The lists — to dos before the year ends

The lists — to dos before the year ends

All of sudden, I already feel behind on holidays (gifts, cards, NYE plans), plus all the year-end financial things I should think about. But then I remember that’s the inner critic/perfectionist in me. I’ve named her Barbara and recently told her to chill, and maybe find some CBD gummies. The world won’t end if cards don’t go out and there is no NYE plan this year. Time to prioritize.

So I made some lists. Here goes:

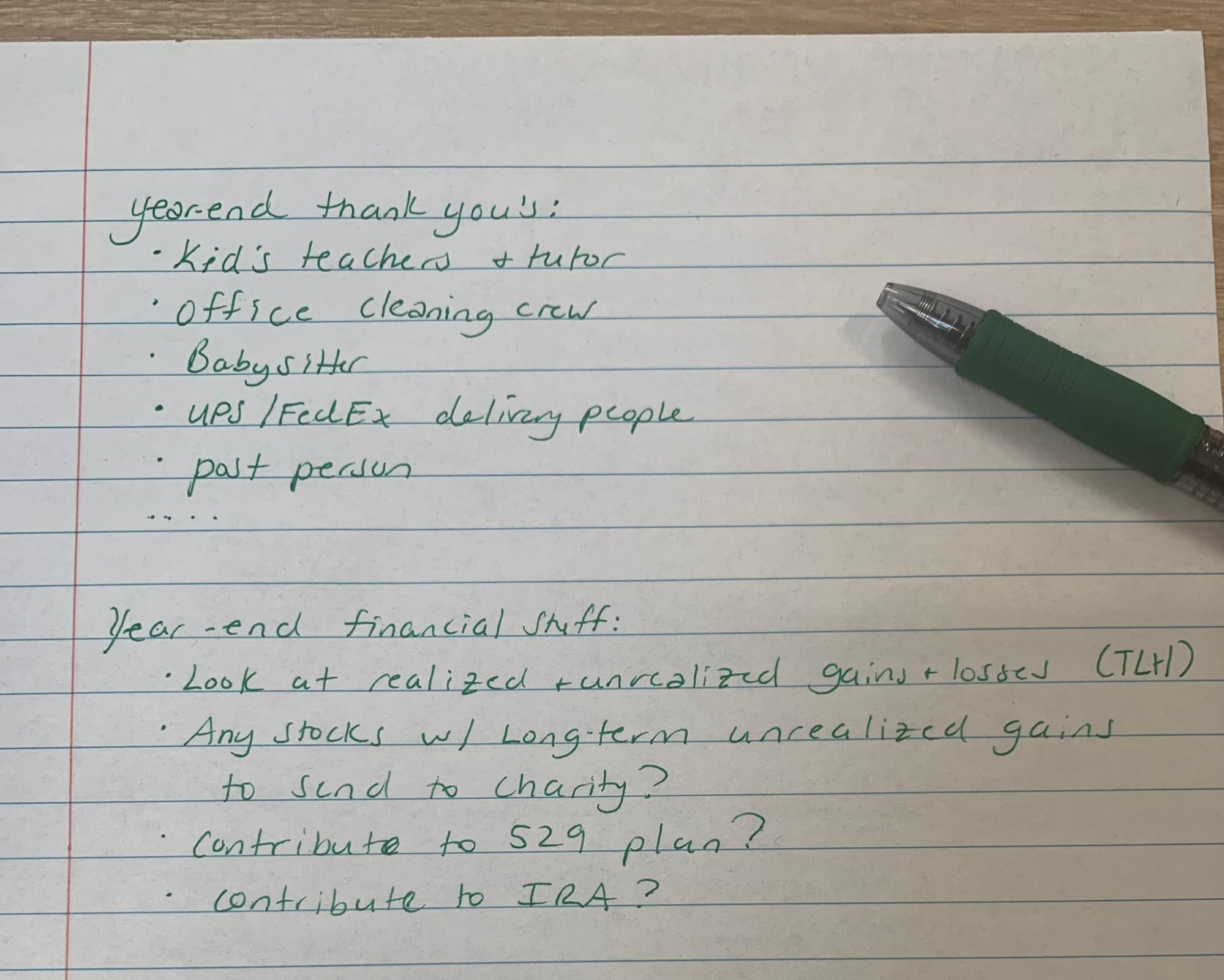

The financial stuff is too easy to put off. But doing them helps form good habits and can be really important in the long run. Let’s go a bit deeper in these — and always consult a tax advisor for questions on your specific situation.

