The US dollar — scary or fun?

The US dollar — scary or fun?

Nothing is better than Halloween. You get to play someone else for a while and explore who they are. And IMO, deciding on the details of a costume is just as fun.

The decision for me always starts with fun or scary? So many options.

But to be honest, that’s how I feel about life and the markets. Everyday life has generally come back after COVID. It's much more fun to go out these days and the gratitude for that has not yet been forgotten. But war, inflation, supply chains, and the impact of the opposite of stimulus have all led to feelings of trepidation.

For central banks outside of the US and global companies based in the US alike, the strength of the US dollar has become another source of unease.

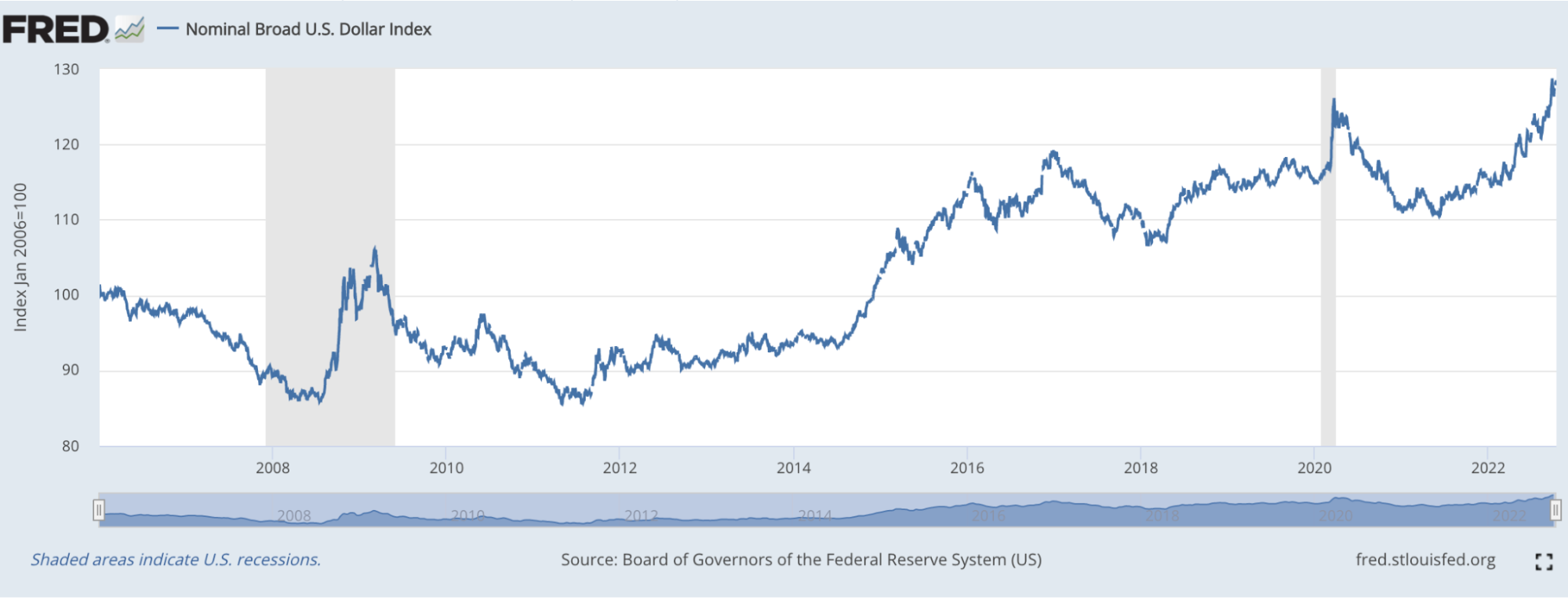

For context, here is a chart of the US Dollar Index, which shows the value of the dollar going back to 2006, relative to a group of currencies the US trades with the most. You can see the current levels are at a peak for the time period (up over 11% this year).

While there are a lot of things that can move a currency, two main ones are:

Interest rate differentials: This is the difference between central bank policy interest rates, where the country with higher rates will often have a more valuable currency than the one with lower rates, all else being equal. →The Fed is currently raising short-term rates, and has done so more than most other central banks, while inflation has raised long-term rates. This has lifted the value of the USD.

