Our 2023 outlook so far

Our 2023 outlook so far

The older you get, the more you realize many events should probably be taken with a grain of salt. In fact, the Zen teaching, where the response to every statement about an event is “we’ll see,” feels the most fitting these days. The point of the teaching is to be careful labeling something good or bad too quickly. Sometimes what seems bad at first is good in the long run, and vice versa. This has stuck with me — in life and markets.

In December, I laid out an outlook for 2023 — and then said “we’ll see.” Now that the first full quarter is nearly over, I reviewed what I thought at the time, to see if it’s changed (and what’s taken place). Here’s a summary of this exercise:

We believed there would be more evidence of a recession in the US. This included growing softness in the broad employment numbers. In addition, we expected more areas that previously benefited from 0% rates, but are struggling now in a higher rate environment, would be revealed. Lastly, we believed earnings expectations for 2023 would come down materially, helping valuations. And given all of this, we expected equity markets to potentially flirt close to the 2022 bottom again some time in the first half.

What I think now:

Employment numbers have remained relatively strong, though I still think they could begin to soften. That said, unemployment is low enough that it may not be felt as much in this recession versus other areas (see next point).

Areas that benefited the most from 0% rates and quantitative easing (QE) are already seeing some smoke — particularly in the commercial real estate sector. A related impact is the failure of several US banks and the risk management of their balance sheets (see last week’s note).

