Rage ceilings, regret ceilings, and debt ceilings

Rage ceilings, regret ceilings, and debt ceilings

Maybe it's a big birthday celebration or even a wedding. But at some point, you might have held a party that not only helped you meet your peak partying potential, but also may have led to a bit of regret… and even some debt. It is understandable—as a party is planned, it gets easier to spend more than expected as the day approaches. And by the time the day of the party arrives, you figure you might as well fully enjoy it, given all the money that was spent (and related debt that may have accumulated).

Another place that money has been spent accumulating debt (and might also carry some regret) is in the US government. Debt ceiling headlines have recently been growing with talk of it being reached—and that this could mean bad things unless Congress acts to raise it. While it doesn’t sound good, many of us probably wonder the same things: What exactly is the debt ceiling? Why has it been reached? What could happen if nothing is done about it, and should any of it matter to investors?

To understand it all better, like many things, looking at history can provide helpful context for where we are today and where things could go in the future.

For background, the Constitution grants Congress the power to borrow money, based on the taxing authority of the United States, allowing it to determine fiscal policies. Over time, Congress granted Treasury Secretaries (today that’s Janet Yellen) more leeway in debt management. Eventually, in 1939, the U.S. Treasury was granted authority to fully manage the structure of federal debt, while also imposing an aggregate limit (aka a ceiling) on the amount. This debt limit applies to almost all federal debt; both held by the public (like in the form of treasuries) and held by the government’s own accounts (like Social Security and Medicare).

In general, since the debt ceiling became a thing, it’s been increased many times. Debt owed by the US government would grow to the established ceiling, and cutting debt would mean tough decisions on what would be funded and what wouldn’t. So instead, the ceiling would eventually be raised each time. The biggest increases have happened after a recession started—since government debt tends to increase in order to help the economy recover.

