A new language: oil prices

A new language: oil prices

I used to take French classes online because I loved the language. I noticed that my vocabulary expanded with each new part of life explored—types of food or activities like going to a movie. A significant part of me believes finance and investing are the same—a language to be learned as you explore. Understand the language, and it's like you’ve got a rosetta stone for your potential future wealth. The rest is up to you and your actions.

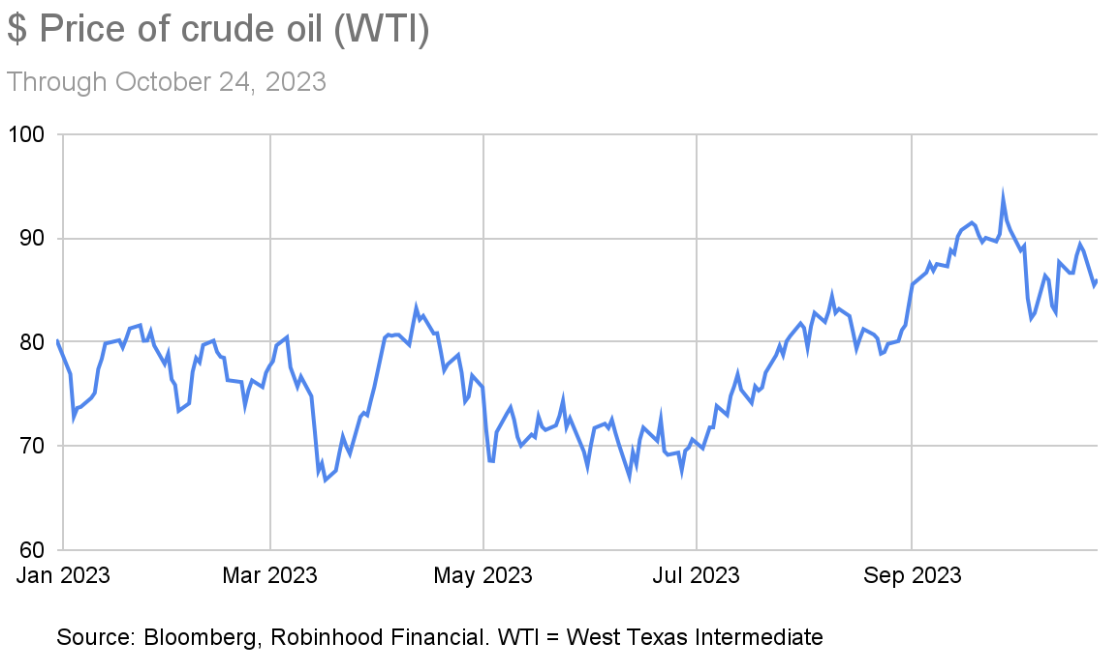

One area I learned about a little later in my career was the commodities markets. In late 2009, a client asked me: with oil prices looking like they might continue to go up, is it investable and if so, how? With this question, came a number of new terms to learn. The question is relevant again today. Here is a chart of oil prices since the start of the year:

Is it investable? The short answer is “yes, but.”

The two main ways you can invest in the price of oil are 1) oil sector companies and 2) through oil futures contracts or ETFs that invest in oil futures. Let’s review them both.

