Running out of time: the US debt ceiling

Running out of time: the US debt ceiling

Part of one of my favorite phrases is “time is a non-renewable resource.”

It’s a good reminder that you can try to make more money and collect more things but you can’t go back in time—and for all of us—it is inevitably limited. And many times, if you don’t remember this tenet on your own, something in life will remind you.

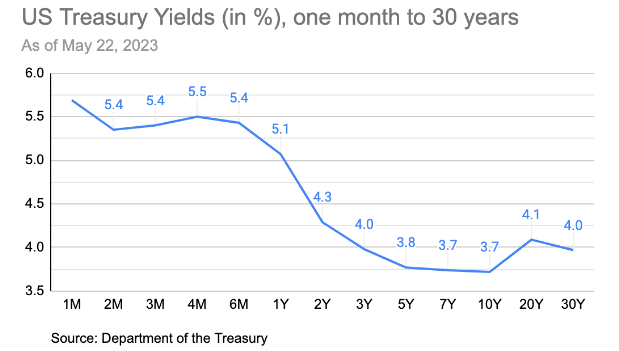

In investing, time is an important factor. Timing markets and investments can be helpful but time in the markets, as they say, can often be the real path to growing wealth (among other things). In addition, time matters not just in the stock market but also in the bond market. When a bond matures, for example, is a key part of a decision to invest and plays a role in its future value with respect to changes in market interest rates (a concept called duration). And as of this writing, time is playing a key role in the temperament of market participants. It’s as if a giant clock is looming, counting down the days between now and “early June,” when the US Treasury runs out of enough funds to keep things BAU at the US government. So far, stock market participants have noticed, but haven’t stopped what they're doing or raised eyebrows quite yet. The bond market, on the other hand, has noticed and the rates on treasury bills set to mature in the next few months are higher (around 5.4%) than those maturing further out (3.7% in 10 years, see chart below). In addition, credit default swaps (CDS), which measure the probability of a default on debt, for the US have increased from 11.7 at the start of the year to 145 today.

Will the US actually get to a point where there is no deal or suspension by the time the US government has to pick what it pays for? I still think no… and still think a temporary suspension of the debt ceiling could be the near-term “deal” (see my April 24 piece). But honestly, the chance is non-zero now with such little time left.

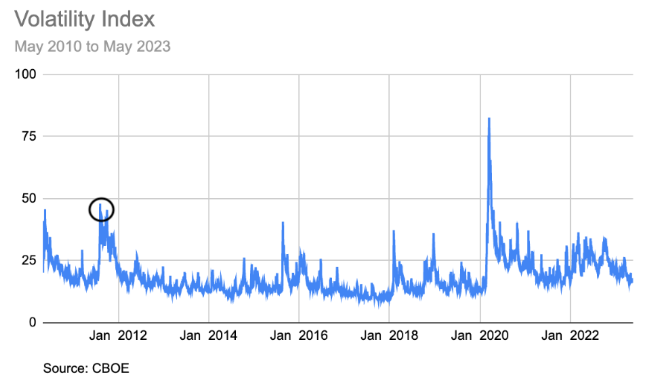

What could happen if it breaches? So that the government could focus on paying their most important bills (external debt in the form of treasuries), parts of the government would likely shut down until an agreement is reached. The US reputation on the global financial stage would probably deteriorate. And with the equity market not really moving on this risk yet, it would likely start to, in a downward direction. Correlated to this, the Volatility Index (VIX), a measure of short-term volatility in the equity market, has been hovering around low levels (17) (whereas in 2011 when we last had a similar debt ceiling risk, it rose to the 30s). So, you could see this rise quite a bit. Short-term interest rates would probably rise further and you could see other assets, like gold, and currencies rally as cover to risks in the US. That being said, like in 2011, the market would likely eventually recover as and when a deal inevitably happens.

Sidenote: The current markets and economy are sooo different from 2011. The Fed had rates at 0% in 2011 vs the 5% today. Inflation was 2-3% then vs 5% today. Equity valuations were moderate vs. on the expensive side today and market leadership is weak—meaning the breadth of stocks that are leading it is narrow vs. broad.

What if there is a deal? While that reduces the risk described above, there are other considerations. A deal will likely mean less spending somewhere. Recent legislation like the Inflation Reduction Act and the CHIPs Act, which provided benefits to certain sectors like the green/climate space, certain healthcare industries and semiconductors, could see some risk. Another place to consider impact is in companies that are sensitive to changes in defense spending. This is up for debate now in negotiations but something to watch.

Lastly, another point to note is that while the Treasury has been waiting for Congress and the White House to come to a deal, there has inherently been more liquidity put in the system. This has been to extend the life of current funds as much as possible. Once a deal is done, this liquidity will lessen, tightening financial conditions a bit, which may reduce overall growth of the economy. It's a bit unintuitive but true nevertheless.

While there are lots of other topics to write about (like the US government looking to rebuild their oil reserves after greatly depleting them or what’s happening in the semiconductor industry), this seemed pretty timely to address (again).

See, there’s that aspect of time. Let’s hope the deal makers understand how important time is—how non-renewable it is—and get a deal done.