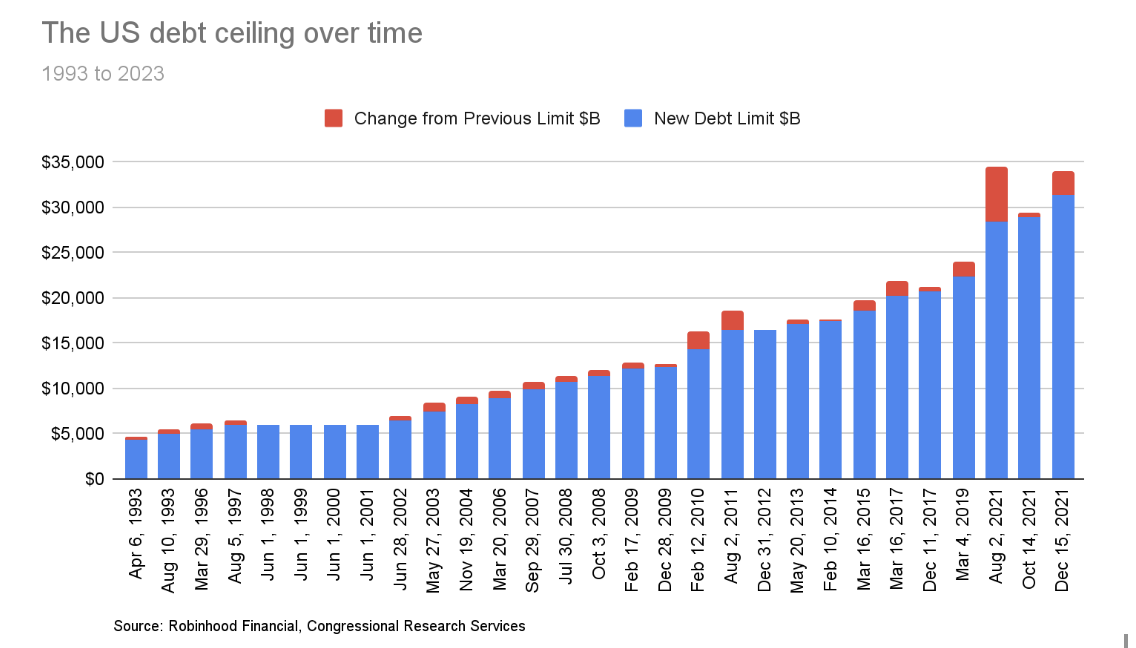

We looked at the debt ceiling going back over the last 30 years, to 1993. During this time, there was only one stretch, from 1997 to 2002, when debt limit increases became unnecessary due to federal surpluses. Since then, however, the federal government has run persistent and growing deficits. See the chart below, which shows an over 600% increase in the debt ceiling, from $4.4 trillion in 1993 to $31.4 trillion today.

On the surface, the reasons for expansions include tax cuts enacted in 2001 and 2003 along with higher spending, the aftermath of the 2007–2009 financial crisis and Great Recession, tax cuts from 2017, and, of course, the COVID-19 pandemic. All helped push deficits to higher levels, which required a series of increases in the debt limit. After recessionary periods, the increases were around 25–35%. Below the surface, the growth of Social Security and Medicare benefits, particularly as the Baby Boom generation has moved into retirement, has increased deficits by more than other factors.

One more historical point of note was in 2011. Back then, similar to now, Congress was split by parties and a debate ensued between raising the debt ceiling vs. spending cuts, while the clock ran down to the wire. Eventually, within 72 hours of a debt breach, the Budget Control Act was passed, increasing the debt ceiling in three steps, in exchange for planned spending cuts over 10 years. This new legislation added one more option for the future—the debt ceiling could be temporarily suspended to help avoid future near or actual misses.

The fallout from this close call contributed to the US credit rating getting downgraded by Standard & Poor’s for the first time ever (indicating to potential investors that US debt wasn’t as safe as it once was and diminishing trust in the country’s economy). Markets plummeted (the S&P fell -17% in the two weeks around this event–see chart below), interest rates increased, and the country’s borrowing costs increased. In the details, what types of stocks fared better during this period were those deemed “low volatility”. That, in essence, means ones that did not necessarily need a strong economy to fare well. This might be consumer staples (products that meet everyday needs) and areas of healthcare, as examples. This was also the start of a tech rally.

Of course, if a breach had occurred, or does in the future, the damage would be far worse on the market and longer lasting—the US would have to prioritize paying its external debt while issuing IOUs to internal debt holders. Jobs would likely be lost and budget cuts would have to be far deeper.

This, in essence, is why it’s important for investors to watch this space. If nothing else, it causes stress and volatility on the stock market, given how essential the Treasury market is to all others. This is a place investing and politics meet.

As of January 2023, the current debt ceiling was reached. Since then the U.S. Treasury has been using “extraordinary measures” to cover bills, extending the deadline for a decision to increase the debt ceiling or temporarily “suspend” it. Current estimates of the final deadline range from early June to mid-August and are dependent on varying tax revenues as well as spending needs. Yellen is expected to issue a letter with an updated deadline this week or next (her last letter said June) and the House is expected to vote on a bill that could increase it in exchange for spending cuts.

Based on all of this, and also important for investors to understand, there are lessons learned from 2011. Many of the hard-fought planned spending cuts never materialized—particularly the ones slated further out in time—because subsequent legislation neutralized it. In addition, it became clear to many that the two issues of debt ceiling and spending should be separated to have more clear discussions.

We’re watching t-bill rates as one measure of market anxiety around this issue — the higher they go, the more concerned the market may be. Given Congress is even more split than in 2011, we believe the most likely near-term outcome is a suspension of the debt ceiling to a certain date—kicking the can down the road—perhaps even into the presidential election season.

So whether US policymakers regret the debt or not, it’s something they’ll have to face eventually. It would be nice for investors if they made it a party and came together on real longer term change, but a decision nonetheless would be a start.

Source: US Department of the Treasury, Congressional Research Service