Is the recent rally in utility stocks a sign?

Is the recent rally in utility stocks a sign?

Sometimes on a Sunday, I get to relive the angst and emotion of my youth.

As I watched my tween daughter march to her room, shut the door (locking out her little brother), and turn up the music, I fell back into my days of doing the same. Just me and Whitney or U2 or LL. The poetry of the words, jamming with, or over, whatever was on my mind. I could hear my girl singing along to her music and I smiled. These moments could easily pass under the radar, but witnessing them as the tween in me, rather than solely the mom looking at a closed door, I felt, well, lucky.

Lots of things pass under the radar in the markets. It’s easy to focus on the inflation in our face, what DJ Powell said about rates, and this quarter's earnings of the companies we invest in. But it’s the shifts in the details that can help you pick up on trends early, or at least move you to look at things in a different light.

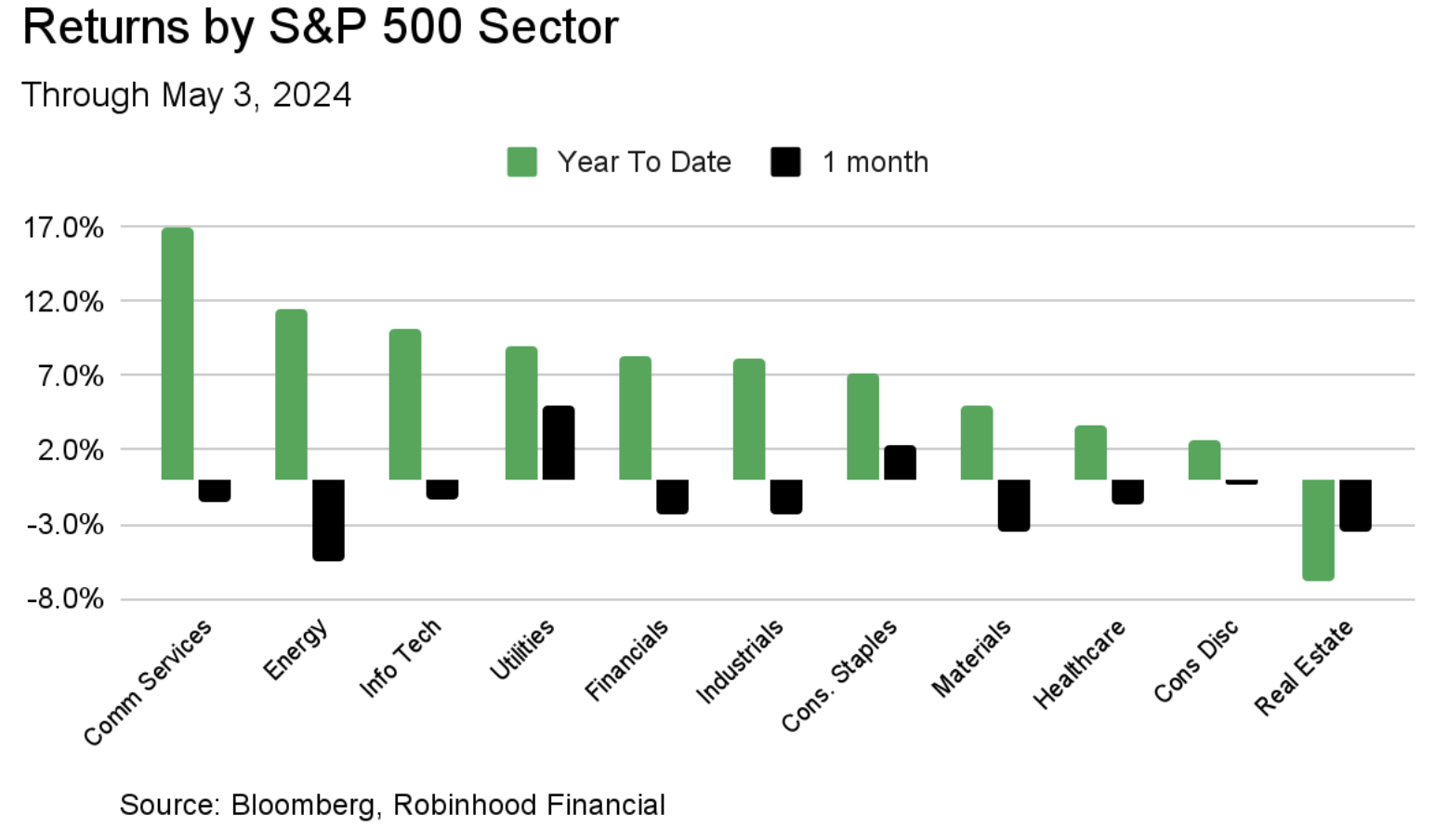

For example, I was looking at sector returns for the S&P and noticed a shift. Take a look at the chart below. In the last one month (in black), defensive sectors such as Utilities and Consumer Staples, started outperforming the rest. That’s quite different to the trend earlier in the year when Communication Services (think social and internet), Energy, and Tech did best (in green).

Given utilities and consumer staples are sectors that tend to do the best in low return environments, is the market starting to plan for a recession or is it just a fleeting shift?

When I looked at this more deeply, I noticed the shift in returns started to happen at the end of February – and was further exacerbated by “disappointing” earnings reports and guidance in some of the bigger names in the highest returning sectors YTD (on the left side of the chart above).

