Debt downgrades: Company debt matters to shareholders too

Debt downgrades: Company debt matters to shareholders too

“A billion here, a billion there, sooner or later it adds up to real money." (Everett Dirksen, US Senator until 1969)

This is what inevitably happened to JetBlue after they announced their plan on Monday to issue more than $3 billion in debt (including $400 million of convertible notes), the majority of which is net new for the company. Credit agencies and investors were not happy. Two of the three major credit agencies (S&P and Moody’s) downgraded JetBlue’s credit rating after the announcement, and the stock fell over 20% in one day. Debt in and of itself isn't a bad thing, but there is a lesson in here. Let’s use JetBlue as an example.

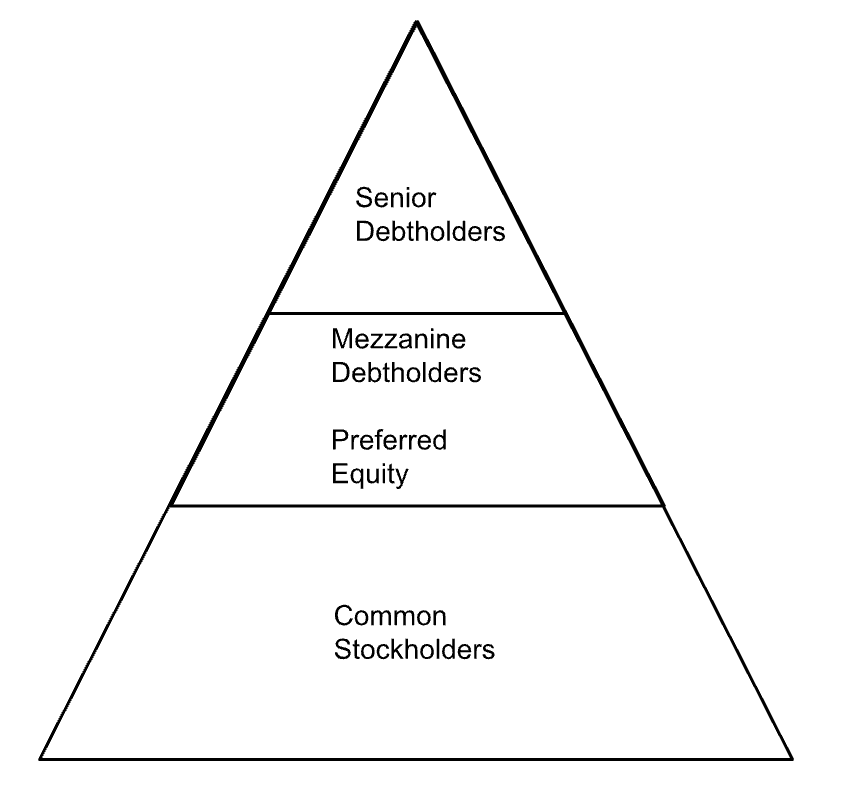

First, the hierarchy of “capital structure.”

For the purposes of a bankruptcy event, every company has a hierarchy for their assets that debt holders and stockholders (who’s in the capital structure) alike could lay claim to:

Within the senior debtholder group, there are those that lent money to a company on a secured basis (secured by existing assets) and also on an unsecured basis. The secured debt has a better chance of being made whole in the event of bankruptcy than more general “unsecured” debt holders because there are specific assets backing up the debt. At the bottom of the list are common stockholders, who get whatever is left which, in many cases, is nothing. As a result, debtholders and credit agencies tend to focus on the company's ability to pay its interest payments and borrowed money back. They care about metrics such as the debt-servicing ratio (EBITDA/interest payments), debt-to-equity ratio, robust free cash flow (the cash flow left after operating and capital expenditures), and overall debt levels. While these metrics are also important to equity investors, they instead tend to focus on earnings growth since this is what they essentially lay claim to (meaning earnings after paying back debt).

In the case of JetBlue, earnings were already under pressure and the new debt suddenly put the company’s ability to pay interest more greatly at risk—aka their cash flow from operations became less than their interest expense. This was enough for agencies to downgrade the “rating.” Downgrades on ratings indicate that creditworthiness has deteriorated, making future debt issuances more expensive. In other words, the interest rates that bondholders will require will be higher and the company overall is less healthy.

Secondly, understanding the different types of debt (aka bonds).

