Checking in: Earnings so far

Checking in: Earnings so far

It's the small things that often matter. You might have a friend who asks how something you mentioned a while back turned out. That small inquiry not only checks in on you, but communicates they made space for you in their brain when they didn’t have to. When this happens, I often think memory, like this, is love.

Memory, too, is just as important in caring for a portfolio. Remembering what you did and why can help you decide if that’s still the right choice. In that same vein, here’s an update on the post I shared at the start of earnings season—and consideration of whether my own view at the time still works.

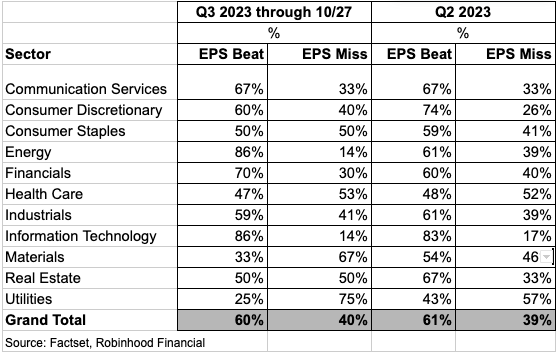

So far, Q3 earnings season has been tracking similarly to Q2 earnings season when it comes to earnings per share (EPS) “beats” and “misses” relative to expectations. According to Factset’s Earnings Insights, S&P 500 companies have reported earnings that are 7.7% above expectations (beats)—and above the 1-year and 10-year averages. You can see in the chart below how at the aggregate level, the percentage that beat and missed (60% / 40%) are similar so far.

Looking at each sector above though:

The consumer sectors are a bit worse so far this quarter, with less “beats.” However, more than half of them still have to report, which could turn this around. The same can be said for the materials and real estate sectors.

Energy and financials are tracking better, with the former having more reports to come.

Despite this not-bad-so-far outcome, the market has been dropping since earnings started (-4.8% for the S&P through Friday 10/27). Earnings have not been providing the typical positive addition to sentiment that I thought they would. Why? Simply put, it hasn’t been enough. In light of the overhang from higher interest rates, higher oil prices, and geopolitical conflict, investors want to see more positive talk about the future. In addition, while revenue estimates (expectations for what a company will make before considering costs) for next year have stayed about the same, earnings growth estimates (what they will make after costs) have fallen—most notably in consumer discretionary, financials, and communications services. This tells me that costs are expected to be higher in 2024, which is adding to anxiety.

Looking through which companies will report over the next couple of weeks and some technical indicators, I think the market could turn up in the near term. It feels a little oversold after last week. Plus, interest rates could fall some in the near term. A recent report from the US Treasury showed the government would be borrowing a little less than originally expected this quarter, and the Fed will likely confirm later today that they don’t plan on raising interest rates again soon.

But I still think the bar (and risk) is higher for next year.