The poor performers in a bull market

The poor performers in a bull market

There are times in life you think you are busy – work, school, caring for family. It can add up. But then something comes along – like a special project at work or an unforeseen major responsibility at home – that makes that old stuff look easy. You adapt, cut out unnecessary things, and occasionally think “hmm I should have enjoyed that slower lifestyle more”.

Some CEOs (or ex-CEOs in some cases), may be thinking the same. From 2009 to 2021, inflation was in check while interest rates were the lowest they had been in modern history. That low cost of debt facilitated things like stock buybacks and investing in projects that easily added to shareholder value, even if they didn’t have the highest returns. As long as the returns were higher than the historically very low interest rates, value could be created for a company.

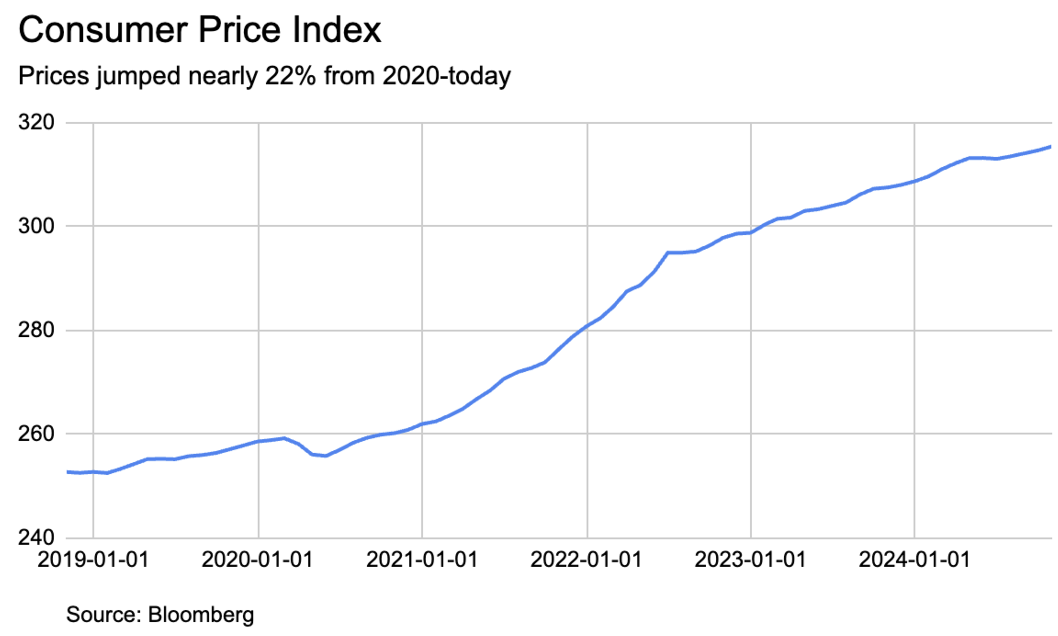

But since then, inflation has driven up the cost of everything. Sales have been more discrete, while higher interest rates have made running a business more expensive. When prices rise, we as consumers get more selective about where we spend our money. Even though inflation has slowed (see chart), consumers remain focused on the absolute cost of goods.

In tandem, higher inflation leads to higher interest rates, and a higher cost of debt. So, for a CEO, finding projects to invest in that beat the higher cost of capital becomes harder, while the incentives to use debt for buybacks is diminished. As a result, they can find themselves in a more difficult spot—threading a needle of enticing value oriented shoppers in their segment, while navigating a challenging consumer and interest rate backdrop. This is especially true in the retail sector.

In fact, retail companies tend to take on more debt on average. Those in the Russell 3000 Index (the largest 3,000 US companies) have a debt to equity ratio of 162 vs. the average for all the companies in that index at 124.

