Are you certain?: It might be time for a market breather

Are you certain?: It might be time for a market breather

In a hundred different small ways, life showcases its tendency to pivot you regularly. Often these are fractional shifts that require a level of awareness most of us don’t have at any given moment. One morning, you might be in a rush to grab coffee and train it to work, while the person in front of you is moving slowly. So you end up ditching the coffee to make the train. Other times unplanned changes happen to someone right in front of you—like the broken ankle my opponent suffered while playing tennis recently. The game went on, but not for the injured. In any one of these, it’s easy to simply get on with it, as if they didn’t happen.

As the new year has begun, I wondered—what if I chose to stop for a moment and look for the shifts that happen? And apply them to my own level of awareness—maybe even feel some gratitude for receiving a reminder that nothing is certain?

Coffee would have kept you a little more awake after a rough night’s sleep and that tennis player planned to walk home to leave her car for a family member. Logically, we know nothing is completely certain (except maybe taxes and our eventual demise). Yet we as humans still operate in certainties.

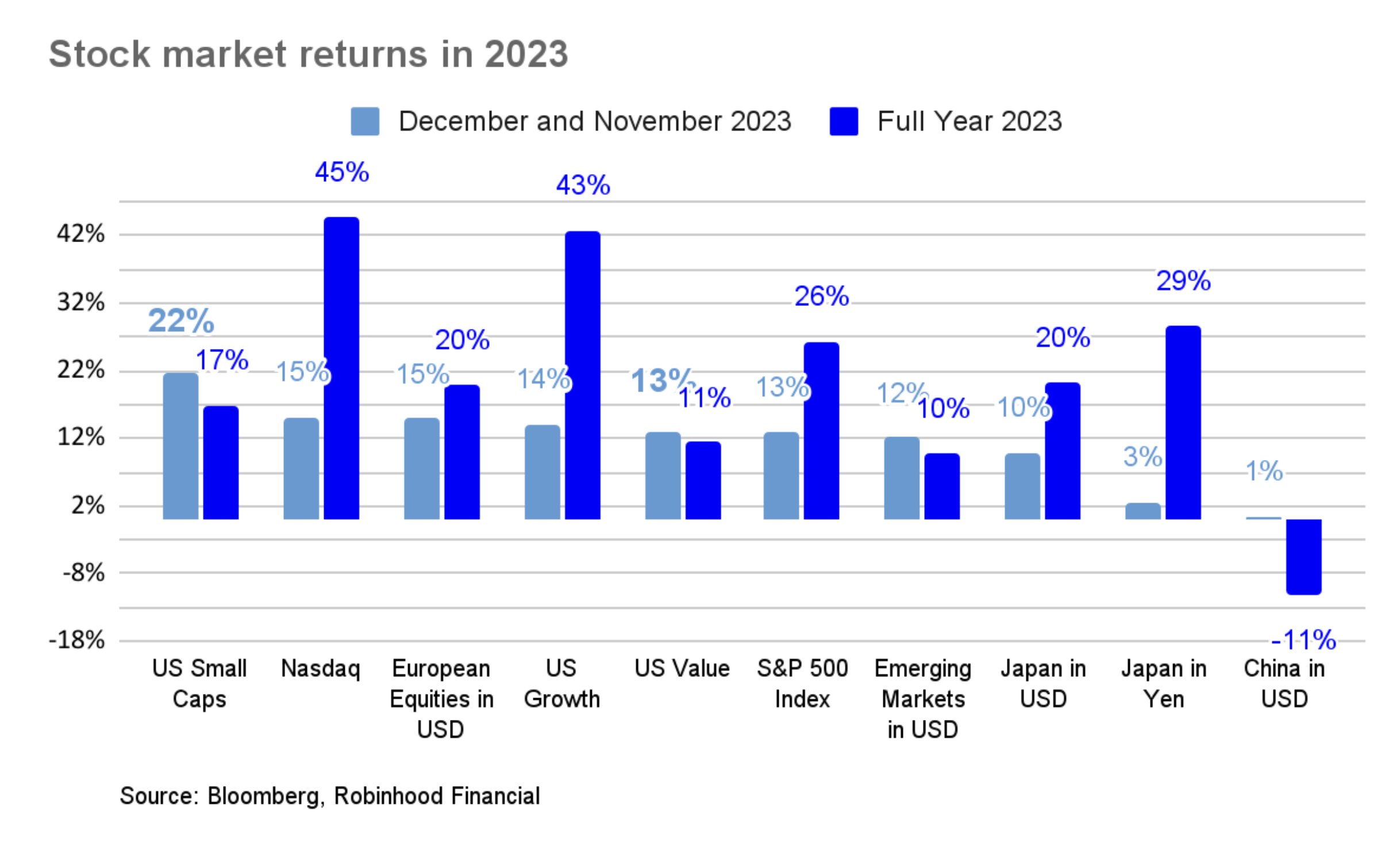

And the market can as well. The months of November and December 2023 were a perfect illustration of this in US markets. Stock markets rallied across the board in certainty that the US will stick a pillow-soft economic landing in 2024, while maintaining strong corporate profits and experiencing falling interest rates. Take a look at different stock markets, sorted by returns in the last two months:

The year-end exuberance was not completely unfounded. The December Fed meeting confirmed the end to rate hikes and also alluded to 0.75% of rate cuts in 2024 through their Summary of Economic Projections. This shift provided a boost to stock market valuations and expectations for the economy and particularly impacted US value and small cap stocks. These are stocks that tend to rely more greatly on a good economy, and each rose in value, just in the last two months of the year, by more than 100% of their 2023 return (denoted in bolded light blue above).

