Welcome to 2023 — a new (old) economic phase

Welcome to 2023 — a new (old) economic phase

The turn of the calendar not only brings a new challenge to us all in remembering to write the correct year for at least most of January 🙄 but also gives us a reason to decide not to let the past dictate how we feel about the future.

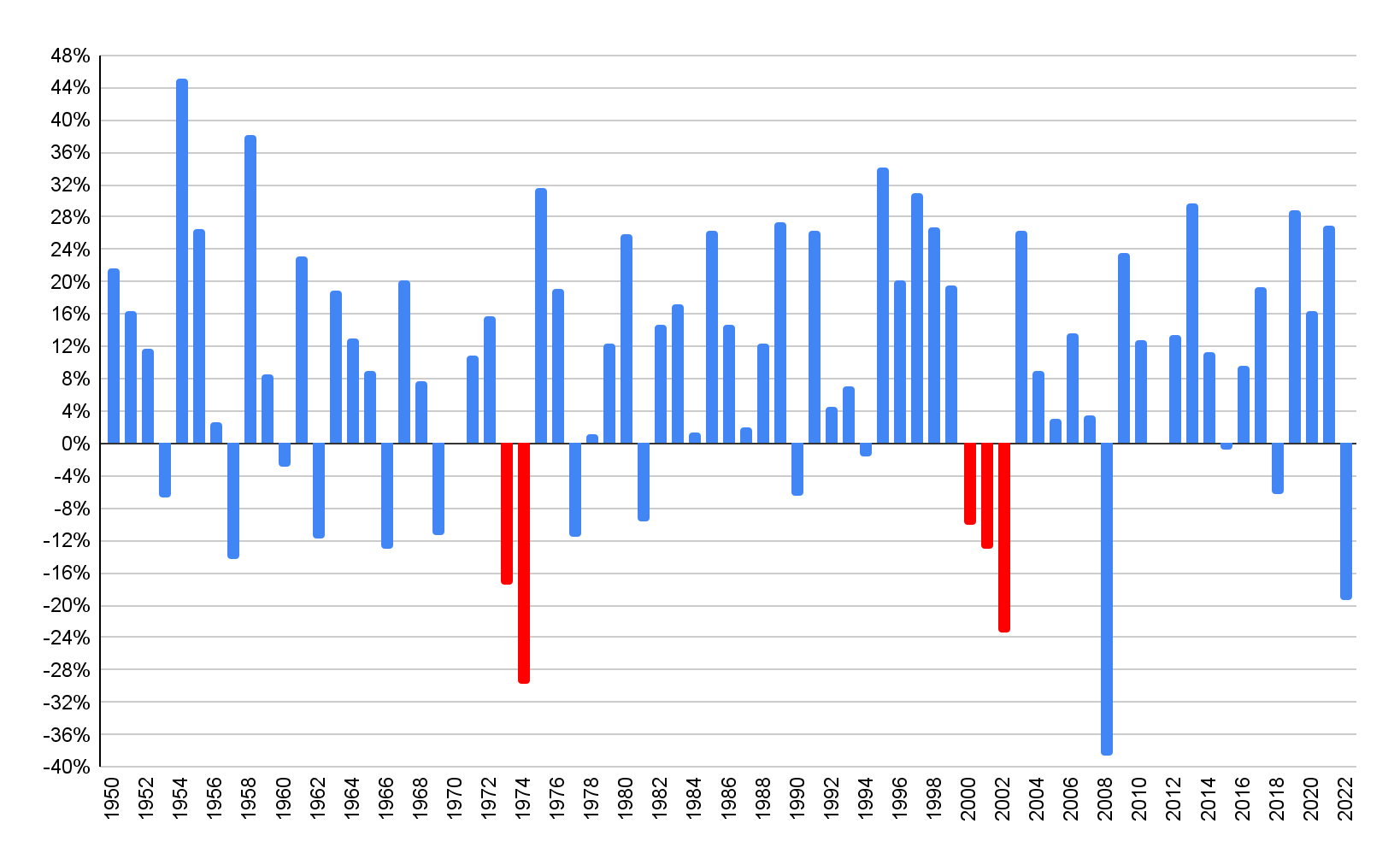

Of course, there’s no shortage of stuff on social media about this time of year — inspirational quotes on seeing a new year in a new way, advice on resolutions, including not to do them, and, of course, data on the markets. This includes how down they were in 2022 (S&P 500 at -19.6%) and how they have very rarely historically gone down again in the following year.

