Is the playbook working?: Interest rates and inflation

Is the playbook working?: Interest rates and inflation

Two statements have been debated in the financial media lately:

Higher interest rates are causing inflation

Higher interest rates are causing an economic boom

As I consider the statements, on the surface I chuckle at number 2—the debate practically starts with the audacity of the economy to be booming; how dare it boom! (And also, is it?)

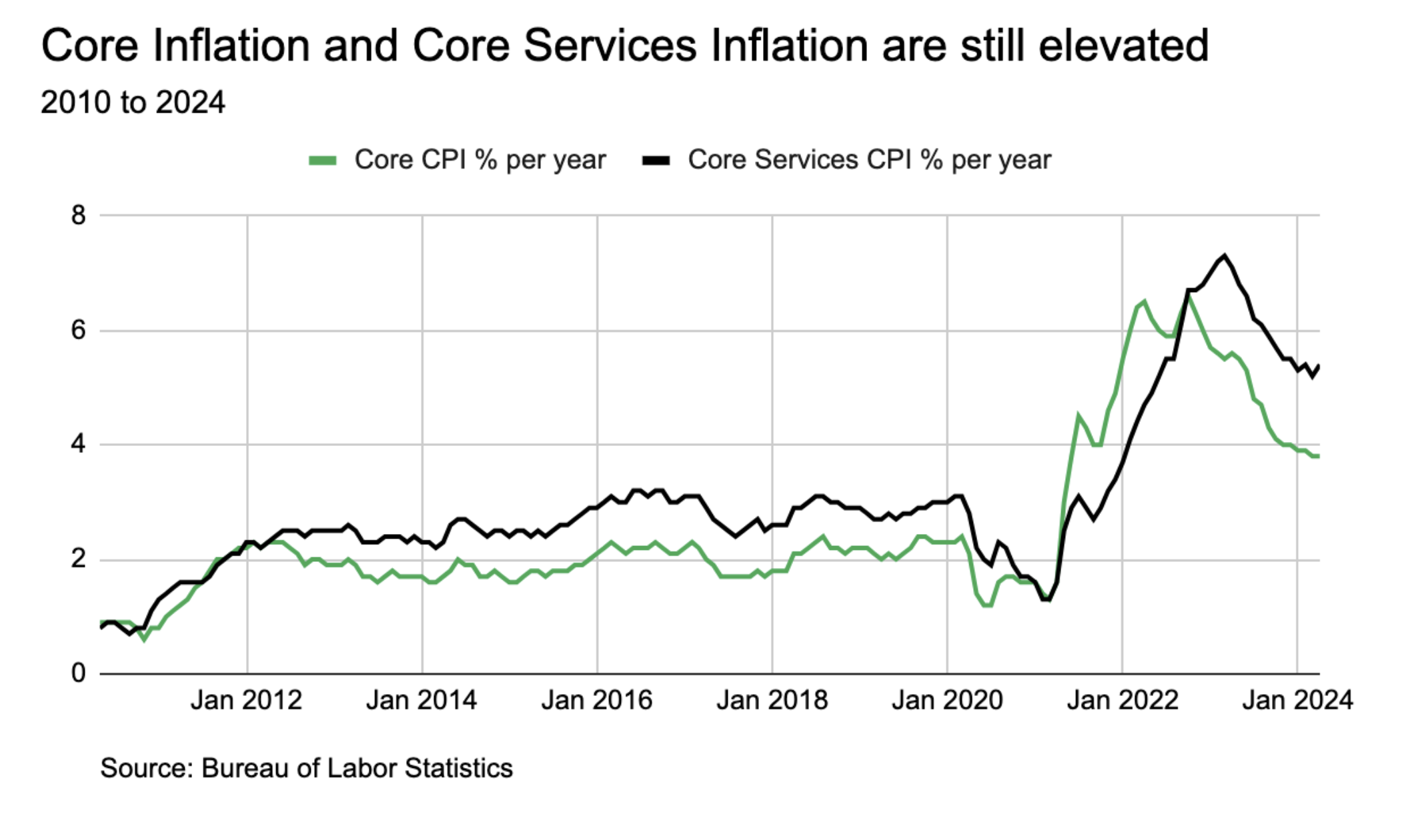

But I understand why the debate. The current play on the field by the Fed is standard under the inflation section in their playbook: raise interest rates in order to cool economic activity and, thus inflation. Since, from a high level, we still have inflation, albeit lower than its peak, and we still have economic growth, albeit not uniformly feeling that way, the debate is rational. The intended effect of higher rates on inflation seems, on the surface, to be limited. See inflation below:

Does that mean there is something to the statements?

