Words are just sounds, but rates are important

Words are just sounds, but rates are important

There are several words that start to sound strange when you say them over and over. One for me is “scalp.” It’s a one-syllable word that conjures up so many pictures in my head. Say it enough, and it starts to sound odd.

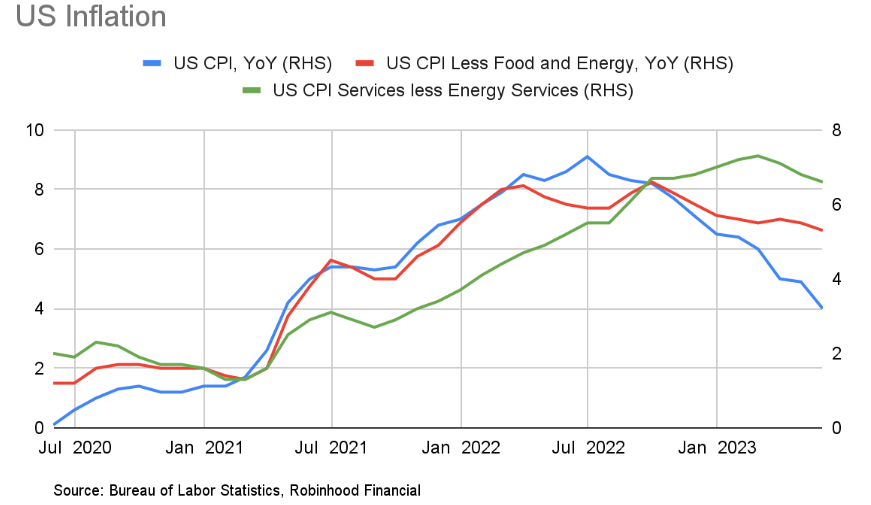

Inflation is another word I have been saying a lot these last several years. It doesn’t have the same strange effect as other words but it certainly has elicited feelings and impacted wallets. Luckily, it hasn't been rising faster lately. In fact, “headline” inflation peaked last July, while “core” inflation (which removes the effects from food and energy prices from headline) has leveled off.

You can see in the chart’s blue line above, which includes yesterday’s inflation update, broad annual inflation (Consumer Price Index or CPI) has been falling since July 2022, mostly thanks to energy prices. However, the red line, which is core inflation, is also visible, and has fallen, but not as much. Finally, the green line, which tracks the price of core services in the US (vs goods), has only fallen a touch recently. This green line is the reason Jay Powell at the Fed is likely to keep interest rates around the current levels for the foreseeable future—in an effort to cool this part of inflation.

Remember, the Fed has two mandates—to keep inflation low and employment as strong as possible. Since employment has stayed stable, inflation continues to be the Fed’s boss for now. The Fed will provide an update today on how they see things.

But there are many concerns that come from higher, sticky inflation—which the market has been trying to ascertain. They include: are we heading towards a recession, because the Fed will slow us down? Or are we in a period where the labor market will remain naturally strong due to demographics, and the Fed won’t really be able to lower the very services-inflation that good employment creates?

It’s certainly getting harder to claim we’ll be in a recession soon. Even despite the troubles in the banking sector, many data points show it may all be okay for now—including stock market moves, company earnings, and employment.

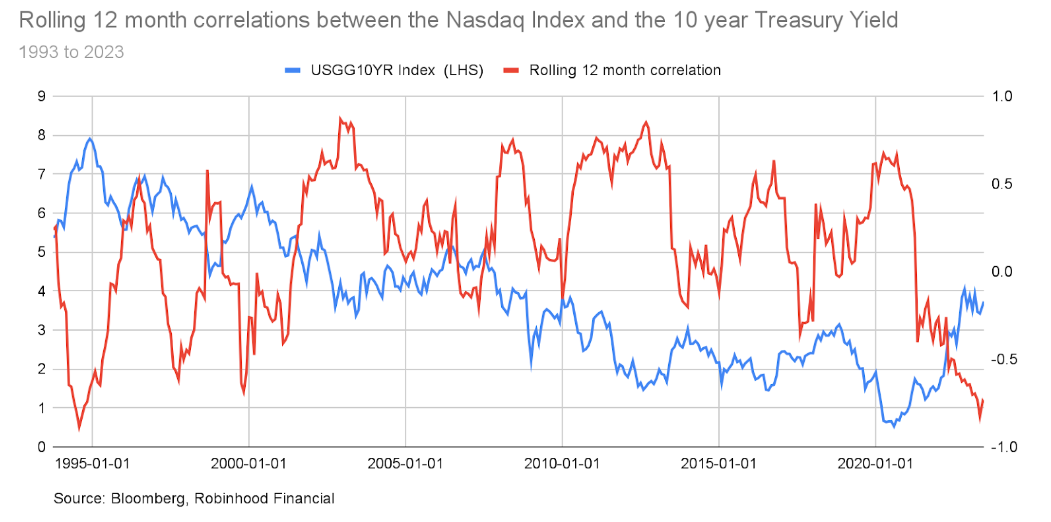

I do, however, think rates will be naturally higher than they have been for the last decade or so. With this view in mind, I looked at the correlation between markets (in this case, the Nasdaq Index) and interest rates (the 10 year) for the last 30 years. Correlation lets you know the direction of a relationship—meaning if one piece moves up, what direction and to what degree does the other move? If the result is +1, that means they move perfectly together. For -1, it's the opposite. The other premise to know is, generally speaking, when rates are falling, stock values tend to go up (all else equal). Here’s the correlation analysis (in red):

I also included the 10-year treasury yield (in blue) for context.

I see three things in this chart:

Since 2002, when the Fed first took rates down to a level not seen before, the correlation between changes in rates and markets was generally positive (above 0).

Prior to 2002, when rates were higher, correlations between changes in rates and markets were negative (below 0), on average.

And it just so happens that the most recent correlation data is very negative, while rates are higher.

My view is that when the Fed didn’t have to worry about inflation and focused more attention on growth and employment (from 2008 to 2021), the resulting interest rates on cash were so low, it incentivized risk taking—like investing in the stock market. There was little return to give up by moving out of cash and into other things. Today, there should again be a more naturally negative relationship between markets and interest rates since investors can earn something while sitting in cash (just like the 1990s). Watching interest rates, and their direction, will be a more important key to the future of investing than it was in the last decade-plus—reminiscent of the environment 30 years ago.

There’s a word—reminiscent—that I don’t use enough. And it doesn’t matter how many times you say it. It doesn’t change. Just like the past.