The “fab five” and something I’m worried about

The “fab five” and something I’m worried about

It’s selfish to think you can do it all yourself. It’s always a team effort. Right?

But then I hear speeches from successful people, like Snoop Dogg (“I’d like to thank me”), Issa Rae, and Taylor Swift, and I wonder, can a few give themselves credit, for the many? And own it? The market thinks so. Five of the six largest tech companies can take credit for 80% of the 3.7% return from the S&P 500 so far this year. This lack of diversity is similar to what we saw in 2023 with the “magnificent seven,” which includes the mega-cap stocks; Apple, Microsoft, Amazon, Google, Meta, Nvidia, and Tesla. However, this year so far, it’s more like the “fab five,” with Apple and Tesla recently reporting disappointing Q4 earnings and guidance on the future, and falling in value.

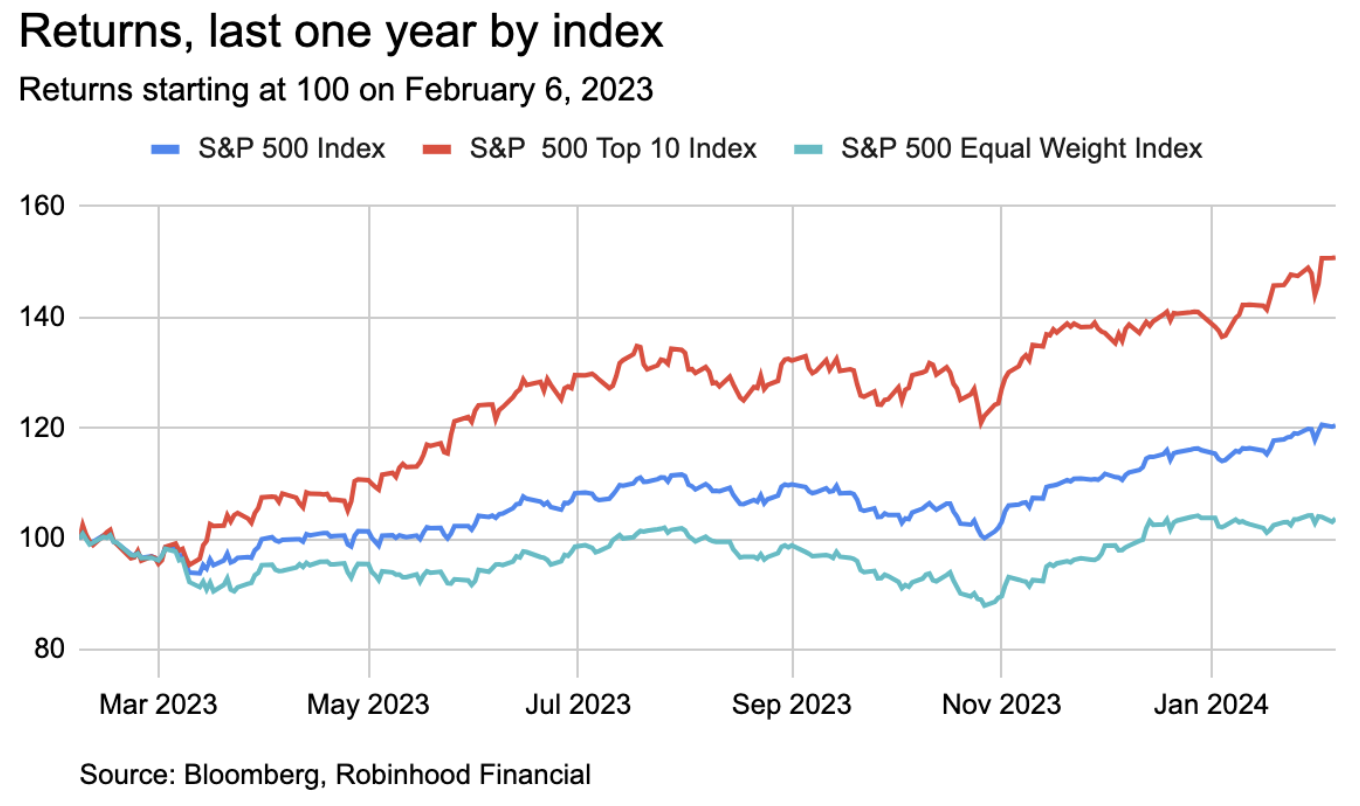

Meta alone increased their market cap by $200bn last week on Friday (that additional market cap is greater than 93% of the companies in the S&P 500). The last time we saw this type of concentration was the 1950s into the 1960s. Looking at the earnings contribution from these five, it’s not unwarranted. They have contributed 425% of the S&P 500 earnings growth for Q4. Sectors like financials and energy bring that growth number back to a lower 1.2% number for all the companies in the whole index so far. Here’s a one-year chart of the S&P 500 Index (blue), the top 10 stocks by size in the S&P 500 (red), and an equal-weighted S&P 500 (where the biggest companies have the same weight as the rest, in turquoise). You can see just how big the return gap is for the biggest companies.

Will it continue? I think it can for a bit longer. While I’d love to see greater diversification in stocks that contribute to positive returns, there are headwinds in play in many areas of the market outside of tech. This includes falling inflation which is a headwind for revenues and sticky wage growth (a headwind for costs). This puts pressure on margins—a headwind unless and until growth increases or costs are cut. And all of it makes the growth in mega cap tech stocks still look interesting.

Also on my mind, is a threat to inflation here continuing to cool: Due to rising conflict in the Middle East, global trade is being impacted, increasing the cost to ship goods from Asia to Europe and the US. According to data from Bloomberg, Suez Canal passages are down 68% since December, while Cape of Good Hope passages are up 4x to compensate, making shipping times longer. There have also been droughts around the Panama Canal, affecting shipping routes. Thus the cost (and time) to ship goods from Asia to the West has more than doubled since December, see below:

So while shipping costs are not nearly as high as they were in 2021, if they continue to increase, this will either increase inflation for us or reduce earnings for companies if they can't pass on the increased shipping costs (or both).

We’ll continue to watch how these individual areas contribute to the many. In the meantime, I’d like to thank me, for sharing this with you 😉.