Staying curious about the dollar

Staying curious about the dollar

If you think about it for a bit, you can probably recognize it, too. That is, a time when you assumed something was a sure thing — that it would never change — but then it did. And you had to shift your whole perspective. It might be assuming you’d always have a certain job or a certain someone in your life. Inevitably, life teaches all of us there is no promise of today in the future, and, even more, that staying curious can help avoid some “forever” assumptions.

The same thing happens in markets. Market participants and companies can assume certain things won’t change. When they ultimately do, surprises and big moves ensue. An assumption that interest rates would be low forever eventually resulted in bank capital issues once rates went higher, as an example.

So all the recent talk of the US dollar losing its prominence is, in many ways, good. Questioning its status is healthy and means there are fewer assumptions it will function the way it has indefinitely. So, will its dominance, as the world’s reserve currency*, wane to a minority position?

I personally don’t rule it out in the long run. It could at some point, many years from now. Currencies tend to have very long periods of dominance such that when they begin to wane, it happens over a period of time — not suddenly. And they’ve needed an obvious replacement.

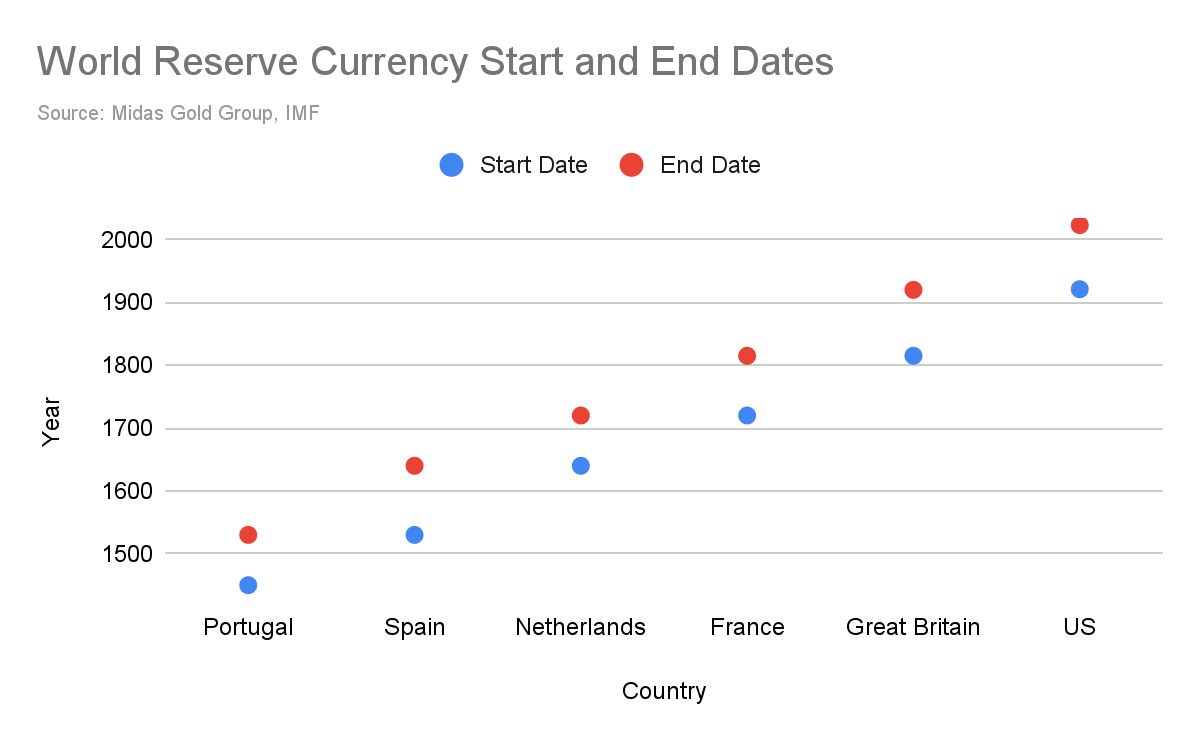

For some context, below is the estimated change in reserve currency status over the last nearly six centuries. Each status lasted between 80-110 years. The US is at 102 years and counting.

To understand the if/when, knowing the history of the US dollar as a reserve currency can be helpful.

