A crush, but not the bae kind

A crush, but not the bae kind

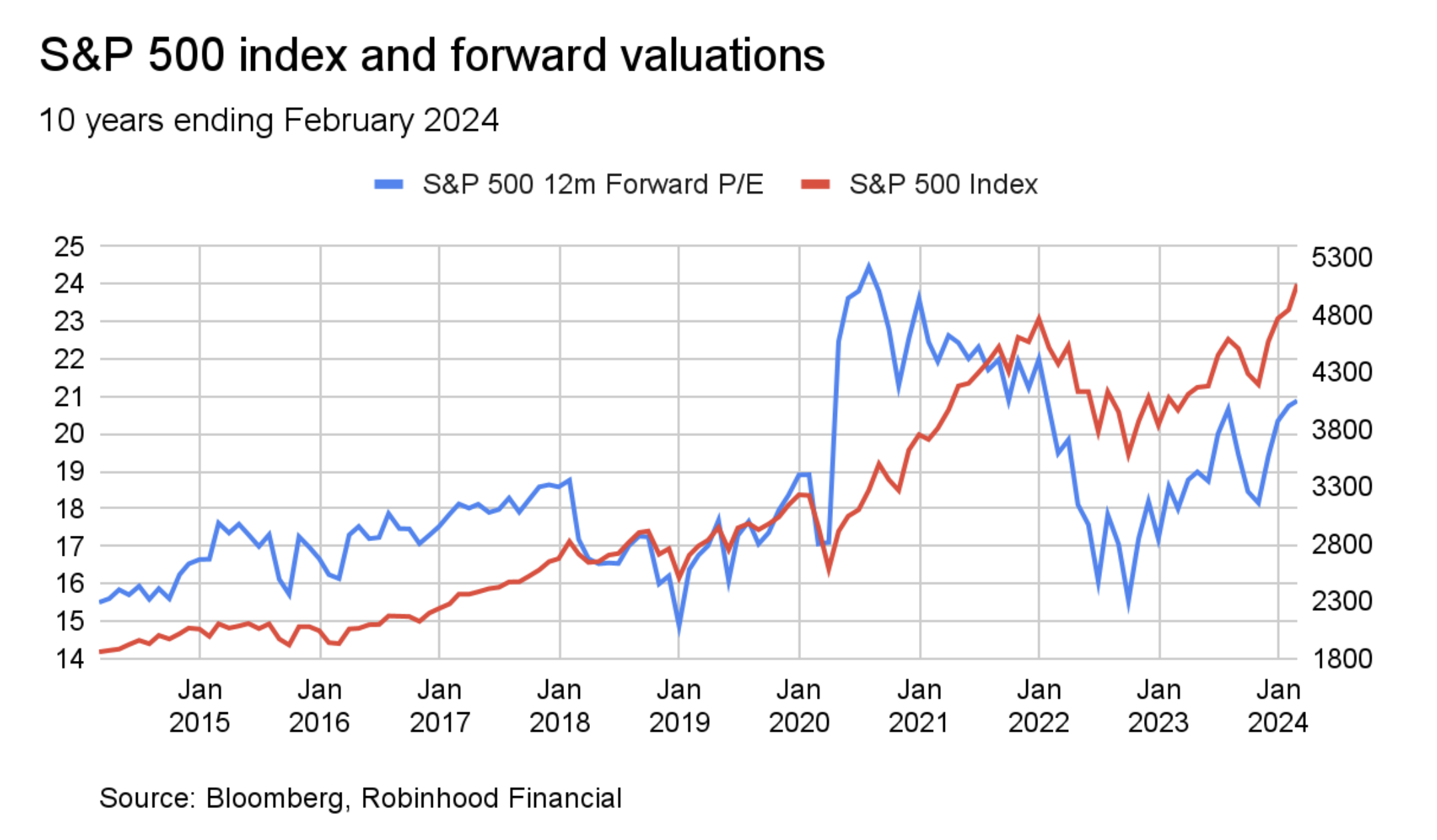

Markets are up beyond most Wall Street strategists’ expectations. We started the year with the S&P index at around 4750, when the median Wall Street S&P estimate was to end the year at that same level. We are two months in, and even the most bullish Wall Street strategist is looking like they could be “wrong,” with the S&P above 5050. And mea culpa—I, too, thought we’d see a correction this first half, driven by high interest rates and overly ambitious earnings expectations, before getting to higher market levels to end the year. It could still happen but each day that passes is one less day it won’t.

And a rising market where valuations are high relative to history can be both loved and hated at the same time. A market moving higher is well-received but higher valuations can make Wall Street nervous, since they have historically been eventually corrected back to fair, or even cheap levels. But it’s important to note that valuation is usually a poor barometer for timing the market. The chart below shows how right now both valuations and markets are high.

Despite the disagreement between strategists and the market trajectory, broad stock market volatility has stayed muted relative to history. The Cboe Volatility Index (VIX) is at 13.7 relative to the 10-year average at 18.1. But this masks that stock-specific volatility maintains higher levels (always does). And in particular for the last several weeks, due to earnings season. After all, volatility is a measure of how swiftly changes in price occur—up or down.

