Looking back: Mid year review on the markets

Looking back: Mid year review on the markets

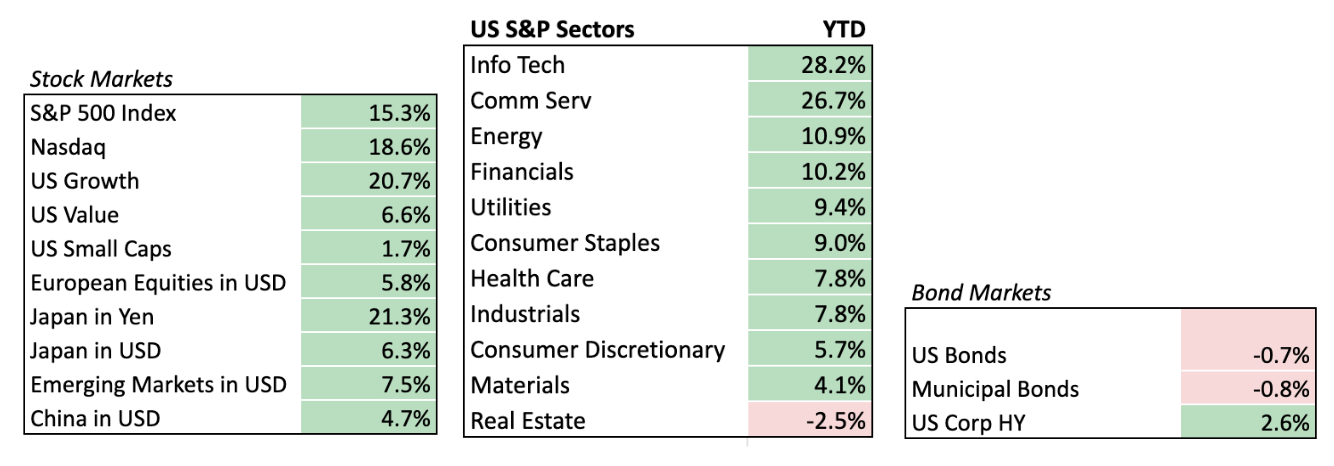

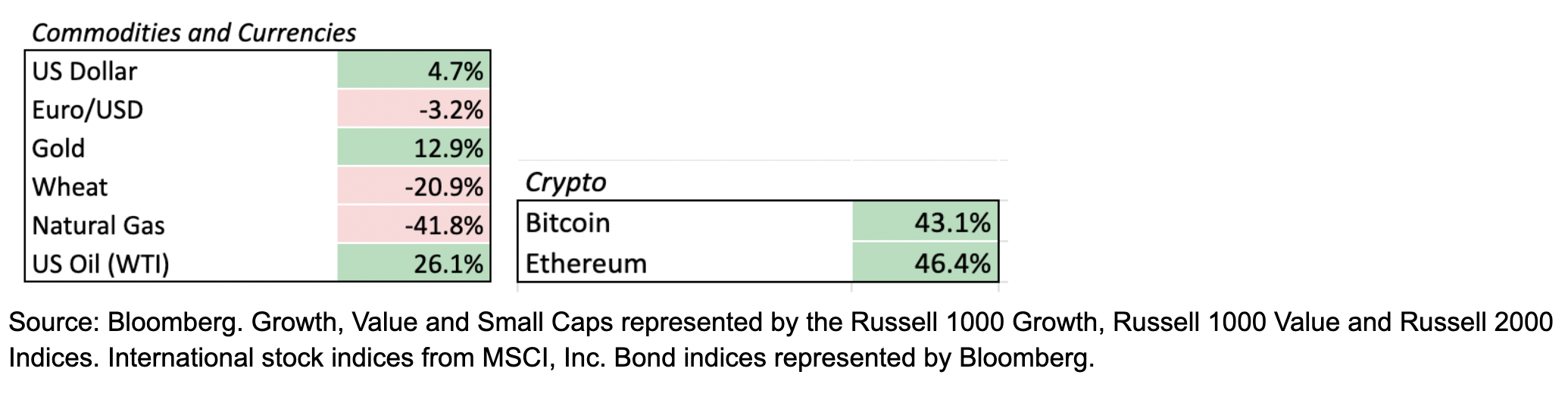

We’re at mid year, so time for a check on markets and the economy so far. These charts show returns from the start of the year through Friday, June 28th. From these, I think it couldn’t be more clear that the markets are not the economy and the economy is not the markets (hi, tech sector!).