Well, one could argue that the opposite was true during the 2010s—the decade of nearly 0% interest rates and quantitative easing limited inflation. Cheap money perhaps allowed companies to price their products at low levels for the sake of revenue and/or subscriber growth, keeping inflation in check. Thus, capital did not have to go to grow wages. And since cash earned investors nothing, there was no cash return to compete against, so they didn’t scrutinize bottom-line profits as much.

With higher rates today, cash earns around 5% now. This raises the bar for companies to earn a higher return for their investors, and could incentivize them to raise prices, creating inflation.

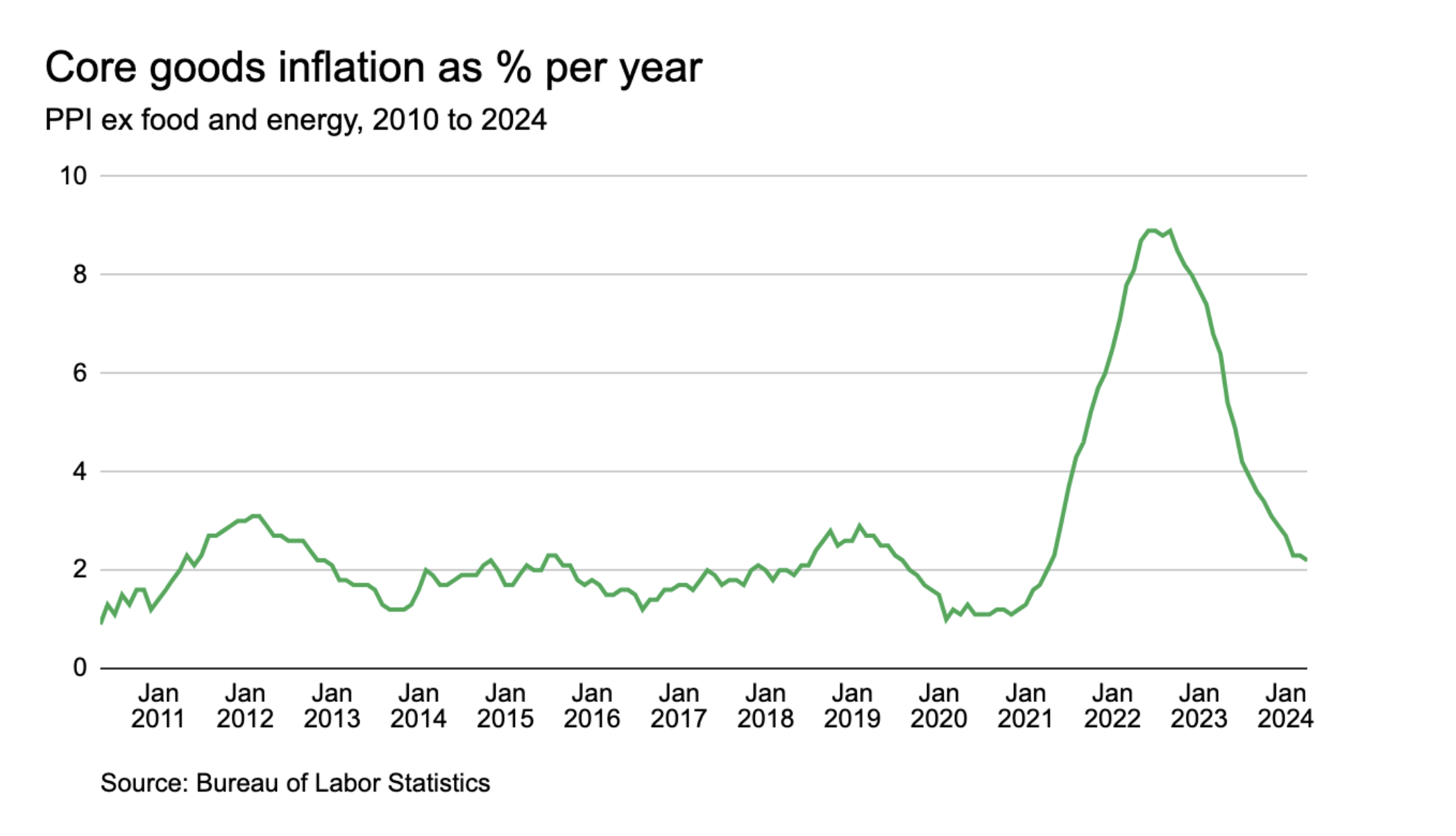

So is this what is going on? I believe at the beginning of a higher-rate environment this may have been true. But eventually this only works if demand stays the same in the face of higher prices. If it doesn't, sellers are forced to, at least, limit price increases. And that has happened to some extent, at least when you look at goods inflation (see chart).

So more likely, in my opinion, the reason we still have inflation (and related economic growth), despite higher interest rates, is largely due to the fiscal stimulus present in the economy, which is historically unprecedented for a non-recessionary time.