Broad stock trading volume is up in general, as is options volume. Putting the two together—stock specific volatility and greater volumes— reminded me of something that can commonly happen and is worth knowing about:

Volatility crush.

This is not love for volatility. First, options prices are impacted by several factors but mostly:

time to expiry,

implied (aka expected) volatility, and

the current price of the underlying stock or index relative to the strike price of the option

Now it’s natural to expect that buying a call option, for example, on a stock before their earnings announcement, and then seeing the stock price go up after a good earnings report, could lead to the value of that call option increasing.

However, what can be missed is the 2nd bullet point above. Buying an option means you also “buy” the implied volatility. And implied volatility can rise in advance of a highly anticipated earnings report. Once the news comes out, the volatility can fall. So, while the market value of the underlying security can rise, the “value” of the volatility can fall, which, if it’s a big enough drop, can mean it may offset the potential benefit of the rise in the underlying stock price. This is referred to as “volatility crush.”

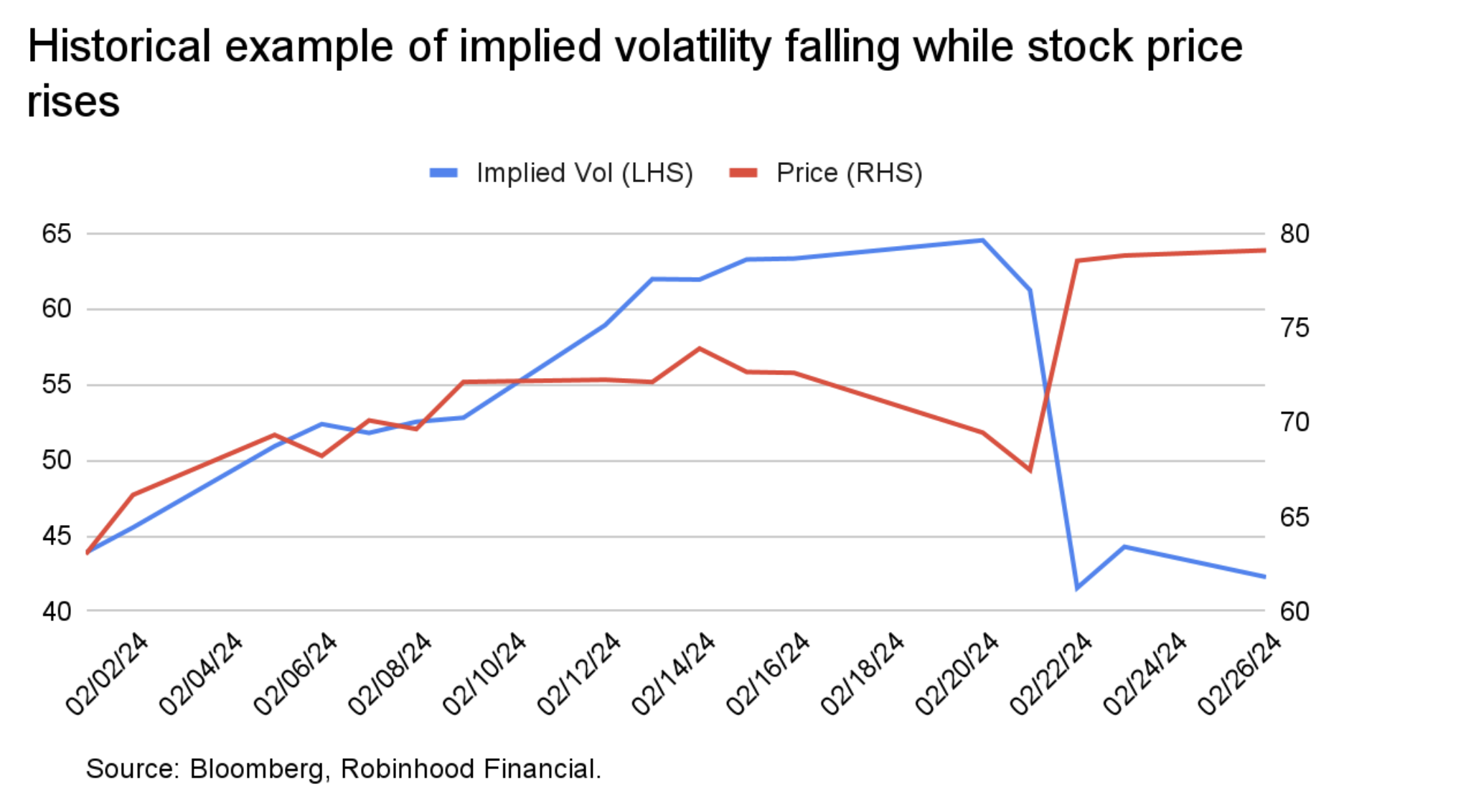

Here’s an illustration for a call option of an unnamed stock last week. The company reported earnings on February 21. The implied volatility fell right after the report, while the stock’s price rose. Not shown here but the call option value was not up as much as the stock was.

It’s no fun to experience, but as we explain more thoroughly in this article, checking the implied volatility of an option relative to the history can be a good idea to try to avoid disappointment.