Advice for your future

Advice for your future

“Make your bed every morning,” they say. This advice scrolled past me on social media in a widely distributed speech to a graduating class of college students. Touted as a way to start a day off with initial purpose and accomplishment—that should put one on a path for a life full of achievements.

I was fortunate to learn how to make an ace bed from a professional. After coming to this country, my grandmother was part of the housekeeping staff at a high-end hotel. She made her bed every day and taught me how to fluff pillows and fold sheets to perfection. I think of her every morning as I pull my comforter up and straighten it.

But something that crossed my mind one morning was how equally, if not more, important advice would be to save for your retirement every day. Why don’t speeches to graduating classes say that too?

It’s no secret that the current public infrastructure for funding a retirement is dissipating. Social Security is funded by the income of current workers and the Old-Age and Survivors Insurance Trust (OASI). Together they fund the payments to current retirees who also put into the system while they worked. Given the growing number of people retiring vs. contributing and inflation, the trust is expected to be fully spent down by 2033. After that, Social Security will only be able to pay out 77% of scheduled benefits for retirees, according to the plan.

It is time to take matters into our own hands. Retirement accounts—individual retirement accounts (IRAs), employer-sponsored 401ks and others—were made to facilitate saving and investing for retirement. They allow for tax-deferred or tax-free investment growth, and depending on the type, can even provide a tax deduction.

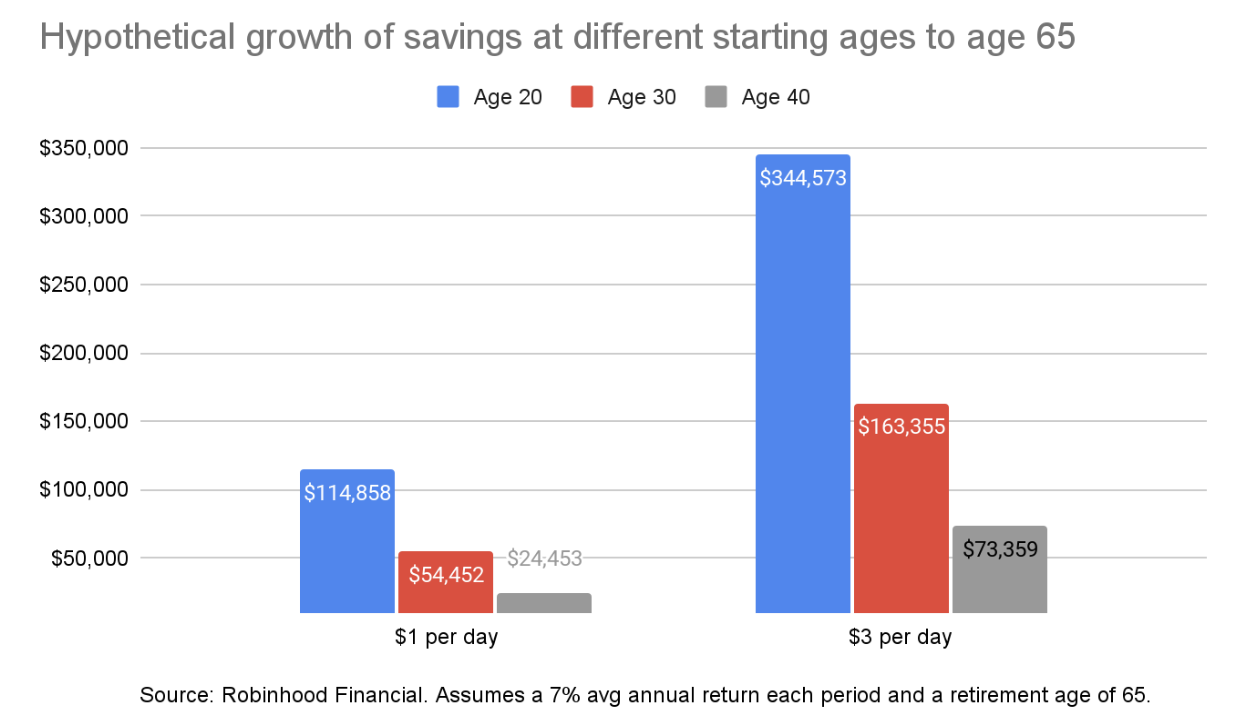

But perhaps a more important aspect is that retirement is so tough to think about when you are starting out on your own and when the cost of living seems to be rising each day. However, saving any amount for retirement on a regular basis is helpful. Even if it amounts to $1 per day. The earlier someone starts saving for retirement, the better position they can be in when the time actually comes to retire. And making sure it gets invested in a diversified way is also important to potentially reaching a more relaxed retirement—so the money can work too.

In our analysis above, we calculated the savings at retirement, from ages 20 to 40, after investing $1 per day and $3 per day, earning a 7% return along the way. This return is less than the long-term returns of the US stock market, which have returned around 10% a year over varying longer periods. While it doesn’t take into account how returns can swing from year to year, it’s a decent proxy for a median outcome over time.

While a combination of starting early and saving as much as one can shows the best result, importantly, this also shows that even starting later, with only $1 per day, can get to something helpful at age 65. The $9,000 saved from age 40 could grow to over $24,000 25 years later—much better than $0 savings.

Similar to making your bed though, caring for retirement savings is important too. What do I mean?

Making sure it's invested is important, but so is knowing the investment fees paid. Mutual funds and exchange-traded funds (ETFs) have expense ratios within them, so know how much that is. For context, the average target date fund, widely offered in 401ks, has an expense ratio of 0.33%, while the average index equity ETF’s expense ratio is 0.16%, according to the Investment Company Institute (ICI).

If you’ve contributed to a 401k plan, know they can have administrative costs associated with them as well. According to ICI, the average participant was in a plan with a total plan cost of 0.55% of assets. But importantly, these can go up if you no longer work at the company.

Which means, if you leave a job where you put money in a 401k, make sure you know your options on what to do after you leave. Check the plan documents to see what fees are involved. There may be an alternative place to put it that costs less (like rolling it over to an IRA or moving it to the 401k at your next job).

Either way, do the work necessary to ensure your 401k isn’t “left behind” after you leave a job. In fact, according to a recent whitepaper from Capitalize, there’s approximately $1.65 trillion of assets in forgotten or left-behind 401(k) accounts—which, they inferred, means close to 30MM people are potentially not optimizing their retirement savings. And we all work too hard for that. So make your bed, or skip it, but don’t skip saving for your future, if you can.