See calendar year chart of S&P 500 price returns going back to 1950 (red denotes more than one year in a row of negative returns):

While all of the quotes, advice, and data are helpful to see, what you personally do about it really carries the most meaning.

Right now, I’m keenly sensitive to my belief that we are economically in a new phase. I’m not saying “it's different this time” — that always feels a little wrong. What I am saying is the catalysts for the last 14 years of the market — quantitative easing (aka QE, aka easy money, aka the “Fed put”*), very low interest rates, high valuations — are no longer an assumption to embed in financial analysis. Comparing current valuations to ones from five years ago, for example, to me, is not worthwhile in most sectors. Just like the way I used to exclude the late 90s tech bubble in looking at historical average valuations, I’ll probably do the same with the 2021 period.

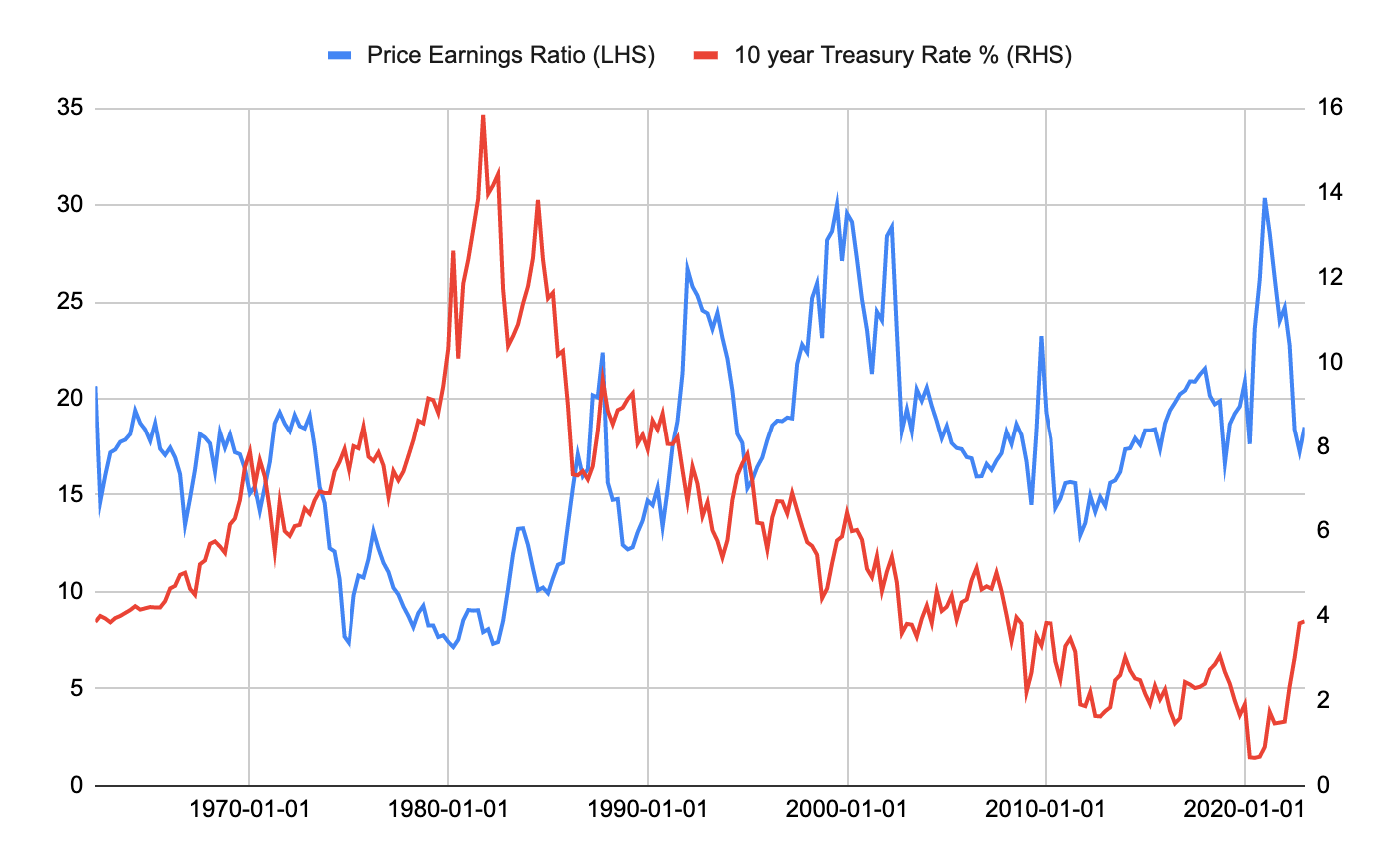

See a chart of stock valuations in blue, as measured by the S&P 500 index, going back to 1962, with the 10-year Treasury rate in red:

You can see that every time rates fell, valuations would typically pop (and vice versa) while overall, they were allowed to be elevated over the last decade plus (even if more volatile).

Going forward, I think we have to dust off some of the old playbooks for valuing companies based on what they are actually doing vs. projecting what they could do with practically free money. In many ways, the playing field among companies appears to be more level than it’s been in a long time. Meaning, I believe it could be rarer to see a company commanding a higher valuation based on potential or just because of the sector they are in (ahem, tech), vs. what their actual earnings and cash flows dictate is fair. And because of this, financial analysis could potentially be more rewarded in this phase of the economy and markets. Simply put, the macro picture will always play a role, but good individual investments may be a little easier to identify now than in the last decade plus.

So for 2023, I personally want to share insights from said playbooks to help you understand markets better. How one does it is not taught in most schools. And even when it is, experience really does matter.