Capital flows: This is when investments in a country look so attractive that money (aka capital) starts flowing their way or vice versa. →With the current market and economic conditions suspected of slowing economic growth globally, more money has been flowing to the dollar as a “safe haven” relative to other types of investments. This is not to say it's going to the US stock market, but more likely sitting in cash or cash-like investments denominated in US dollars.

Why is a strong dollar tough for some companies?

For US companies with global businesses, the rising dollar means sales in other countries become worth less when translated back into dollars. This naturally has a negative impact on those companies' earnings. It can also make the goods/services of these companies cost more in other countries, negatively affecting demand. While research analysts try to estimate earnings that are smoothed from currency movements, it’s still due to create volatility in stock prices.

According to Factset, 40% of the S&P 500 aggregate revenues come from international sources vs. domestic. Tech and materials sectors are the most exposed vs. utilities and real estate, which have virtually no exposure. This makes intuitive sense based on the kind of businesses they are.

And so far, the strong dollar has made a difference in returns this year. US companies in the S&P 500 Index with no foreign revenue are down less relative to companies with some or a lot.

Year to date through October 14, 2022:

Return of companies with foreign revenue >=50%: -28.9%

Return of companies with foreign revenue <50%: -18.8%

Return of companies with foreign revenue = 0%: -16.0%

Source: Factset

And according to a report from Goldman Sachs, an analysis going back to 2003 showed a stronger dollar is correlated with fewer revenue beats. Something worth watching as we get deeper into earnings season over the next couple weeks (77% of the S&P will have reported their Q3 before we get to Halloween).

Why is a strong dollar not welcome by central banks around the world?

Well, related to what I stated above, it makes any US good or service in their country cost more in their local terms — meaning that it compounds the inflationary pressures everyone is feeling now. This is why you have seen some countries like Japan, who is not raising interest rates, attempt to “defend” their currencies by buying more of it — they are trying to limit the inflationary impact.