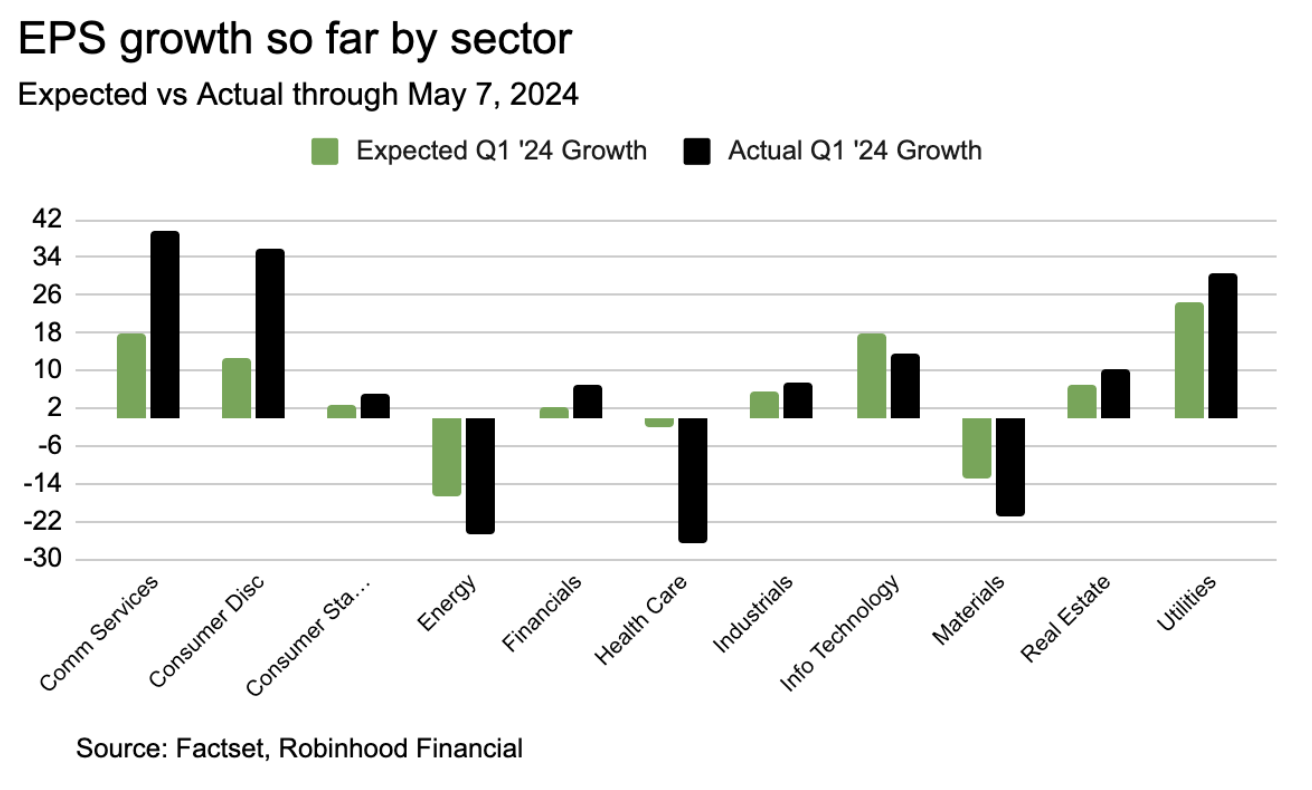

85% of S&P 500 companies have now reported earnings for Q1. When looking at actual vs. expected earnings growth (see chart below), Utilities is in the top three, with only Comm Services and Consumer Discretionary doing better on this measure. So it could be that Utilities ranking well on returns was more about the earnings/guidance disappointments in some tech names vs the strength of utilities alone.

On the other hand, we have had a culmination of data pointing to a slowing economy, which could eventually lead to a headwind for stocks (supporting owning the aforementioned defensive sectors). None of it is slow by any means but certainly not as a strong as it was, including:

April jobs report at 175k vs 235k expected

Manufacturing ISM at 49 (less than 50 so contractionary)

Services PMI at 49 (less than 50 so contractionary)

In addition, commentary from company earnings reports have, in some spots, pointed to a slowing consumer. For example, McDonald's and Starbucks said their customers are increasingly seeking value and scrutinizing their spending while, Sysco, food provider to restaurants around the country, highlighted lower traffic to restaurants. However, Visa and Mastercard both highlighted a healthy consumer, while hotel and cruise line companies noted still strong travel demand. Can you really blame people for applying more scrutiny to where their dollars go? And perhaps it’s not a slow consumer but one that has shifted more permanently to do more things rather than buy more stuff?

So, back to the question, is the economy slowing enough that we should take cover in defensive sectors? I am not personally convinced. A slow down like this still feels in the temporary territory, because nothing goes up in a straight line. While it’s always good to have a balance in a portfolio, I am not raising the alarm—yet.

However, the thing that does worry me, a song I have on repeat, is the US fiscal policy (I discussed this two weeks ago, in October 2023 and more in depth in August 2023). It not only contributes to interest rates staying higher than they would be otherwise (and inflation), keeping stock valuations in check, but also means our deficits are large despite a still healthy economy—leaving little room for when the economy is weaker and stimulus is needed. That is a song I am happy to keep playing—for the youth of today and tomorrow.