What else happened during the year so far?

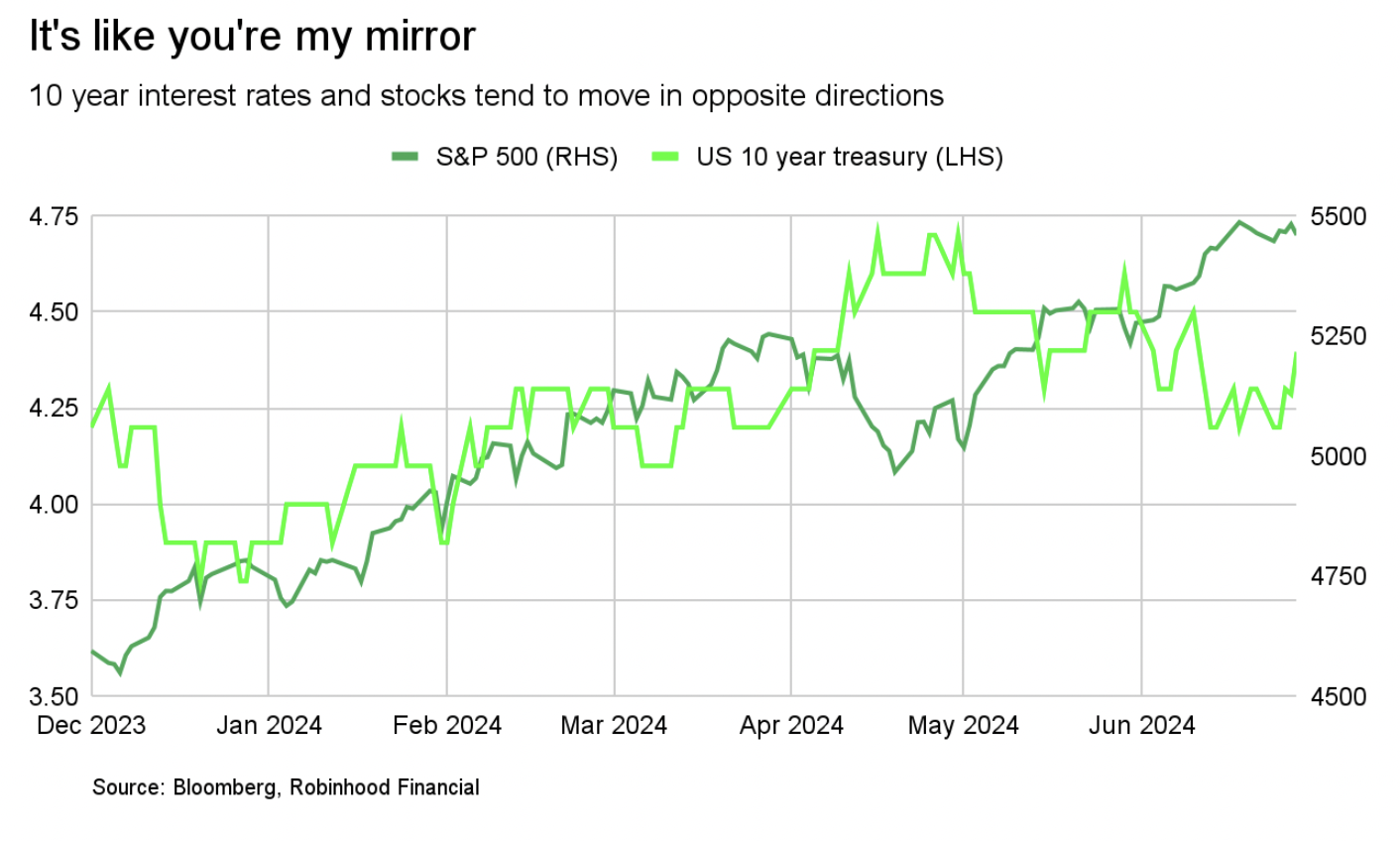

Interest rates went higher and then sideways, but most recently are lower:

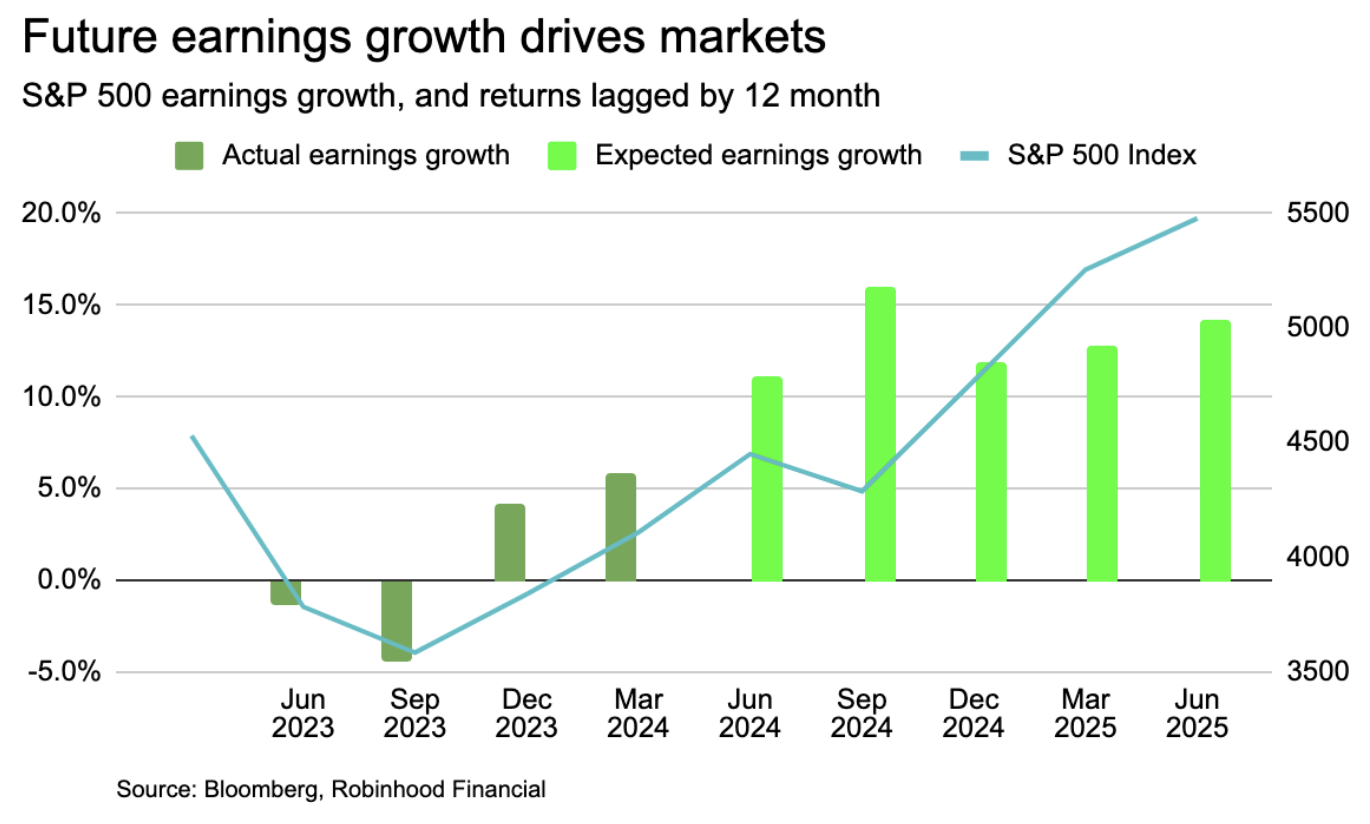

Earnings growth expectations drove markets, but look to be fully discounted in prices now:

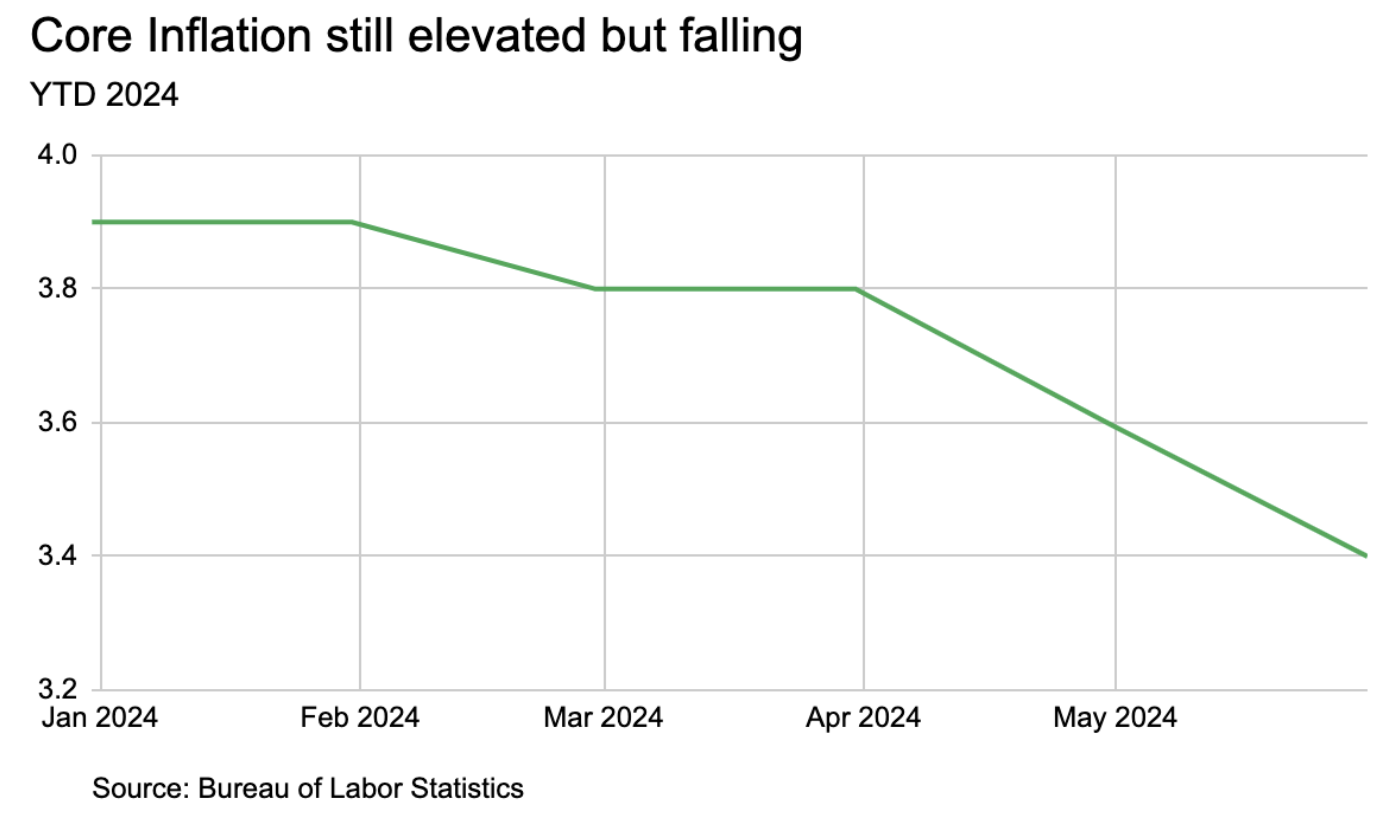

Inflation cooled a bit:

