The importance of sentiment

The importance of sentiment

For a long time, I was a city person. And not just a city person—but also a warm-weather loving, only-beach-vacation kind of city person. The idea of hiking in a forest, being near the mountains, and especially camping, was the furthest from my mind when planning a good time.

But sentiments and ideas change. Experiences (like a global pandemic that makes you better appreciate the outdoors) and the people in your life lead you down paths you never thought you’d be on. Literally. Fast forward to today, and I found myself hiking at the top of a mountain. For a moment, I stopped and took it in. The quiet hum of the alpine forest seemed to listen as much as it spoke.

That same focus is helpful in investing—listening to the hum of the market (aka the shifting of sentiment and data) is as important as talking to others about it. Recall that over time, the three main drivers of stocks are 1) earnings-growth expectations, 2) assumptions about future interest rates, and 3) actual sentiment. Picking up on these three factors, particularly sentiment, requires a keen market ear. Sentiment, or the perception of how good or poorly things are going for a company, market or economy, often seems to shift last—and turn the other way last. Knowing this can help determine entry and exit points of investments.

When I first wrote about this year’s rising stock market, I was admittedly skeptical of this rally (much like I was about hiking). Until recently, it had been driven higher by rising earnings-growth expectations from only 8 stocks in the tech sector (which also accounted for 75% of returns). But it has finally started showing signs of expanding breadth, with other stocks and sectors moving up, making the rally finally feel more healthy. And expectations of falling inflation, which also showed up in last week’s inflation report, further fueled the belief that interest rates would no longer be meaningfully rising for now. This shift in sentiment was a risk I called out then, but now, in my view, it’s got more goods to back it up. All of this has led to a positive vibe in the market, and more investors jumping in.

In my experience, there are 3 phases of sentiment after a bear market like in 2022:

Everyone is skeptical and negative (many call for a recession)

Then some people start noticing a slight positive trend—little green shoots (like the ones on a forest floor in late Spring)

Then the capitulation comes—and many more jump in. Once this happens, sometimes it’s a good time to trim some winners and rebalance.

Where are we today in this continuum?

Well, according to EPFR, investors are now moving into stocks from money market funds. Last week, global equity funds hit a 21-week high for fund inflows (taking in over $22B with US equity funds taking in even more). According to a report from Bank of America, US equity funds—particularly in the tech sector—have seen the strongest stretch of inbound money flow since March 2021. The last couple of weeks have also seen flows in other parts of the US market, such as US value and small-caps. And these equity investments seem to be funded from money-market funds, which saw net outflows for the first time in months.

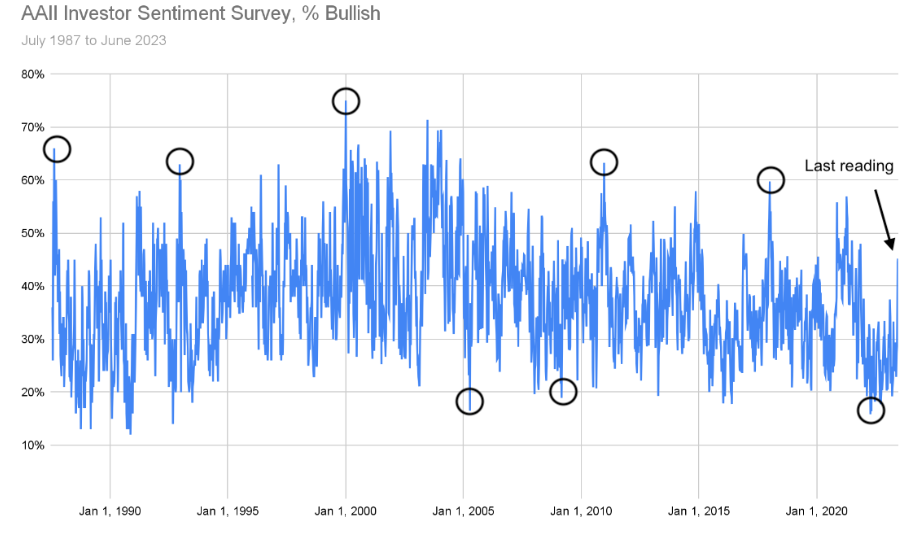

In addition, the American Association of Individual Investors (AAII) aims to measure sentiment through surveys, and it’s showing stronger-than-average-bullish sentiment (recall bulls are positive on the market, bears are negative). Their bullish sentiment reading is at 45.2% as of last week, the highest since November 2021, and above the historical average of 37.5% for a second straight week. Here’s its history, going back to 1987:

A few observations:

The last bottom reading in bullishness (aka bearish time) was September 2022—right before the markets started showing a recovery from the lows of the year.

Many of the peak bullish points, such as in January 2000, December 2010, January 2018, and April 2021, also marked peak near-term values in the stock market, where the next 6-12 months saw negative returns.

When in the extremes, this can often look like a signal to take the opposite direction. Meaning historically, it was better to buy when readings were very low, rather than when they were very high.

This is why measuring sentiment is so important. Because it actually can help you decide if it’s time to trim some winners. The most recent reading, while high, is not at the extremes that served as an ominous potential signal in the past. But, of course, it’s not very low either. From all of this, I think we are in the later part of the middle stage—people are noticing. There are some reasons to start to trim your winners, yet there are still some opportunities to invest. But, as always, it needs to be in light of your specific situation.

For me, given the valuations in the larger-cap tech space are not as attractive as they once were, the marginal equity investment looks more attractive in the value and small cap areas (on a relative basis). This refers to industrials, financials, parts of retail, etc., which are just starting to get some more attention.

Listening to the shifts in the market, and yourself, can lead you down a path you may not have expected to be on, but a good one nonetheless.