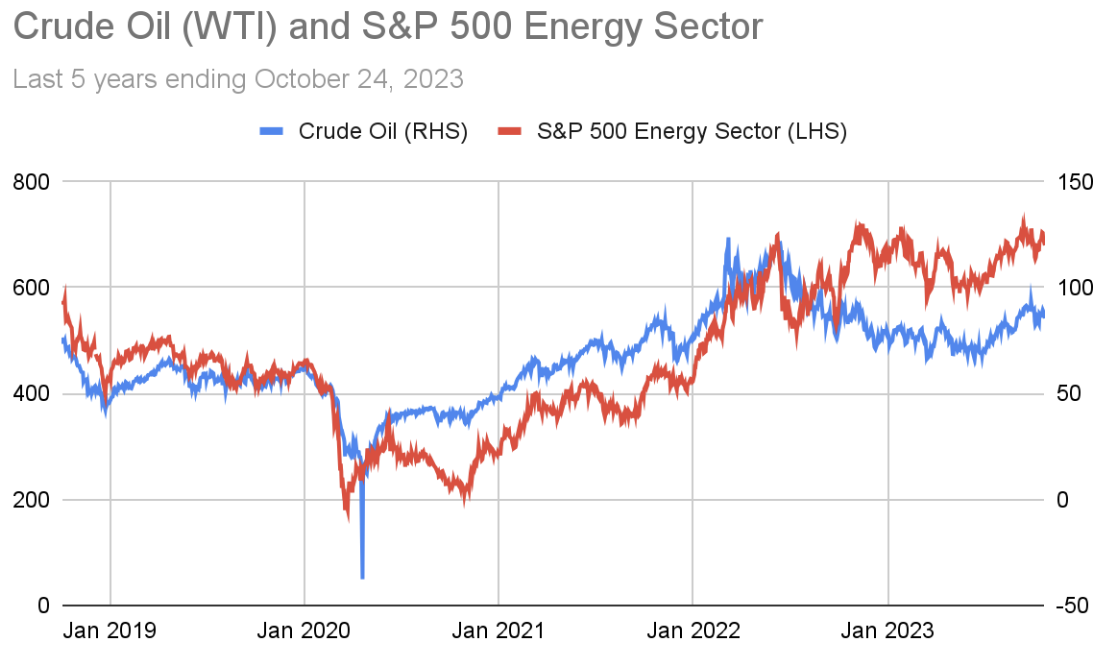

Neither of them are exactly like owning the advertised price of oil. If you invest in energy companies, their prices may indirectly benefit from a rising price of oil, but you also get the company operations with it—and all the decisions made at that company (like who to hire, how to manage the budget, and how to grow). Based on the long-term data below, energy companies have a positive, but not 1-to-1 correlation with oil prices. Of course, stock by stock the differences might be greater or smaller.

If oil prices keep going up, this could eventually be bad for the companies. That’s because at some point oil prices can get high enough to dampen demand, hindering growth for the companies (and economy). But I don't think we are there yet.

With the other way to get exposure, through futures or ETFs that invest in futures, comes an important understanding:

The price of oil is derived from futures contracts (aka futures). Futures are agreements to buy or sell a commodity or security for a set price at an agreed future date. Thus, someone could agree to buy barrels of oil in one month, two months, or even 12 months from now, at an agreed price. The values for all these different points in time are tracked and form what’s called a curve.

The most often quoted price for oil is actually the price of the front month contract—so right now that would be the contract that expires in December.

Given these two points above, if you wanted to stay invested in oil prices for several months, you would have to, in effect, keep buying the next month, each month.