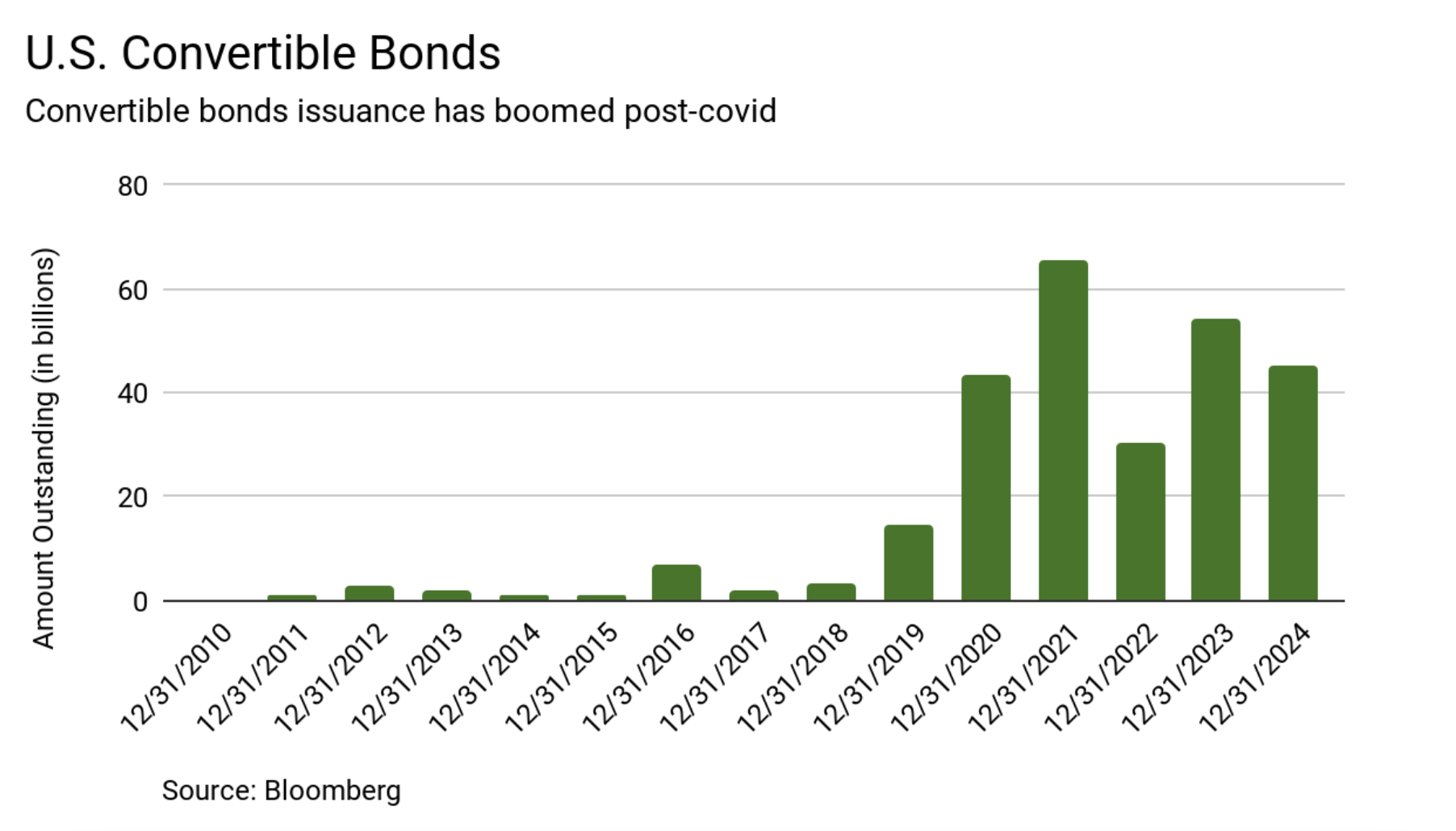

JetBlue also planned to issue two forms of debt: secured debt and convertible debt. As mentioned, secured debt is backed by an asset, much like mortgages are backed by homes. Convertible debt has a unique characteristic in that it can be converted to a specified amount of common stock under certain predetermined terms called "conversion privileges." Convertible debt tends to have lower interest rate payments than traditional secured debt, which is beneficial for the issuer given it carries this option. The promise of lower interest payments has actually sent convertible bond issuance through the roof (see chart), in light of the current higher interest rate environment.

However, convertible debt can also give current equity holders pause. If the bonds were to convert to stocks, there would be a greater supply of stock, diluting shares and potentially reducing the value of the shares in general. And this, along with the general downgrade in the health of the company, drove JetBlue’s share price lower.

In short, the JetBlue case highlights the complexities and risks that come with carrying debt. Issues and triumphs can be a direct reflection of management decisions, health of an industry, and macro trends. The story of JetBlue emphasizes the importance of understanding the balance sheet for each company, whether you’re a bond or stock holder, especially in the event things “get real.”