Let me share some logic here and a chart to show the current nature of the fiscal stimulus relative to history:

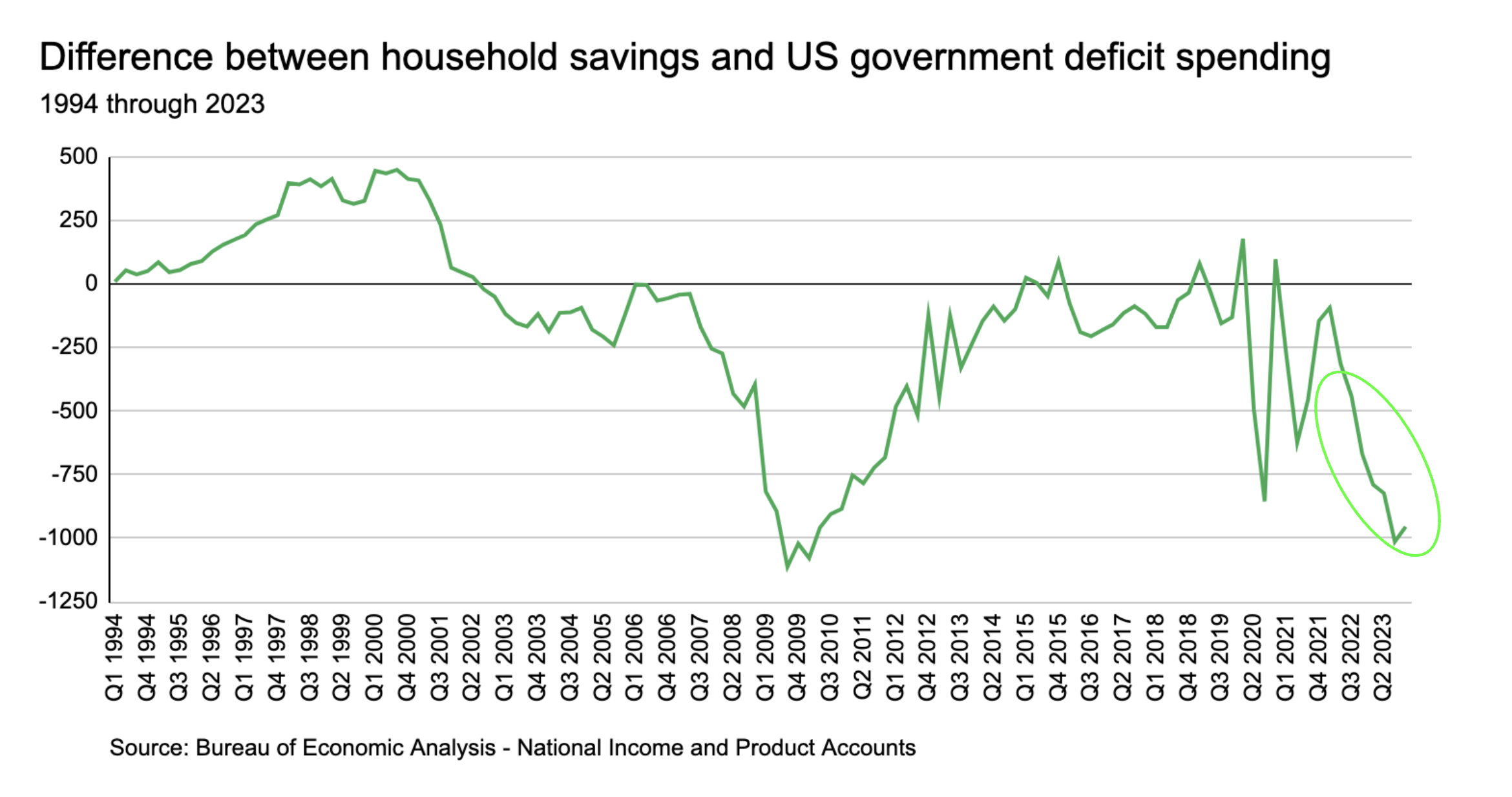

How government budgets tend to work:

In general, households tend to save and grow their money for security, stability, optionality, etc. This may be at varying levels throughout history, but there has always been aggregate savings from households.

Since savings from households is like withholding from spending into the economy, governments typically engage in deficit spending to offset the savings (aka withholding) from the household sector.

Since this is an offset, the amount of deficit spending the government does has historically been about the same as the amount of savings in aggregate from households—except during quantitative easing.

Check out this chart going back to 1994 showing the difference between household savings and government spending. It has historically hovered around 0. But note how much deficit spending is taking place today, despite that we are not in a recession or just coming out of one (circled).

^ This level of deficit spending is what I believe is the undercurrent fighting against all the efforts of the Fed—and why we still have inflation. Not because we have high interest rates.