A short history of bank failures

A short history of bank failures

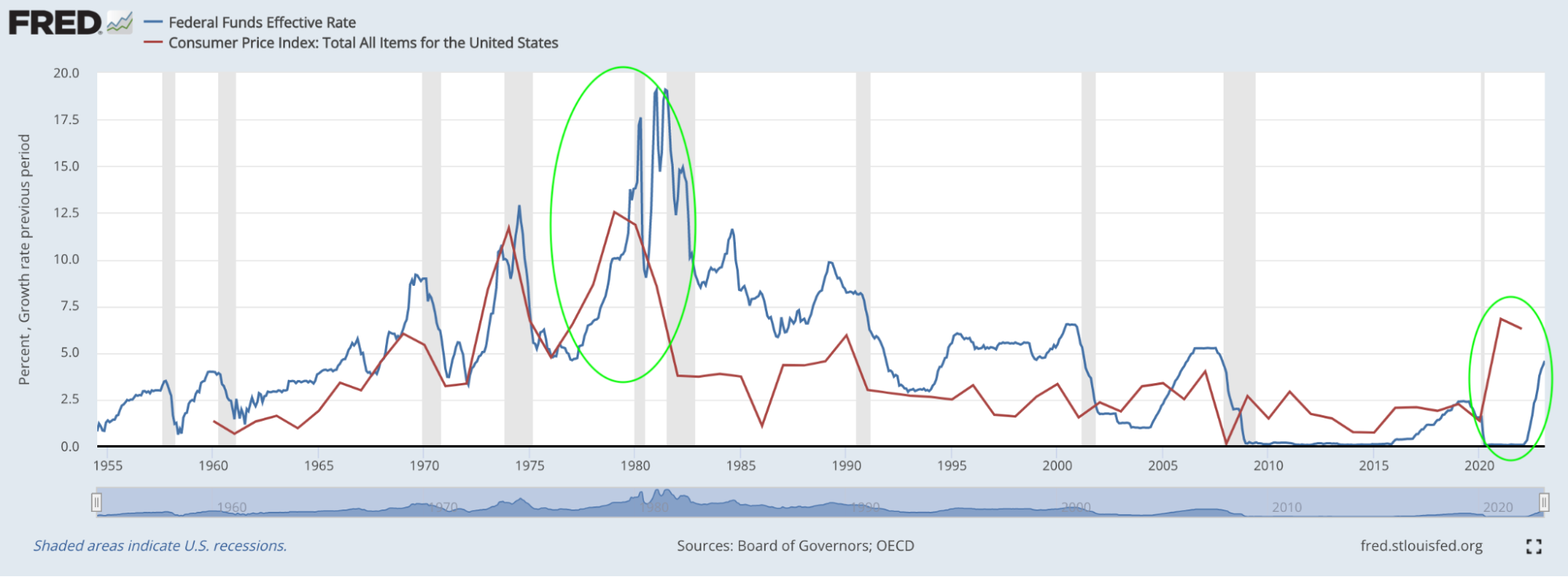

Inflation rates and interest rates both climbed quickly, and this created two problems. One: interest rates that banks could pay on deposits were lower than what could be garnered elsewhere, so cash started leaving these banks, and two: assets (loans, mortgages, and investments) all lost value due to the rising rates.

If you’ve been keeping up with the news in the banking sector, this sounds like what happened this past week, right? But what I am actually describing is the start of the Savings and Loan Crisis of the 1980s (see the spikes of the Fed Funds interest rate and inflation in both the 1980s as well as more recently in the chart below).

That’s right. On a smaller scale, we witnessed history repeat itself this past week as three banks failed due to inflation and rising interest, a mismanagement of risk in assets… and a concentrated customer base. Let’s hope this story ends a bit better.

That’s because when this happened in the 1980s, Congress responded by passing the Depository Institutions Deregulation and Monetary Control Act of 1980. But regulators enforcing it lacked sufficient resources to deal with the losses taking place (it was estimated to be a $25B problem with only a $6B industry insurance fund at the time). So they pivoted, deregulating these smaller banks, which were originally designed to support mortgages and homeownership, with the intention of letting them grow out of their problems on their own.

To me, that’s like letting your kids eat unlimited candy in the hopes they will do the right thing and restrain themselves. So it didn’t work. Many of the S&Ls became known as “zombies,” taking on even riskier loans than before and promising higher and higher deposit interest rates to attract cash deposits (which meant they limited their own profits from the riskier loans), worsening the problems.

Eventually, a true bailout was required, and significant reform legislation came in 1989. With reform, these small banks were placed under the FDIC (the insurance fund for all banks today), and the Resolution Trust Corporation (RTC) was established to resolve the remaining troubled S&Ls. The RTC eventually closed 747 S&Ls with assets of over $400B, and an estimated cost (mostly to taxpayers) of over $100B, taking about 16 years to complete.

Reflecting back on what happened in that period, more swift and decisive action may have been the better move. This is certainly the lesson regulators heed now when financial system stresses show up, which is why we saw deposits guaranteed at the failed banks and funds put in place for future troubles pretty quickly.

But it is disconcerting that for all the regulations that have come, particularly since 2008, the imbalance of these failed banks’ balance sheets still fell under the radar.

It’s not clear if there is more to come. But what seems more clear, especially given the lower producer price index (PPI: a measure of inflation) numbers today, is the Fed is likely done raising rates for now after their meeting next week (March 22). I am, like many, 50/50 on whether they increase rates by nothing or 0.25%. But I believe we will see the “Powse” I’ve mentioned before, thereafter. This doesn’t mean they will start to take rates down. Inflation is still a thing, and they can’t let that go just yet.

Sources: Board of Governors of the Federal Reserve System, OECD, "Main Economic Indicators - complete database", Main Economic Indicators (database),http://dx.doi.org/10.1787/data-00052-en (Accessed on date) Copyright, 2016, OECD. Reprinted with permission. Federal Reserve History, Federal Deposit Insurance Corporation.