First, in the current global financial system, most countries want to hold their reserves in a currency with large and open financial markets so they can access it in a moment of need. Since the US Treasury market remains the largest and most liquid bond market in the world, central banks often hold currency in the form of US Treasuries. In fact, US Treasuries make up close to 60% of global reserves. How did it get to this status?

The dollar’s status as the global reserve currency was cemented in the aftermath of World War II, when the Bretton Woods Agreement established a system of exchange rates whereby each country pegged the value of its currency to the dollar, which was convertible to gold.

However, with the rise of the use of the US dollar, the US did not have enough gold to cover all the dollars in circulation outside the United States by the 1960s. So the dollar’s convertibility to gold was suspended in 1971.

While this initially hurt the value of the dollar, by 1973, the system we have today of mostly floating exchange rates was in place. And importantly, the dollar became the currency of choice for international trade, including important commodities such as oil. Thus, the petrodollar was born.

Of course, the dollar has stayed in its dominant position thanks to its relatively stable value, the sheer size of the US economy, and the United States’ geopolitical influence.

So why has the dialogue of the future of the US dollar (USD) kicked into gear? Well it’s not the first time, and it has a lot to do with a number of factors (some described in a post of mine from October 2022):

The USD has been weakening since Q4 2022. The last time the USD was in major question was around 2011-2012, when it was also weakening. Note: the USD has been in a general upward trajectory since, despite the recent weakness.

What causes a currency like the US dollar to weaken or strengthen? It’s all relative.

Interest rate differentials: This is the difference between central bank policy interest rates, where the country with higher rates will often have a more valuable currency than the one with lower rates, all else being equal.

With the Fed being close to the end of the hiking cycle and others, like Europe, still going, the difference among rates has started to narrow, with non-US rates expected to inch closer to US rates.

Capital flows: This is when investments in a country look attractive such that money (aka capital) starts flowing their way or vice versa. While more money has been flowing to the dollar as a “safe haven” relative to other types of investments, it’s also been flowing to other countries, commodities such as gold, and bitcoin.

Perception of stability and accumulated debt: With the recent banking issues in the US (and Switzerland), the Fed increased its balance sheet, reversing some of the recent progress they made in unwinding years of quantitative easing. This has hurt the perception that the Fed can eventually get back to a place where they do not have to support the US financial system. Looking at the numbers, the balance sheet fell from a peak of $8.95 trillion to $8.3 trillion, only to increase to $8.7 trillion in March. Of note, pre-2008 it was steadily less than $1 trillion.

And another more recent phenomenon that may be playing a role in the discussion: the US has used the size of its economy as a way to manage geopolitical conflict.

The dollar’s centrality to the global financial system in payments not only allows the US to maintain financial sanctions power, but the use of it also ironically threatens the dollar’s status. In seeing sanctions impact targeted countries, others have looked for ways around a US financial sanction when needed. For example, in 2018, several countries created a dollar-free trading system with Iran after the US sanctioned it. And around the same year, and perhaps in advance of an eventual invasion of Ukraine, Russia implemented a strategy to “de-dollarize” the Russian economy and lower its vulnerability to the ongoing threat of US sanctions, opting for a greater use of Euros and Chinese Renminbi.

The US dollar’s reserve status can also hurt the US economy. This is because other countries can engage in currency manipulation — when another country artificially holds down the value of its own currency by accumulating dollar reserves — hurting US exporters in the process. A stronger US dollar makes exports more expensive, and thus, less competitive. This was observed in 2012, and caused the US trade deficit to grow by an estimated $500 billion per year, resulting in millions of US job losses.

So I don’t think the dollar will lose its dominance soon — but rather, this could happen slowly over time, and more likely in a way where the US dollar eventually shares the stage, rather than another currency taking over. After all, many of the floated alternatives have their own problems. And, if it were to happen, it could make US exports more competitive and potentially create jobs, which alone is a reason to stay curious about the possibilities.

Source: International Monetary Fund, Council on Foreign Relations, Bloomberg *A reserve currency is a foreign currency held by countries to manage their economic shocks, pay for imports, service debts, and moderate the value of their own currency. It is essential for countries to hold reserves to ensure a steady supply of imports and assurance for creditors for debt payments in foreign currency.