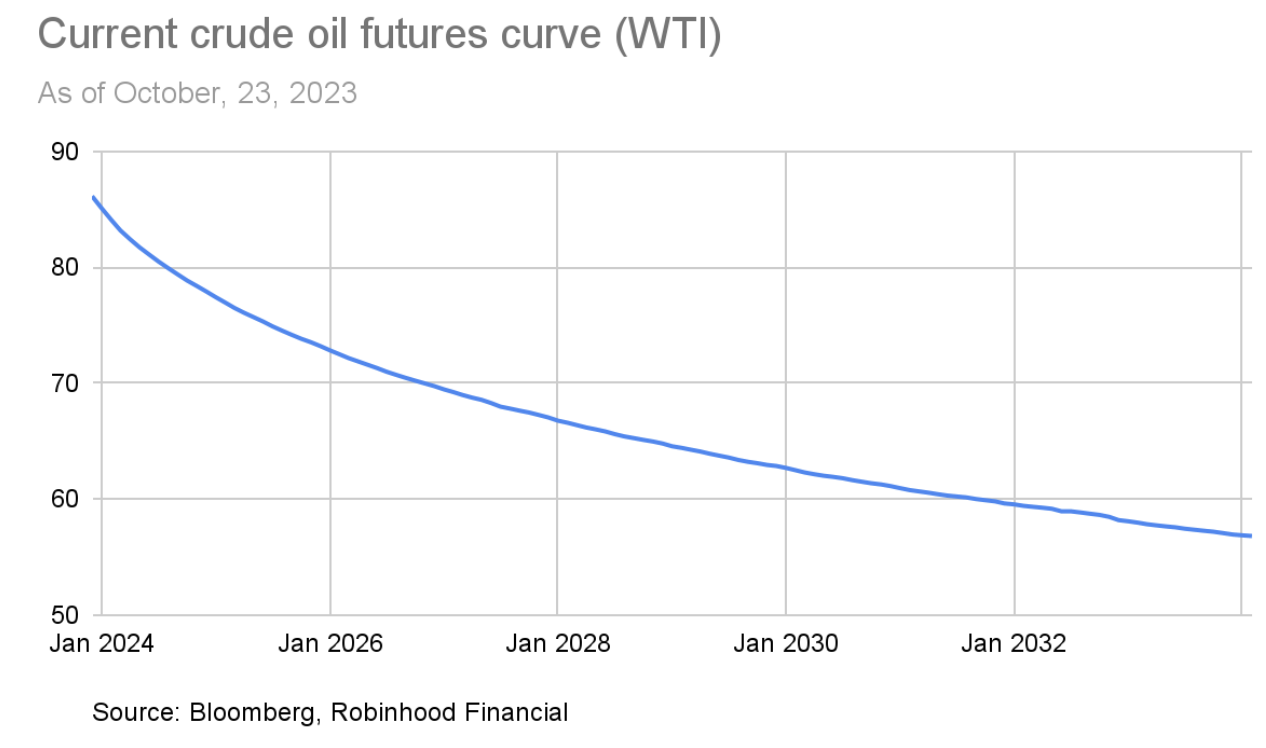

So this is where the curve comes in. If, for example, each contract costs more than the previous month, that means you need to believe oil prices will rise faster than the curve—and vice versa. Here’s an illustration of the current oil curve:

So what this current curve is generally saying is there may be a benefit to owning the physical material now—known as the “convenience yield.” When inventory levels are high, the convenience yield is low but when supplies are low, the yield is high. If you believe prices will rise further in the future, you could stay invested in the price of oil from month to month and have a positive “roll yield,” which comes from each future month’s oil price being lower than the previous month. By the way, this shape is called “backwardation” and I only remember it because it falls, as if you fell backward off the side of a boat.

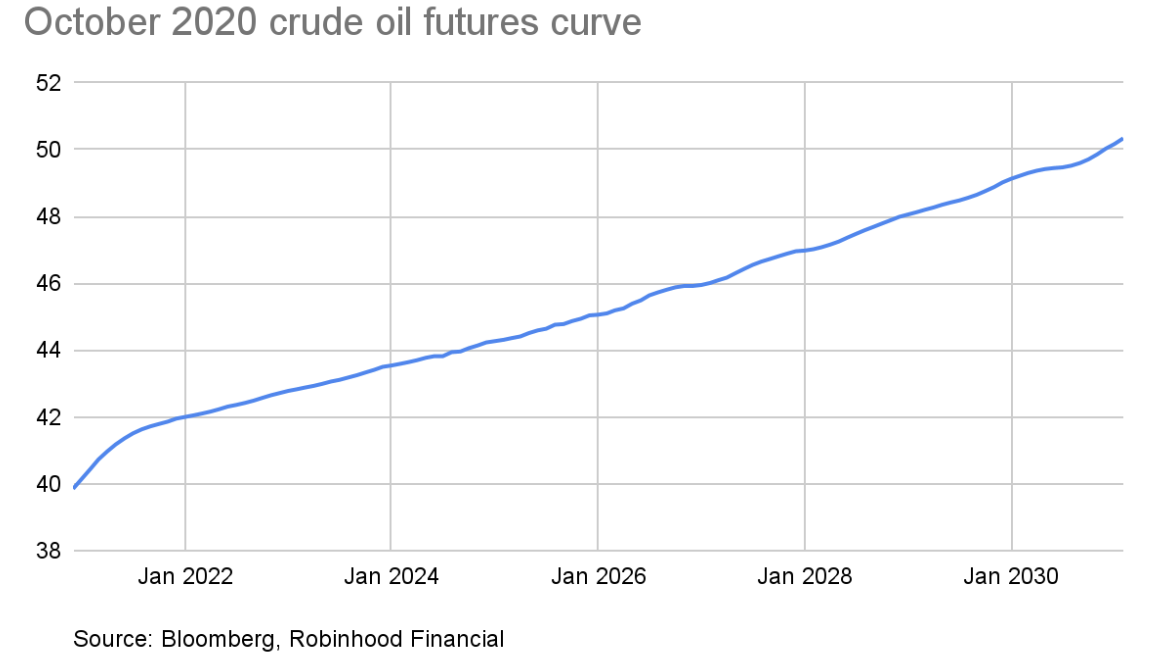

However, note that this curve, and the shape you see today, can change at any time, particularly from a shock in supply or demand—like from weather or geopolitical tensions. For example three years ago, in October 2020, the curve was shaped the other way, with higher prices in the future and low demand from a recession (thus inventory levels increased):

This shape is called “contango,” which always makes me think of the Argentinian dance of a similar name (the tango). Which reminds me of a tango dancer's arms pointing up and out. It's the only way I remember it.

As for oil prices, I believe they will remain elevated, despite any impact from a slowing economy. Tensions in the Middle East will keep supplies as a point of contention. In addition, the winter season is coming in the Northern Hemisphere and the need for the US government to restock their reserve supplies remains.

For my client back in 2009, we eventually decided the answer for him was yes. But I made sure he knew that buying an oil ETF or energy ETF may not provide what was intended. And always knowing what you want to own is important. We also both got to expand our vocabulary in the process.