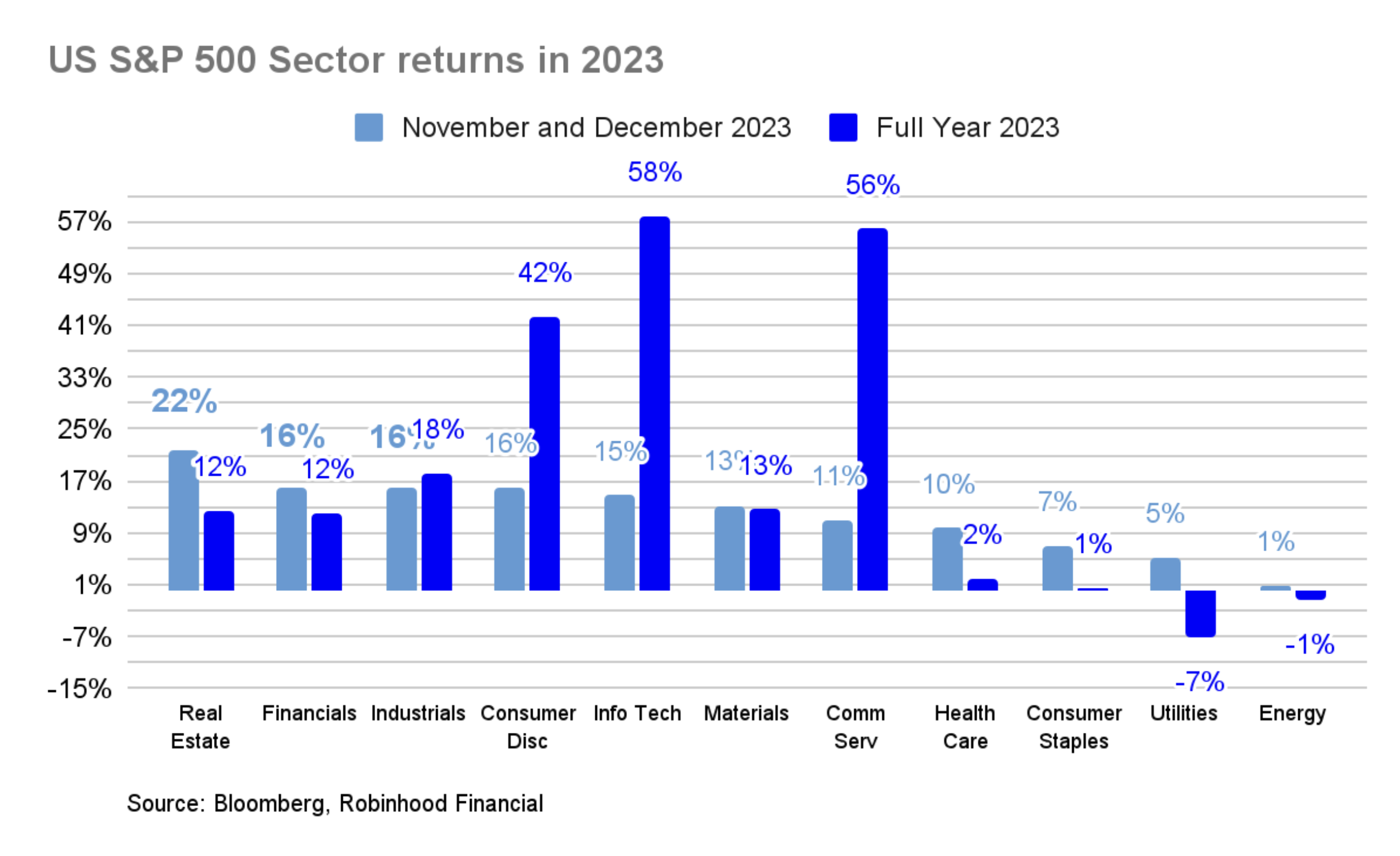

Markets took this signal from the Fed and ran with it. It’s now pricing in a 2024 year-end median fed funds rate of around 3.9%, suggesting over 1.4% of rate cuts next year. And with this move in market expectations of interest rates, the sectors of the market most sensitive to movements in interest rates really rallied—like real estate, financials, and industrials. You can see below (in bolded light blue) how many sectors earned more than 100% of their 2023 return in the last two months of the year.

I believe US markets now fully reflect a nice and certain 2024 (or at least first half), leaving little room for something to not live up to it. As a result, I expect some consolidation in the broad markets this quarter. In fact, I wouldn’t be surprised if there was a correction of 5-7% in the next month or so.

For example, if one takes the following current market expectations as certain:

Soft economic landing with GDP growth lower but solid at 2.3%

Unemployment rate in 2024 remains low at 4.2% (last reading was 3.7%)

Wage growth stays around 4%

Core CPI continues to fall to 2.6% (closer to the 2% Fed target) from 4% today

Fed funds rate ends the year at around 3.9% from around 5.3%

Earnings growth of the average S&P 500 company at 12% for 2024 to $264 per share

A slightly generous 18x valuation multiple is fair (10 year average is 17.6x)

And if you apply this math of certainty ($264 x 18), you get to a “fair value” of the S&P 500 level at around 4,752. Compare this to the S&P 500 closing level for 2023 of 4,770, and it doesn’t look like there’s much room for appreciation.

