Recap of the first half

Recap of the first half

This is not news, but headlines can lead you astray. Read only them and you could believe exaggerations, or even simply things that are untrue. But read an entire article, or several on a topic, and you usually, and finally, get the real deal—opinion starts to be mitigated. For example, I saw a headline that the White House wants to block sunlight. Of course, my immediate reaction was to think “well that seems fraught with peril.” But as I read various full articles on the topic, the headline became less and less accurate to the story. It soon became clear there was no imminent action to throw a tarp on the sun (so to speak).

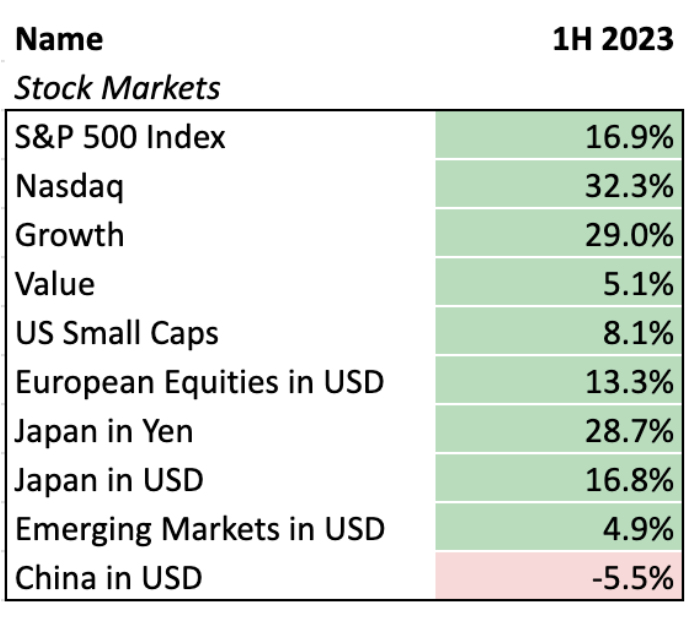

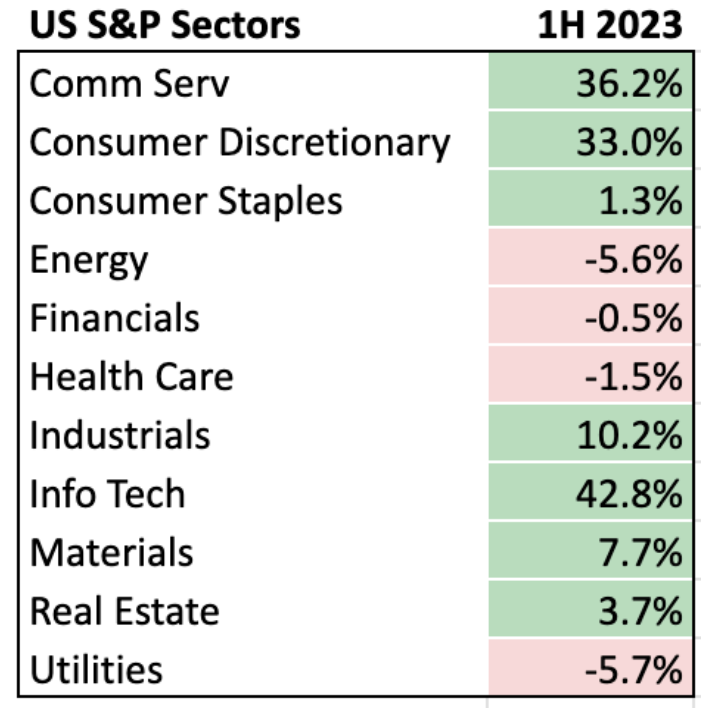

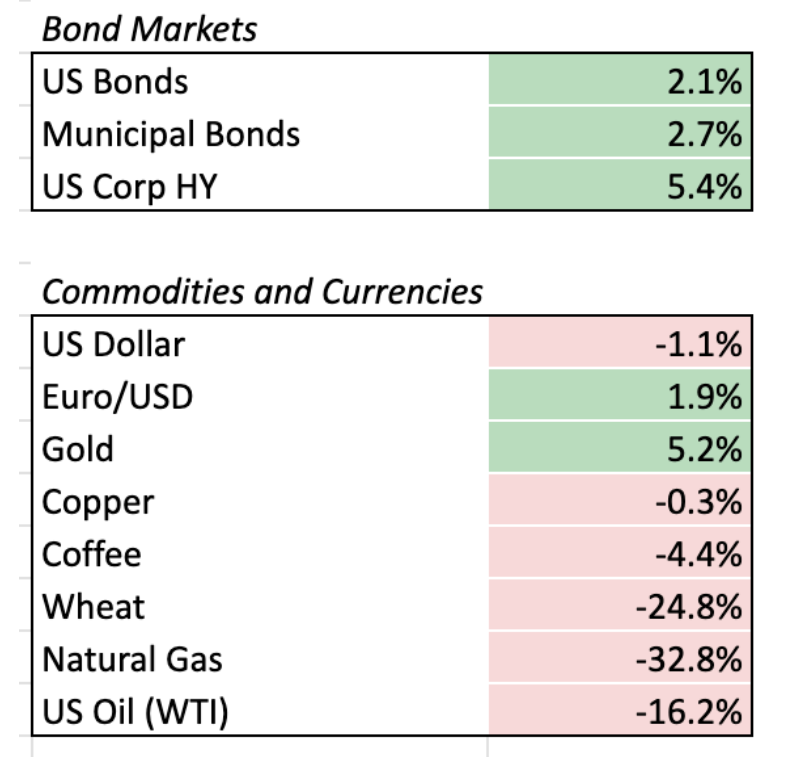

The same can be said for markets. As we closed out the first half of 2023, many articles are touting a strong 6 months, remarking that dire predictions were simply not correct. While there have been investment opportunities this year, blanket statements of a broadly strong market are not quite accurate. So to help provide a more refined picture of the markets so far this year, below is a snapshot of returns for 1H 2023 (12/31/2022 to 06/30/2023) by sector and region. No opinion or headline necessary—just the facts. : )

Source: Bloomberg, Robinhood Financial. Growth, Value and US Small Caps represented by the Russell 1000 Growth, Russell 1000 Value and Russell 2000 Total Return Indices, respectively. European Equities represented by the MSCI Europe Total Return Net Index, Japan represented by the Nikkei Index. Emerging Markets represented by the MSCI Emerging Market Net Total Return Index. China represented by the MSCI China Net Total Return Index. US Bonds represented by the Bloomberg US Aggregate Index, Munis represented by the Bloomberg Municipal Bond Index. High Yield represented by the Bloomberg US Corporate High Yield Index. US Dollar represented by the US Dollar Index. All returns in USD unless otherwise noted. Commodity returns are represented by their front month contracts except Gold, which is spot price.