I’m cleaning out my closet: tax loss harvesting

I’m cleaning out my closet: tax loss harvesting

Like spring cleaning and clearing out a closet you haven’t gone through in a while, towards the end of every year is a good time to take a look at your portfolio, with your income in mind, and a tax lens in hand.

Despite the S&P 500 being up nearly 19% this year through Friday, November 23, there are a lot more stocks, by number vs. proportional weight, that did worse. Looking at the largest 1,000 US stocks, 70% of them had returns below the S&P and 44% actually fell in price so far this year. Only 30% did as good or better than the S&P.

This all means, it’s a good time to assess what gains or losses you have in your portfolio and any actions you might want to take.

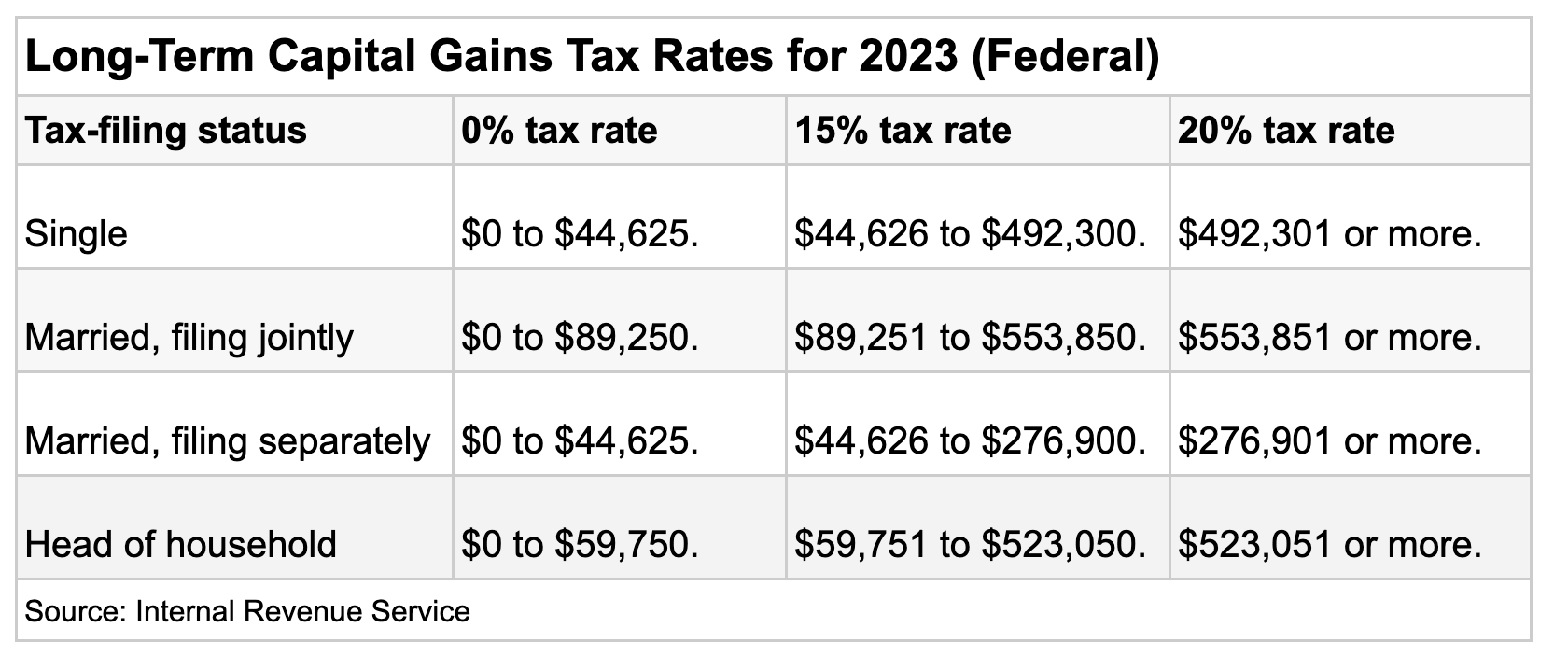

Capital gains (and losses) are a result of an asset being at a price higher (or lower) than you paid for it. Realized capital gains—or selling an asset for a profit—are usually subject to taxes based on your income level and vary by the length of time you held an asset. So it’s good to know where you fall on this. If you hold an asset for at least 12 months and one day, any gain will generally be taxed at the long-term rate (between 0%-20%). See below for the 2023 Federal long-term gains tax rates.

Anything held 12 months or less is considered a short-term gain, and the tax rate is then based on your ordinary income tax rate (which is usually higher, between 10% and 37%).

Before I go on, it’s important to note the above does not apply to investments held in retirement accounts. Taxes on gains do not apply to sales within an Individual Retirement Account (IRA), 401k or other retirement program. This means investments that happen inside the account are generally not subject to tax—and only usually come when you withdraw an amount in the future, depending on the type of account you have.

Lots of people talk about tax loss harvesting. While it has nothing to do with farming, to do it requires you to look over your taxable portfolio for both gains and losses, realized and not realized. If you are subject to long-term capital gains tax, loss harvesting is a good thing to understand. This is because gains that would be taxable can generally be offset by losses taken—aka, harvesting losses. If your gains are offset, you may be able to mitigate your tax bill. The three main things to gather are:

What you sold during the calendar year, if anything

Whether it was at a profit or loss

How long you held it (more than 12 months vs. 12 months or less)

Once you know all that, you can subtract the realized losses from realized gains to see where you are. If you end up in a positive gain, you might decide that is fine and potentially pay taxes on it. Otherwise, you can choose to sell any positions that are currently at a loss to offset those gains.

A couple of things to know about tax loss harvesting:

If you decide to tax loss harvest, know the “wash sale rule.” This rule prevents you from taking a tax loss if you buy a security considered “substantially identical” within 30 days either before or after the loss trade date, in any account. So you can’t sell for a loss, buy it back the next day and expect to mitigate a tax bill. You must wait 30 days after selling for a loss to buy it back, and you must also have not bought that same security 30 days before. Note, I said “in any account”—because trades made in a retirement account would count toward the rule in this case.

Generally, the IRS allows up to $3,000 of a capital loss against your income. So if you generate losses that, after accounting for any gains, add up to a $3K net loss, this could help your overall tax bill. Any losses above this amount, can be carried forward against income in future years.

Since short-term gains can be more “costly” through higher tax rates, be sure to consider that as you’re investing. If you are a short time away (like a few days), from holding a profitable investment you want to sell for more than 12 months, then consider whether holding it a few more days to go long term is better for you vs. selling it that day.

There are, of course, other ways to be tax efficient. Contributing to and investing within an IRA, depending on your income, can provide a tax benefit. And if you are charitably inclined, giving to the charity in the form of shares that have a gain and were held for more than 12 months, can be a tax efficient way to do that vs. donating cash. In this way, you never realize a gain and you can potentially get a deduction for the charitable donation in the amount of the value of the shares donated. You can then use cash to buy the same investment back (without worrying about a wash sale rule), should you choose to.

While this part of portfolio management can feel complex, once you practice it a couple times, it will start to feel natural—good, even. Just like it can feel after cleaning out a closet.

For more information and descriptions of tax loss harvesting, see our Learn article here.