Gains and losses: Whenever you invest, you are going to have things in your account that go up and down. While it might be more the latter this year, even in a year where markets are strong, you may still have a stock or two that you’ve lost money in. So while reviewing your investment accounts with an investment lens is always good practice, adding in a particular lens over the gains and losses in accounts subject to taxes (so not IRAs or 401(k)s) is also good practice at this time of year. This — often referred to as tax-loss harvesting — is a strategy that can help make sure you won’t be paying more taxes than you need to. That’s because:

You may be able to offset any gains you realized (meaning you sold an investment with a gain during the year) against losses you realized (aka selling an investment at a loss), limiting potential taxes.

Depending on your income situation, if you don’t have any realized gains this year, or you have more losses you want to realize than gains, you can use your losses to deduct up to $3K from your stated income.

Finally, if you have more than $3K worth of losses, you can carry losses you take this year into the future such that they can help offset future gains.

You can always buy anything you sold back after 31 days and still keep the realized loss — but note if you repurchase the same or substantially similar investment within 30 days, this would be considered a wash sale, and you can’t deduct those losses.

Charitable giving: If you like to give to charity, especially at this time of year, a very efficient way to give is to transfer whole shares of something you invested in that has a long-term gain (owned for more than 12 months). If you do that, you may be able to claim a charitable deduction worth the value of the shares, but you also never have to sell the shares and realize the gain, creating a potential tax benefit. You can then immediately replace the shares in your portfolio, should you want to, with the cash you would have given to the charity.

529 plan giving: While this really depends on the state you live in (e.g., NY does this but NJ does not), it may be worth looking into whether you get a tax deduction for giving to a 529 plan. 529 plans are designed to save for college and beyond and, like an IRA, grow tax-free while you are contributing to it, for your children, a niece or nephew, or anyone in your family that could benefit from college savings. You can always change the beneficiary as well, as long as it’s the same generation or later.

Contribute to an IRA: Individual Retirement Accounts (IRAs) were created for people to be able to save more for the long term. Realized investment gains in IRAs are not taxed before withdrawal, and if it’s a Roth IRA, withdrawals may never be taxed. Depending on your income, you may be able to contribute to a Roth IRA, a traditional IRA, or both. You might even get a tax deduction for contributing to a traditional IRA. While you don’t get a tax deduction for contributing to a Roth, your withdrawals in retirement can be tax-free. And even if you make more than the allowable amount to contribute to a Roth IRA or to get a deduction for a regular IRA, contributing to an IRA every year up to the max helps increase your long-term savings and the potential future value of it. This year, you can give up to $6K (with an extra $1K if you’re over 50), while next year you can give $6.5K. And even if you forget before the year ends, as long as you haven’t filed your taxes yet, you can contribute to your IRA for the previous calendar year up to Tax Day (on or around April 15). Just make sure you tell your financial institution what tax year it’s for — lots of clients of mine used to give for both years at the same time to get it over with.

And this last one is more important than ever. I’ve been thinking a lot about the data around long-term savings (it’s falling), how the way we are working and living is changing (more people are taking part-time or contract work) and the spending decisions the government made over the last several decades (our deficit is the highest in modern history). Essentially, the safety net our grandparents had — pensions and Social Security — has faded. Pensions are barely offered these days, replaced by 401(k) plans that moved the onus to the employee to save. Social Security, unless it gets more funding, it’s expected to not be able to deliver the same benefits as soon as 2034.

So if this last decade or so has taught us anything, it’s to empower and take care of ourselves. This includes saving enough — even if it’s a very small amount each month or year. It can add up over time.

And there’s nothing more satisfying than crossing something off a to-do list (per Barbara). So here’s to a fun (and accomplished) holiday season.

See here for more info on tax loss harvesting, IRAs, and the IRS website on IRAs and charitable giving.