The wisdom of Yogi

The wisdom of Yogi

If you don’t know who Yogi Berra is, you should. He was a three-time MVP baseball Hall of Famer, coach, and manager during a career that stretched from 1946 into the 1980s (as a player, most of it with the Yankees). But he’s as famously known for his unique quotes that often contradicted from within or used tautology. You never quite knew if he meant to share that amount of wisdom with such pithiness or if it was an accident, but all of them were gold.

Some of my favorites include: “You can observe a lot by watching.” “Nobody goes there anymore. It's too crowded.” And “I really didn't say everything I said.”

Another quote that’s been attributed to him, as well as to others, is “Never make predictions, especially about the future.”

It got me thinking about the recent predictions made by global economists through the World Economic Forum’s “Chief Economists Outlook” for September. In it, 73% of the economists surveyed said a global recession was somewhat or extremely likely in 2023.

Are they right? And if so, what happens for investors?

Well, first let’s review what a recession is. Many refer to a “technical” definition of two consecutive quarters of declining gross domestic product (GDP), a measure of economic growth. We’ve actually already had that with Q1 and Q2 GDP coming in at -1.6% and -0.6%, respectively, this year.

But the National Bureau of Economic Research (NBER), a US organization that tracks economic growth, says a recession is more of an assessment after “a significant decline in economic activity that is spread across the economy and lasts more than a few months.” It also says a recession “must influence the economy broadly.” It looks at numerous measures to make a call, and most recently it has “put the most weight on real personal income less transfers and nonfarm payroll employment.” Of course, the NBER’s committee that makes the determination is retrospective — meaning something that’s called only after it’s over.

Since — based on this — a recession isn’t officially called until we’re back in expansion, we’ve built our own composite of metrics that monitor the business cycle of the US economy today relative to the past 20 years. My team and I have divided this in to three types:

A leading score includes indicators that first show the change of economic cycle. This includes things like business surveys and building permits.

A coincident score measures the current conditions of the economy. This includes personal spending, retail sales, and home sales.

A lagging score confirms the economic cycle/trends after the economy shows a downturn or upturn. This includes job openings, unemployment, and wages.

The chart below shows the scores over time. The most recent scores for leading and coincident show signs of a down-trending economy, approaching levels seen in the past two recessions.

Source: Robinhood Financial. Shading indicates a recession.

So we agree it's likely the case that we’ll be in an official recession next year — a recession that’s already started. The piece that’s not there to make it official yet is employment, which goes in the lagging score. Employment continues to be strong, making it hard to call right now.

