What’s up (or down) with inflation?

What’s up (or down) with inflation?

Many times in life you go through periods that feel like there is practically a sole topic everyone around you is talking about. Then one day it starts to fade, and suddenly you realize it’s been so long that you can look back on that time like “remember when?”. For me, that was my sticker collecting days as a kid, getting my hands on the “parental advisory” music as a teen, and as an adult, most recently, Covid’s impact on all our lives.

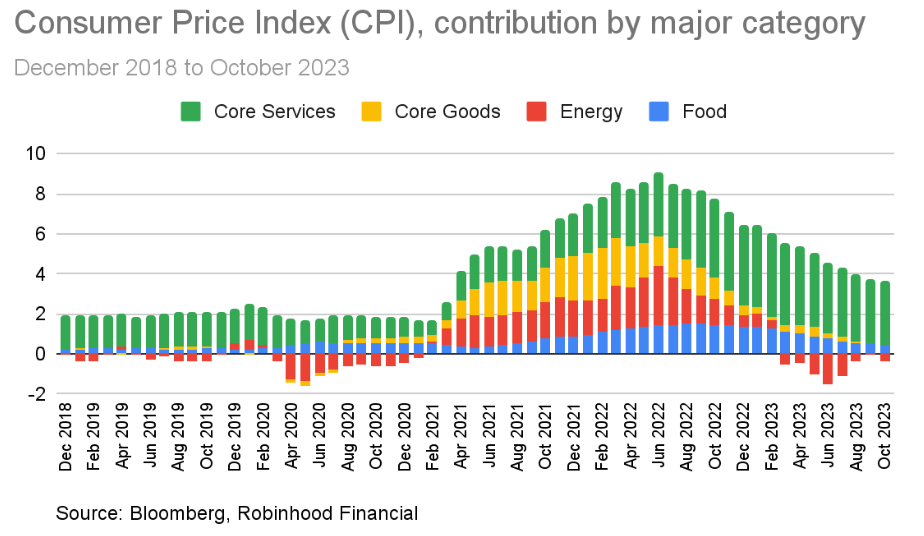

I would say inflation could be heading to the same status. It’s not gone, but it’s no longer at a peak in the vernacular. And that’s because the data itself has fallen from a peak (in most parts). Here’s an outline of inflation data over time, by category:

Yesterday’s most recent publishing of year-over-year inflation data continued the falling trend, coming in at 3.2% overall and 4%, excluding food and energy prices (aka core)—the latter of which is the lowest reading since September 2021. Even core services prices (vs. goods prices), which the Fed cares most about and have been the most stubborn, showed a small drop.

The markets high-key celebrated this (e.g., the Nasdaq was up over 2% and small cap stocks rose over 5%), mostly to rejoice in what felt like more certainty the Federal Reserve is unlikely to raise rates any further. While we have had the expectation that the Fed would be done hiking for a while, I am pretty sure DJ Powell isn’t going to stop cautioning the market. At least not until inflation is closer to their long term inflation target, which is still 2%. So not quite out of the conversation yet.

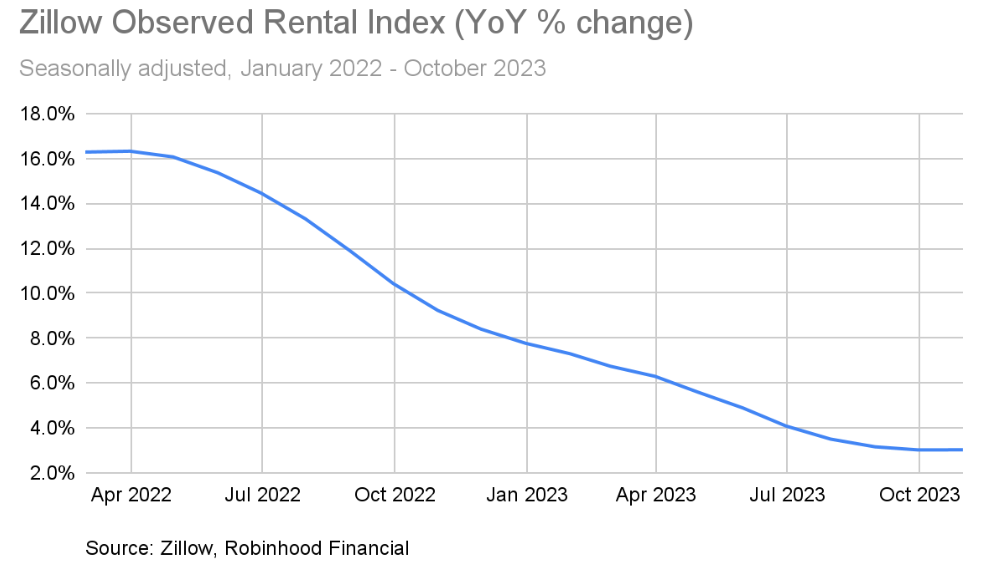

As we said last week, this rally could have some legs but it’s still tough to see it making big new highs—since the other side of lower inflation is slowing growth. One of the biggest contributors to core inflation, shelter (aka home and rental prices), should fall as the Zillow Observed Rent Index is already reflecting a softening (see chart below)—and slowing growth.

As I was thinking about this, I expect inflation to continue to fall, but unlikely to feel as smooth as yesterday's CPI data may have looked. At least a good thing about higher than average inflation still lingering is that limits on stuff like tax brackets and retirement contributions are often increased. For example, the IRS recently announced that the maximum amount someone can contribute to an IRA in 2024 will be $7,000, up from $6,500 this year. Saving for retirement—now that’s something I would love to make a main character in conversations…indefinitely.