So we are going to spend the next couple of posts sharing some insights on how I and my team approach analyzing a company — or any investment really. It’s not perfect, for sure. Like snowflakes and people, each investment is different and carries its own unique set of risks and potential rewards. However, I believe with an understanding of just a few basic principles, someone can get far enough down their own path to glide (and learn more) on their own.

Before we embark on this next week though, one concept to first understand:

Before you consider investing, it’s important to know what I call your own personal triangle. After paying down high cost debt, a general guideline is to think about your savings/investments in layers.

It’s prudent to first form a foundation of a rainy day fund. This can be an amount set aside in case you need it. I’ve personally found that having it gets me to actually think long term, with my longer term investment funds.

A middle layer of a diversified portfolio for longer term funds

If appropriate (depending on your risk tolerance and time horizon), and #1 & #2 are in place, consider a top layer of more aspirational, riskier investment types

Your mix, the size of each layer, and whether or not that layer is there, is specific to you. One way to consider your own mix is to know your general expenses vs. your income — how much is coming in vs. going out each month or year? After paying down high-cost debt (like credit cards) with the difference, one general rule of thumb is to aim to maintain between three and 12 months of expenses in that rainy day pool — that base layer. Where you land in that range is again up to you and your personal comfort level. If you have that, you can start to think beyond it to the second layer. It doesn’t take much to start building these out — every little bit helps.

Be back to you next week with the first concept: why interest rates matter.

In meantime, we’ve got a busy week of data releases:

Today 10am: ISM Manufacturing, JOLTs Job Openings for November

Today 2pm: FOMC Meeting Minutes

Thursday 1/5: Purchasing Managers Index (a measure of economic activity)

Friday 1/6: Employment report for December, ISM Services, Durable Goods Orders

* The “Fed Put” describes the belief many market practitioners held that the U.S. Federal Reserve (the Fed) will step in with accommodative monetary policy to help cushion the stock markets, if prices fall too far too quickly. This doesn’t seem to be in play today.

Source: Robinhood Financial, Bloomberg