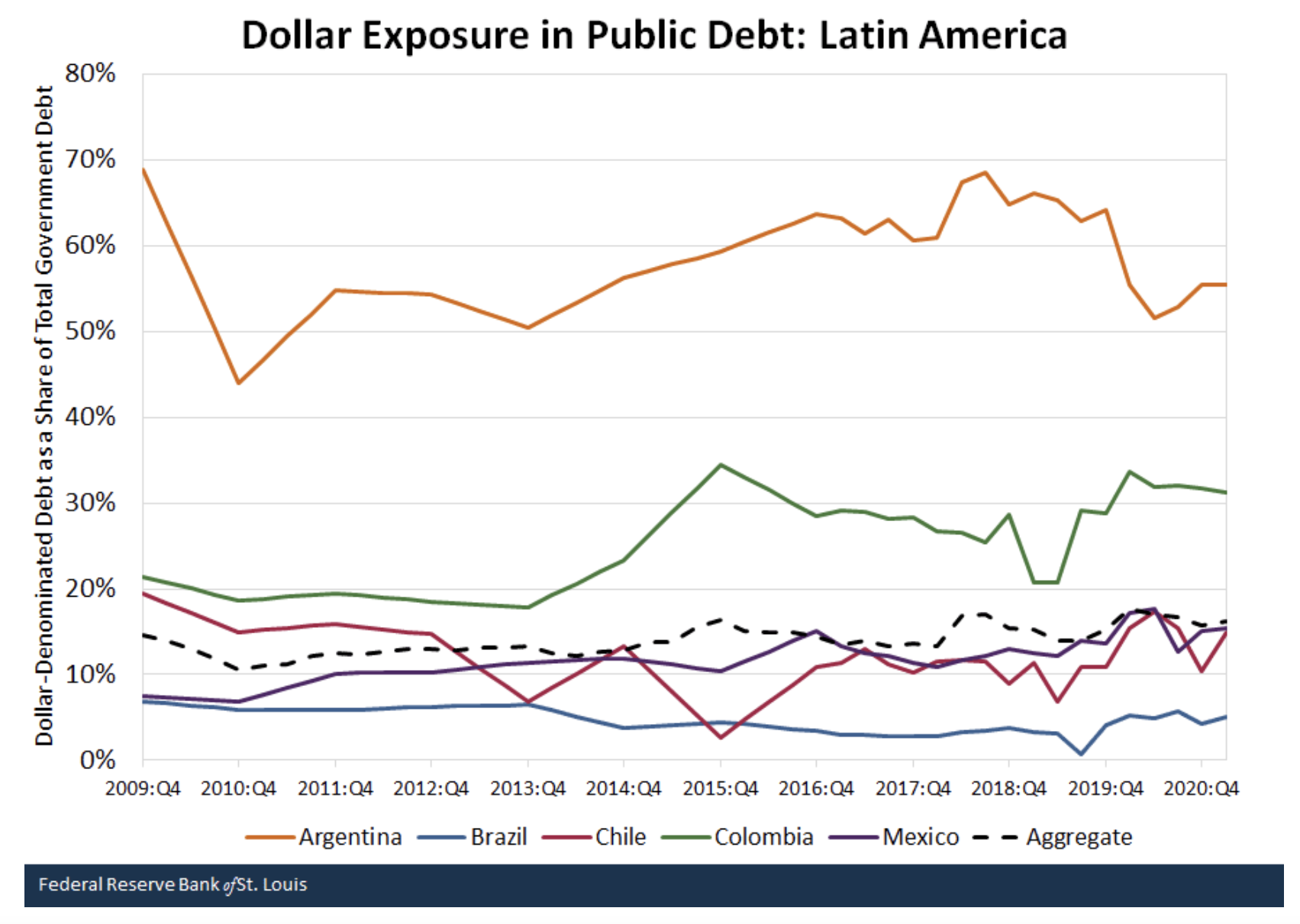

Furthermore, there are some countries who issue debt in USD rather than their own currency. They do this to broaden the universe of potential buyers of their debt. However, as you can imagine now, when the USD rises in value, this makes their debt more expensive for them, as their interest payments end up costing more with the rise.

This is something we are watching closely, especially for emerging countries. In particular, according to the Federal Reserve Bank of St. Louis, Latin American economies are most impacted by this, where at the aggregate level, issued dollar-denominated debt makes up around 17% of total government debt in select countries. See chart below with percentage of US dollar denominated debt by selected countries in Latin America.

Now on the other side, the opposite is true for the US central bank — the Fed — and companies who do business in the US. A strong USD should make items we import into the US less expensive in USD terms, helping the Fed’s focus of lowering inflation. And for companies that sell into the US from abroad, a higher dollar should help their earnings. Another consideration for investors is US companies who earn all of their revenue domestically. They should avoid some of the negative impact described since currency doesn’t directly factor into their revenue. These are usually small cap companies that don’t have a global business.

OK, so global companies and global central banks will feel a headwind from a strong USD. But are there any other impacts to investors from a strong US dollar?

Ah yes. A US person, when investing internationally, whether its stocks, bonds, or even real estate, should not only look at the fundamentals of the investment such as cash flow and the balance sheet, but also how shifts in currency can impact their return in dollar terms. Meaning, if a stock is foreign, their stock price in US dollar terms can rise or fall simply from currency changes.

