Rain or shine, it’s time for earnings season

Rain or shine, it’s time for earnings season

The drive home from the holiday weekend brought the kind of rain where you can’t see anything on the road. The kind where your wipers are at their fastest speed, and the water on the edges of the highway flies up dramatically as you drive, flashing warning signs in your brain. When it happens, you can either pull over and wait for it to pass, or keep going (slowly), stay aware and breathe.

Investing and watching your portfolio can be the same way. Sometimes it’s storming, sometimes it’s calm, and sometimes it's so hot it gets your mind wondering when it will all stop (and if you should sell). Generally speaking, if you are in the right plan and investment allocations, then the right course of action is always to breathe and keep going. But no matter the season and weather of the market, earnings season is often a time to cause big moves in stocks—at the individual level as well as the sector and theme level. And earnings season is set to kick off in two days, on Friday the 14th.

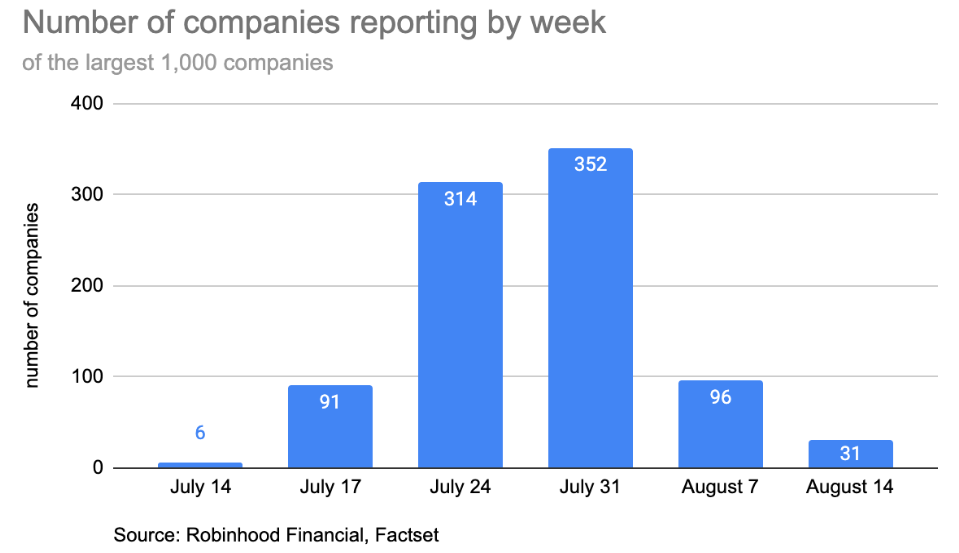

Starting on Friday, the following month will bring the earnings reports of over 85% of the largest 1,000 companies. The biggest reporting weeks are those starting July 24 and July 31, when ⅔ (about 67%) will provide a quarterly update on their businesses.

The thing about earnings, like the weather, is it’s all about expectations. If you build up your own expectations of enjoyment of an outdoor activity and it rains, it's pretty disappointing. Earnings expectations get built up and down all the time. And it can lead to nice (and not so nice) surprises—with respective market reactions.

Looking back in history, expectations of what earnings will be reported usually fall before the reporting season starts. Yet, according to Factset’s Earnings Insights, this upcoming quarter is showing one of the smallest negative revisions in quite some time. The aggregate Q2 estimate for earnings of S&P 500 companies fell by -2.9% over the past few months. Compare that to last quarter’s revisions, where expectations dropped by -6% heading into the quarter, and actual earnings reported were generally a pleasant surprise, helping to drive the markets higher. This -2.9% also compares to the 10-year and 20-year average quarterly estimate declines of -3.4% and -3.8%.

What this all means is that it could be easier to disappoint investors during this next earnings season, on average. But despite this data, I personally believe, through effective cost management and better than expected growth, companies have a decent chance of reporting good earnings this Q2 2023 season.

As I look at the weather forecast for the market though, I note two things:

September is a historically poor month for markets. This doesn’t mean this year’s September will be bad but, since June was very strong, if July and August are close to small returns, then the year is close to a typical trajectory.

Inflation has been cooling. With it, I am concerned that, as time goes on into later quarters, earnings seasons could get tougher. It’s possible revenues could cool with the lower inflation—as companies won’t be able to raise prices as much—hurting profits.

Both are things to expect as possibilities—so you can be a prepared investor—whether that means changes in your portfolio or simply staying aware and focusing on your breath.