Nothing’s for sure: lower rates could be coming but not for the right reasons

Nothing’s for sure: lower rates could be coming but not for the right reasons

There are so many things that are easily counted out. Things that you think for-sure could never happen. And you plan your life around that certainty. But the universe laughs at those notions. Because nothing, especially in investing, is for certain (well, almost nothing).

Like back in November when the market took it as a certainty that the Fed would start cutting rates in March of this year. It’s May and there have been no cuts.

However, it might be getting closer. The Fed Reserve Chair, and DJ for the markets, Powell, made remarks yesterday that were biased toward a likelihood of Fed cuts at some point this year (aka dovish, these remarks are always made in terms of birds). He believes the disinflationary process will resume while the odds of another rate hike are low.

This, coupled with the coolest inflation report since April 2021, multiple retail companies (including Home Depot this week) reporting a slowing in consumer demand, and a weaker than expected retail sales report, combined with the high volume of rental home construction in 2023 potentially starting to place downside pressure on rental rates, leads to Mr. Powell potentially being right.

Of course, everything still feels expensive, and inflation is still, in an absolute sense above the 2% target, coming in at 3.6% for “core.” Services inflation is also still elevated at 5.8%. This means there is still some waiting to do on the part of the Fed, even if a rate cut may be closer now (I think September or December might be in the cards like the market believes now).

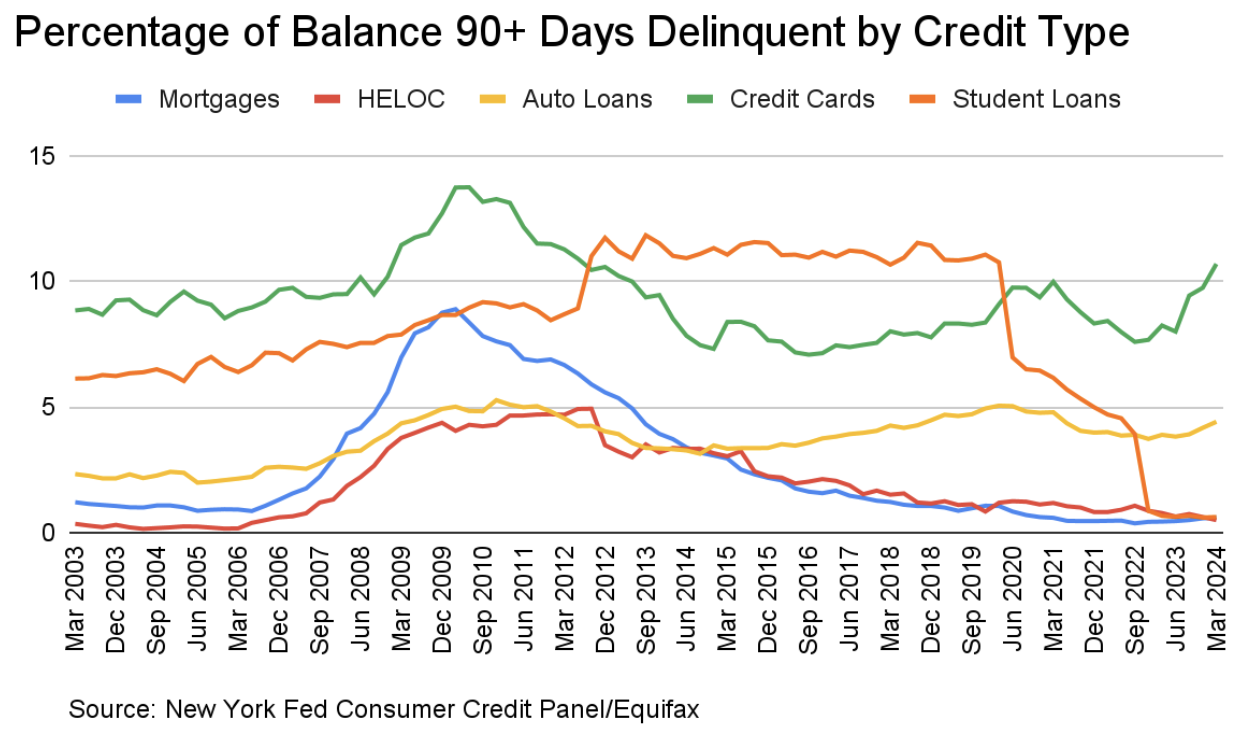

This concept of the consumer, in aggregate, slowing down is something I am watching closely now. The New York Fed published its Q1 report on household debt, revealing an increasing number of borrowers missed credit card payments (check out the green line in the chart below).

So instead of inflation being the real threat to the market, the impact of inflation on the consumer, and thus resulting slower growth, is a larger threat to stock values in my view. Right now, while retail stocks have reflected slower growth, this is not yet in the risk/reward calculations of the broad market. Perhaps it’s because tech and AI are typically more immune to this and they have been leading the market. But expectations here are already high. While stocks will welcome any drop in interest rates in the short term, thanks to potentially cooling inflation, eventually, further drops in rates driven by much cooler growth could spur anxiety in stocks.

So there’s another thing to not fully count on—that much lower rates will lead to a stock rally. It all depends on why they are lower.