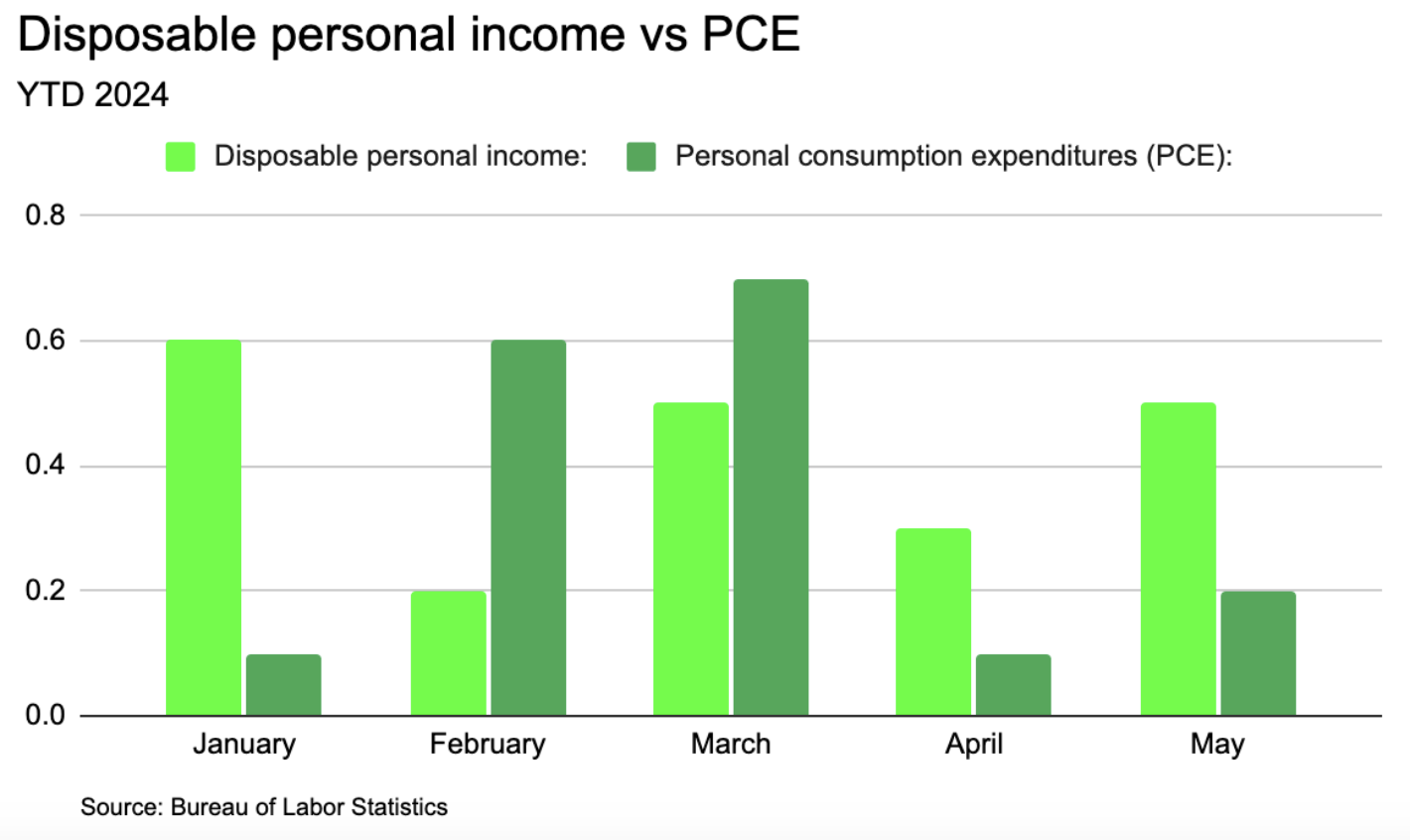

And maybe most interestingly, for two months in a row now, wage growth was broadly higher than the growth in the cost of things (price consumption expenditures, aka PCE).

Because everything still feels expensive, it may not feel like it day to day, but there is evidence of a soft landing. Of course, ongoing risks include growing conflict around the world and our growing deficit.

And, on that note, the most recent Congressional Budget Office’s (CBO) update should be required summer reading on the financials of the US.

We’ll look ahead next week. Happy 4th!