The markets and culture of Japan

The markets and culture of Japan

It starts small. You hear someone talk about it on Insta or a friend of a friend mentions it. But then, you start to hear about it more. Maybe from a news source or a second friend. So you get curious and do a search for it. And suddenly, a whole world is opened. For me, that was Japan.

I mean, of course, I had heard of it. It was a country of the world. And our own country has quite a past with it. But ever since the 1980s, my curiosity has only grown—to bucket list status.

But let’s back up. Japan was a growing global economy from 1970 through 1989. Their stock market was up quite a bit (1,875%), while the US stock market languished from high inflation for much of that period. Japan and Japanese companies owned many businesses and real estate everywhere. Even the famous Rockefeller Center in NYC was bought by Mitsubishi in 1989—my first personal encounter with the country, albeit at a young age. The purchase was talked about quite a bit.

Who knew in that year, however, that it would be a sign of the peak of the country’s economic domination. Like many things that fly too high, they eventually come down. Below is the Japanese stock market from 1970 through 2012.

For much of the remaining decade, Japan had become a market deemed practically uninvestable. From 1989 to 2012, Japan’s stock market returned -3.9% per year. It was plagued with stubborn deflation (the opposite of what we have today) and structural issues, such as the oldest population in the world, virtually no immigration to bring in younger workers, and limited participation in the labor force by women. If it wasn’t for the movie Lost in Translation in 2003, I might have stopped paying attention altogether.

But then, in 2013, the same year Anthony Bourdain visited Tokyo in Parts Unknown, reigniting my desire to see it for myself, “Abenomics” was born. Under strong pressure by then-Prime Minister Shinzo Abe to take bold steps to beat deflation, the Bank of Japan signed a joint statement with the government in 2013 and committed to achieve a 2% inflation target “at the earliest date possible.” The pledge served as the backbone of the seemingly radical monetary stimulus and justification for keeping Japan’s interest rates ultra-low today, even as other central banks increase interest rates to combat stubbornly high inflation.

Abenomics had three “arrows”:

1) a huge amount of quantitative easing (QE), more than we had here

2) a target rate of 0%

3) social and corporate governance changes

While I’m sure his policies were not always agreed with by his people, they were direct. Abe aimed to break the issues in their economy after many decades. In particular, the “third arrow” was aimed at the structural inefficiencies in the economy. Japan had been an insulated society which extended to corporate boards (rarely were there foreigners on them). And there was a lack of diversity in their working population. In 2013, only 49% of the women were in the workforce compared to 57% in the US. Abe aimed to change these things for the benefit of longer-term prosperity.

While these things take time (years vs months), it started to work, along with some help from global inflation. For example, women are now 54% of the workforce. Today, the incumbent premier Fumio Kishida wants to focus on wealth distribution among the population more broadly through higher pay. Wages are set to rise there this year (during what they call ‘shunto’), according to a recent Nikkei survey, by 3.9%—the biggest increase in 31 years. And the overall hope is that this will raise sluggish productivity and create a cycle that leads to consumption and growth.

Perhaps this will lead to even cooler fashion trends in Japan? I am semi-obsessed with Fruits mag highlighting Japanese streetwear. Worth a look.

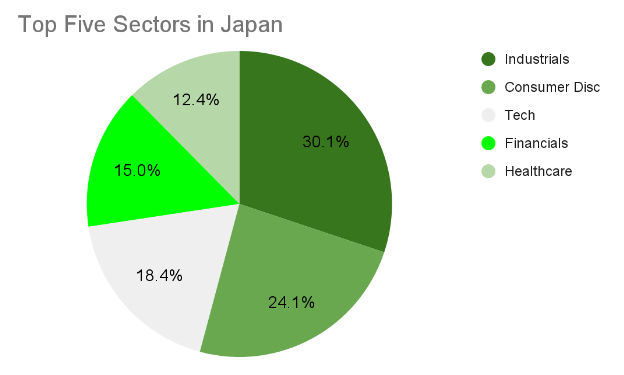

From an investment perspective, I am positive on this region. My expectation of less dollar strength relative to the last decade makes it less of a headwind for a US investor to give up holding dollars for another currency. And the mix of industries is attractive, between car companies, tech, pharma, and industrials.

Now the market may have started to reflect this, but I believe it’s still attractively valued and it only just broke the decades-long top. Of course, like anything there are risks including the ones Abe wanted to mitigate as well as the potential need for the country to raise interest rates in light of inflation, impacting near term valuations like it did in the US last year. The mix of sectors are more “cyclical” in nature so a global recession would impact these and they don’t have any energy companies, making them vulnerable to natural gas and oil prices. However, longer term, I believe there is more upside for the country’s companies.

If nothing else, from Hello Kitty to anime and animal cafes, their culture is one to pay attention to.

Source: Bloomberg, International Labour Organization, Nikkei, US EIA, Robinhood Financial