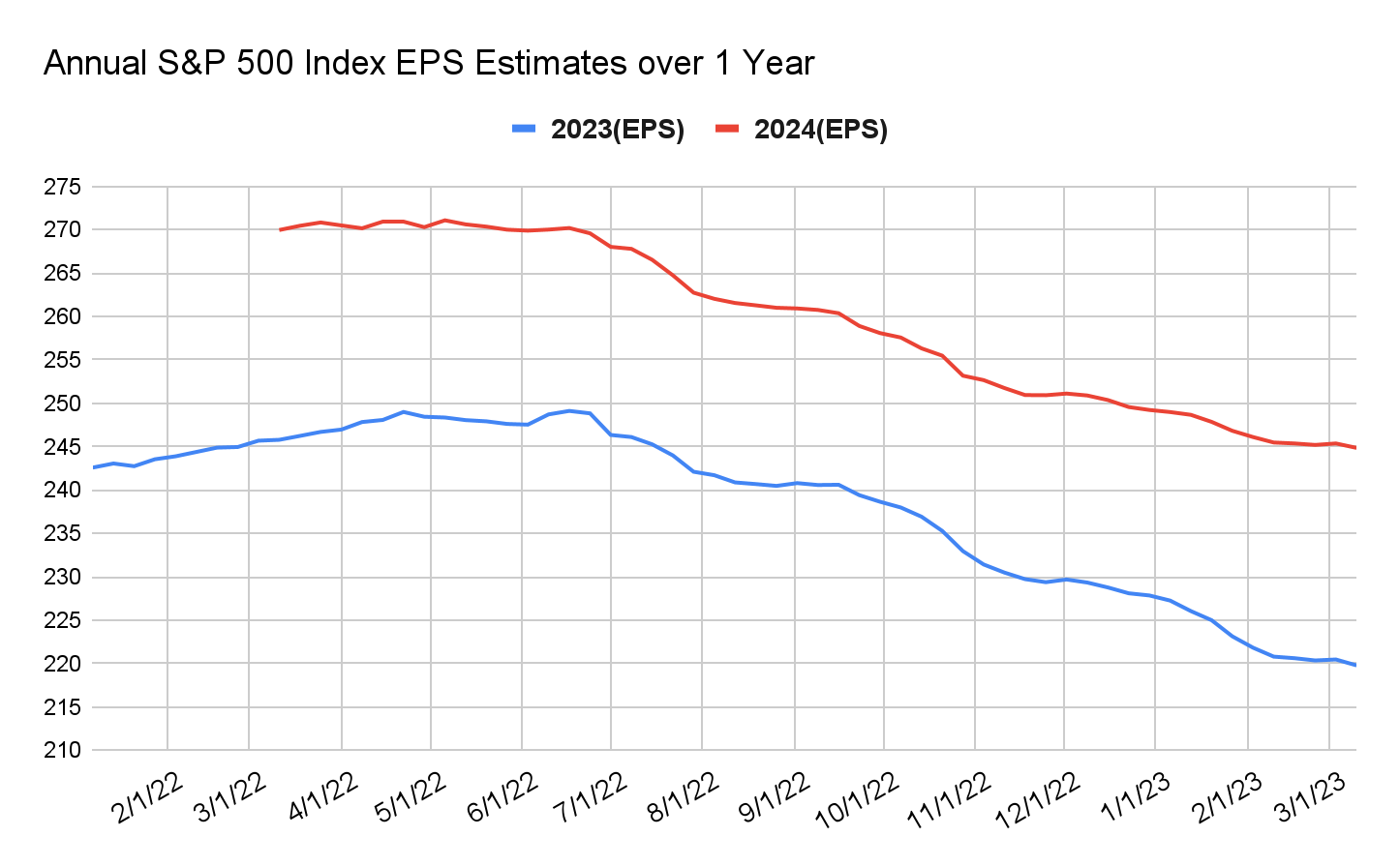

As for earnings expectations, they have fallen and are much closer to our own top-down estimates. By next quarter though, 2024 earnings will start to come into view and that’s expected to be decently higher — higher than I think it should be.

To see what I mean on earnings, here is a chart of S&P 500 aggregate earnings expectations: They are currently estimated to be around $220 per share, and while we think they should be closer to $215, they have come down a lot, as you can see (in blue). 2024 earnings, in red, are expected to be nearly 14% higher.

After January’s strong markets, when the S&P had touched over 4200, it seemed nearly impossible to get closer to 2022's lows. But, it was largely driven by technicals (like buying after tax-loss harvesting in December and short covering) rather than a sustainable bullish sign. Since then, the broad markets have dropped from their highs, so it still seems possible, before stabilizing later this year. That being said, the market has been pretty resilient around the 3900 level on the S&P.

We believed US interest rates and inflation would moderate, with the 10-year Treasury rate averaging around the 3.5% mark (3%-4% range) and, relatedly, the US dollar would soften further. Because of this, we believed (investment grade) bonds could go back to doing what they have done in prior economic slow downs, behaving generally more stable than equities and providing some income through interest.

What I think now:

This has played out, with headline inflation continuing to show that it peaked in June 2022 and core inflation (less food and energy) peaking in September 2022. In addition, the 10-year has ranged around 3.5% to 4% since the year started. As of March 21, it is around 3.55%.

Equally, the US dollar has weakened since we made the call, though with some ups and downs.

The Fed will have their next meeting later today. Given all the stress in the banking sector, the market is pricing a toss up on whether they raise rates or not and is now expecting several cuts by year end -– quite a shift from just a couple weeks ago when it expected several more hikes. Irrespective of what they do at this next meeting, more interesting is what they say about the future path of rates. Will they suggest they will keep them around these levels for longer, given inflation is still tracking well above their 2% target, or hint at cutting to alleviate recent stresses? We think the former is still possible at the next meeting. Decisions beyond that still depend on how wide the bank issues spread to other facets of the economy — and whether the banks tighten financial conditions on their behalf… which is very possible.

Looking abroad, we believed Europe would also experience a recession — driven by the reliance on Russian energy.

What I think now:

While we look to be right on Europe showing signs of slowing down, it’s not because of energy supply. Europe was able to save enough for the winter, which also turned out to be mild. They still have inflation and, as a result, their interest rates are increasing to slow the economy. In addition, their banks have also experienced some issues — namely Credit Suisse, which has been assumed by UBS.

Further East, we believed China would rally on its re-opening from Covid restrictions, but not without some swings as the government waivers between supporting the economy and their health care system.

What I think now:

This played out as such — with Covid spreading quickly and straining their healthcare system. This has passed though, and the country looked clear to rise to a recovery. However, this has been overshadowed by their relationship with Russia and other potential political issues (like Taiwan). We still believe this could be an attractive region but are starting to fear that Xi’s presence and decisions could limit the country’s potential. Thus, we are less bullish than we were.

And we would repeat how we closed our outlook: As the year progresses, we believe the market, as it often does, will begin to look beyond the headwinds to eventual improving growth. In all but one of the last eight recessionary environments, going back to 1970, the market started looking ahead to better days about four to five months before the economic data proved it was no longer getting worse. As a result, we expect a more attractive equity market sometime in the second half of 2023.

But, as the Zen teaching would say, we’ll see.