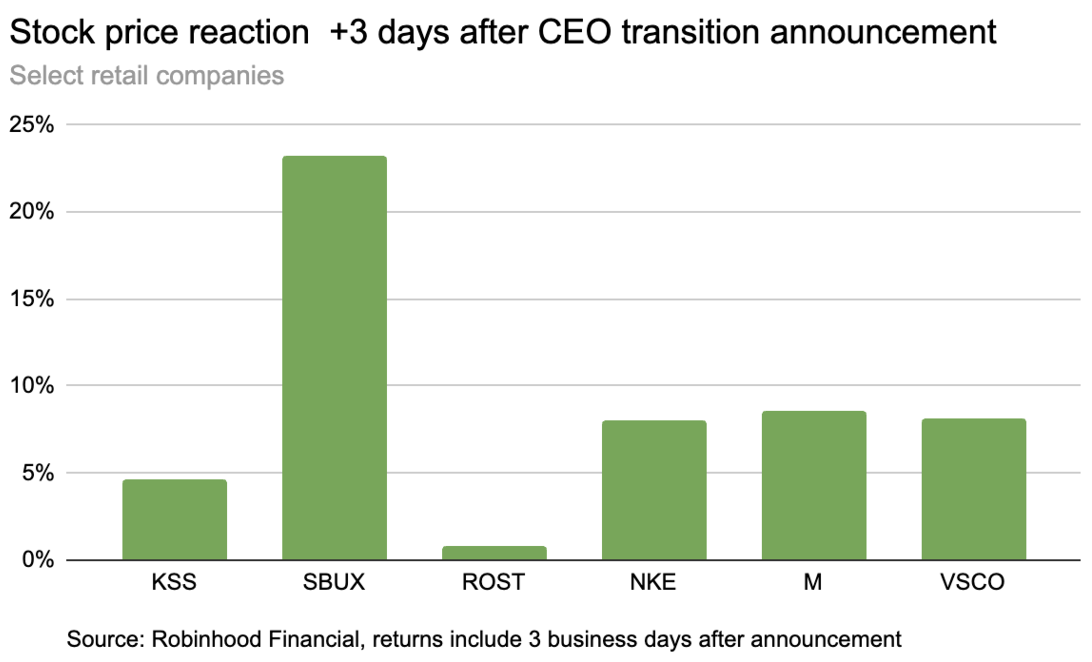

So it may be no surprise that this year alone, we’ve seen CEO changes at some of the biggest names in US retail: Kohl’s, Starbucks, Ross Stores, Nike, Macy’s and Victoria Secret’s, to name a few. This has also started to spread into other industries—to companies like Intel and Stellantis, just in the past week.

In fact, according to Challenger Gray & Christmas, an executive placement and coaching firm, 1,824 CEOs have announced their departure in 2024, the highest year-to-date total on record, since they began tracking this in 2002. It is up 19% from last year, which was the previous record.

With the market up strongly the last two years, company boards are more likely to notice when their company is not seeing the same strength in their stock price. The Conference Board’s recent report, “CEO Succession Practices in the Russell 3000 and S&P 500” shows nearly half (45%) of Russell 3000 companies that changed CEOs had a stock return in the bottom 25% of returns — this was only 29% in 2017.

The market usually initially reacts positively to a change at the top—but then the hard part comes in to actually turn the business around.

So the question is then, who’s next? And more importantly, is leadership change enough to turn things around?

To answer the first question, we looked at the bottom 25% of companies by returns in the Russell 1,000. There are about 280 that have a negative return over the last nearly 2 years (since 12/31/2022) and 300 in that ranking on a year-to-date basis. Many of them have seen a CEO change already – but not all.

Non-cyclical consumer companies were the most populous in the worst 250 stocks by return this year, making up 37%. Most of these were healthcare or healthcare-related companies. This makes sense considering healthcare is lagging behind broad based indices by 20% this year.

Retail stocks were the 2nd most populated in this worst stock return group, making up 15% – many of these have CEO transitions completed or in process. However, there are still some out there such as Hanesbrands and Conagra that have not.

To the point on whether leadership change is enough takes time to know. They must tackle the difficult task of growing sales—vs. just cutting costs (which is usually the first step). This requires understanding what customers want and offering it in a way that stands out from the competition. Common strategies include partnerships with brands, launching new products, or entering untapped markets.

Take Starbucks, for example. Its new CEO, Brian Niccol, has ambitious plans to refresh the company’s offerings. These include bringing back the condiment bar, reintroducing ceramic mugs, and adding more comfortable seating in cafes. He’s also focused on simplifying pricing, streamlining the menu, and boosting staffing hours during peak times. We will eventually learn if it works.

Target, on the other hand, serves as a prime example of strategies not working (at least yet) – though their CEO has not changed. Its shares tumbled more than 20% following missteps in managing inventory and product assortment, which resulted in a disappointing quarter last month. One has to wonder how many more “bad” quarters it will take before a leadership change becomes inevitable there.

As we head into a new year, investors will be looking to see if strategic initiatives by new CEOs are successfully driving business. If they do, these are opportunities in a market that is up a lot these last couple of years—while the hard work and busier time by these new CEOs pays off.