some of the most common mistakes companies make when it comes to subrogation.

- Waiting too long: There are statutes of limitations associated with certain types of claims, such as many auto and personal injury cases. If an insurance company waits until the statute of limitations has passed, they probably won’t be able to recover their damages.

- Ignoring third-party liability: There might be a situation where an insurer ignores or fails to recognize the fault of a third party when a policyholder files a claim. This means lost money for the insurer, and possibly for the insured.

- Failure to prove subrogation: It is up to the insurer seeking subrogation to prove that the third party was negligent or at-fault. Sometimes, especially when the other party denies fault, this takes some investigation on the part of the insurer. And sometimes they fail to do a sufficient investigation.

- Not knowing about a waiver of subrogation: Remember those waivers of subrogation we talked about earlier? Not being aware of such a waiver could cause an insurance company to spend money on subrogation efforts needlessly.

New customers need to sign up, get approved, and link their bank account. The cash value of the stock rewards may not be withdrawn for 30 days after the reward is claimed. Stock rewards not claimed within 60 days may expire. See full terms and conditions at rbnhd.co/freestock. Securities trading is offered through Robinhood Financial LLC. Futures trading offered through Robinhood Derivatives, LLC.