Since we know nothing is certain, and there are many risks out there, I believe the pace of returns should slow; there is still macro uncertainty (geopolitical tensions, lower inflation impacting earnings, an election year) and there will be volatility in economic data.

There is one thing I have gained certainty in—or maybe just confidence. That is, a stock picker’s market is possible again now that we have interest rates well above zero again. No matter whether the Fed lowers them in 2024 (we think they will), it’s unlikely they will go back to zero anytime soon.

That is meaningfully different vs. the 2009–2021 period, when the best option was generally to buy an index and enjoy.

Welcome to 2024, and beyond. P.S. Here is a quick rundown of near-term market events to watch:

1) the Fed Reserve minutes from their last meeting (Wed 1/3 at 2 PM ET);

2) the December US jobs report (Fri 1/5 at 8:30 AM ET);

3) the US CPI for Dec (Thurs 1/11);

4) the start of the Q4 earnings season (the banks kick it off Fri 1/12 before the open).

Source: Bloomberg, Robinhood Financial. Growth, Value and US Small Caps represented by the Russell 1000 Growth, Russell 1000 Value and Russell 2000 Total Return Indices, respectively. European Equities represented by the MSCI Europe Total Return Net Index, Japan represented by the MSCI Japan Net Total Return Index. Emerging Markets represented by the MSCI Emerging Market Net Total Return Index. China represented by the MSCI China Net Total Return Index. All returns in USD unless otherwise noted.