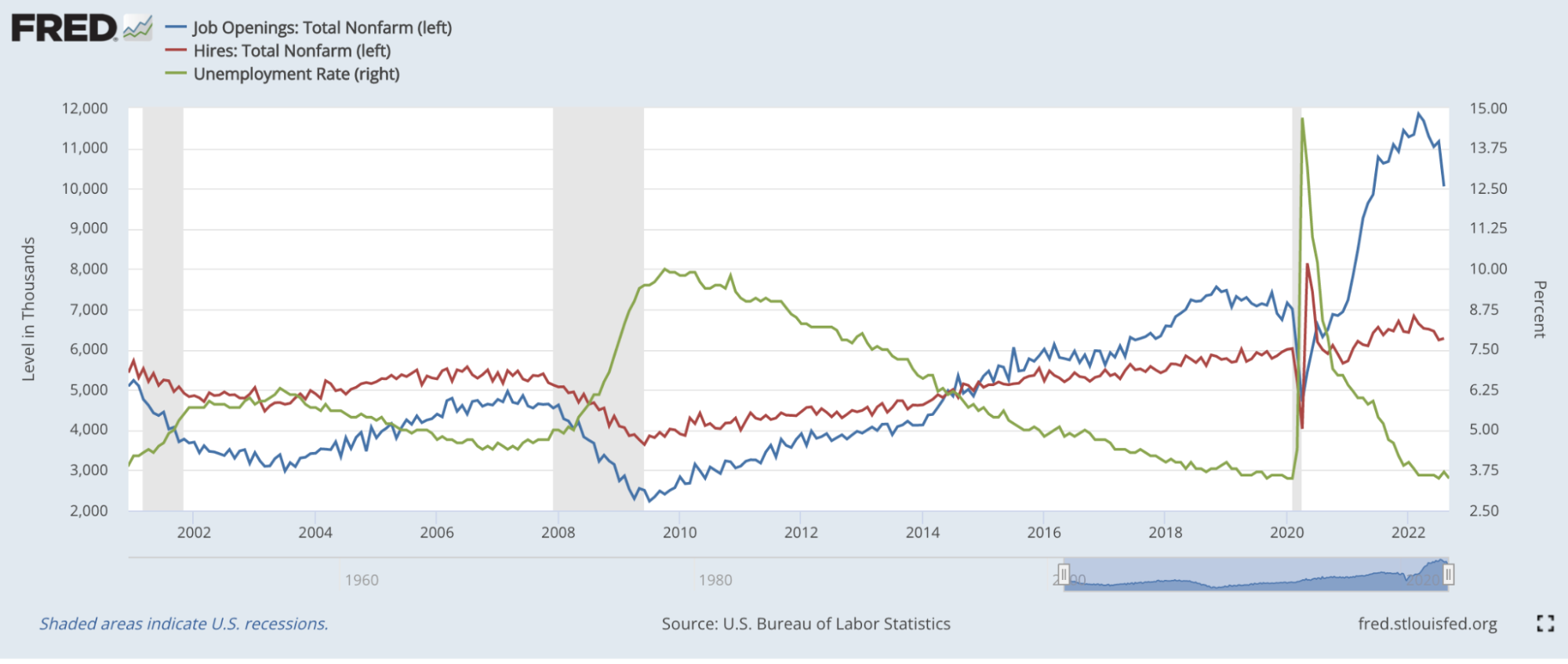

But there are early signs that it’s turning over too. See below for a chart on the job-opening rate, hires rate, and overall unemployment. New job openings tend to go away before unemployment ticks higher, and it has started to fall.

For investors, it’s important to note that markets are a forward-discounting mechanism. What I mean by that is, it doesn’t make retrospective calls. Instead, it changes based on changing expectations for the future. Waiting for employment or GDP numbers to improve — or even for the official call that we had a recession — to look for investment opportunities could mean you’ll likely have already missed the bottom.

Let me put some numbers around it for you. We studied eight recessionary environments going back to 1970. In all but one, measures such as industrial production, payrolls, and GDP bottomed on average four to five months after the stock market hit a bottom and began to rally. Said another way, historically the market has looked ahead to better days on average four to five months before the economic data shows it’s not getting any worse.

This year, most markets are already down quite a bit from their peaks, telling me they already expect a recession. The S&P 500 is down -19% and the Nasdaq is down -28% this year, through October 24, and even bonds are down double digits. But, in our opinion, they haven’t fully incorporated a recession scenario — they’re just much closer than they used to be.

What’s holding us back from saying we’ve seen the bottom? Expectations of earnings for 2023, while down from their peaks, still show a high-single-digit growth rate, which would be very atypical for a recession.

Earnings expectations are one of the last sets of data points we’re focused on before turning more positive on the market broadly. It doesn’t mean you can’t find opportunity sooner, or that adding to portfolios from cash, if appropriate, can’t potentially be rewarding now with the right time horizon. But we’d like to see this finally reset.

As Yogi said, “It ain’t over till it’s over.”

Source: World Economic Forum, Bureau of Economic Analysis, NBER, Robinhood Financial, US Bureau of Labor Statistics, Board of Governors of the Federal Reserve System, US Employment and Training Administration.

2nd chart: US Bureau of Labor Statistics, Job Openings: Total Nonfarm (JTSJOL), retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/JTSJOL, October 23, 2022.