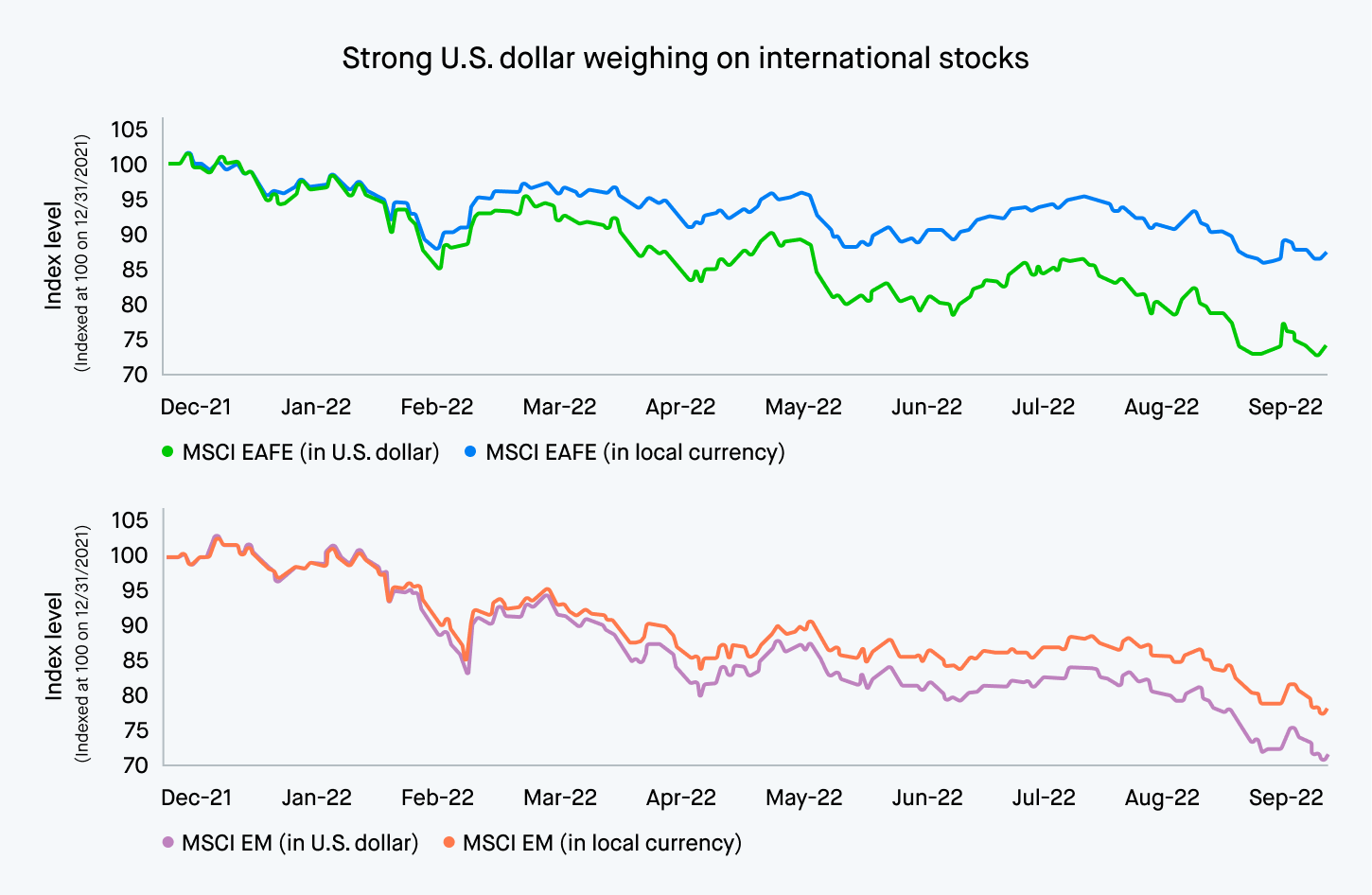

Here’s an example of that. We looked at two international stock indices: MSCI EAFE for developed international markets and MSCI EM for emerging markets. In both cases, you can see the returns in US dollar terms (green and purple) are quite a bit lower this year.

Will this continue?

Thinking ahead, expectations for year-end interest rates are around 2% for Europe, 0% for Japan, and 4.3% for the UK. All are still below expectations of the Fed’s hikes to 4.5% by year end, so I don’t see a world in which the USD will weaken much in the next few months.

So like Halloween and the markets, the dollar can also make one smile or be scared. For this year’s costume, I am choosing fun over fear — we’ve got enough to grit our teeth over.

Source: Board of Governors of the Federal Reserve System, Factset, Goldman Sachs, Federal Reserve Bank of St. Louis, Bloomberg.

First chart: Board of Governors of the Federal Reserve System (US), Nominal Broad U.S. Dollar Index [DTWEXBGS], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/DTWEXBGS, October 17, 2022