Mid-year outlook: Too good to be true?

Mid-year outlook: Too good to be true?

Studies have shown we as a species tend to be more focused on risks and bad news, than we do on possible rewards and good news. The news cycle alone exemplifies that. And naturally, we don’t trust things that seem too good to be true, often asking “what’s the catch?”

I believe the same applies to the markets this year. After a YTD 18% run up of the S&P, and a 25% move higher for the NASDAQ, a common question now is “are earnings expectations for the tech sector too high?” and “should I just take my profits and go to cash now?” Quite naturally, investors are weary of the possibility for markets to keep going.

To help answer these understandably skeptical questions, here’s our mid-year outlook for the 2nd half of 2024 and beyond.

Overall, the market is grappling with two opposing forces:

Traditional economic concerns: The future of interest rates and Inflation → the consumer and growth → the job market

A tech supercycle, driving growth for a handful of companies with potential for greater increases in broad productivity—but also sparking questions on valuations and heightened expectations.

Let’s start with the macro stuff first.

Inflation and interest rates

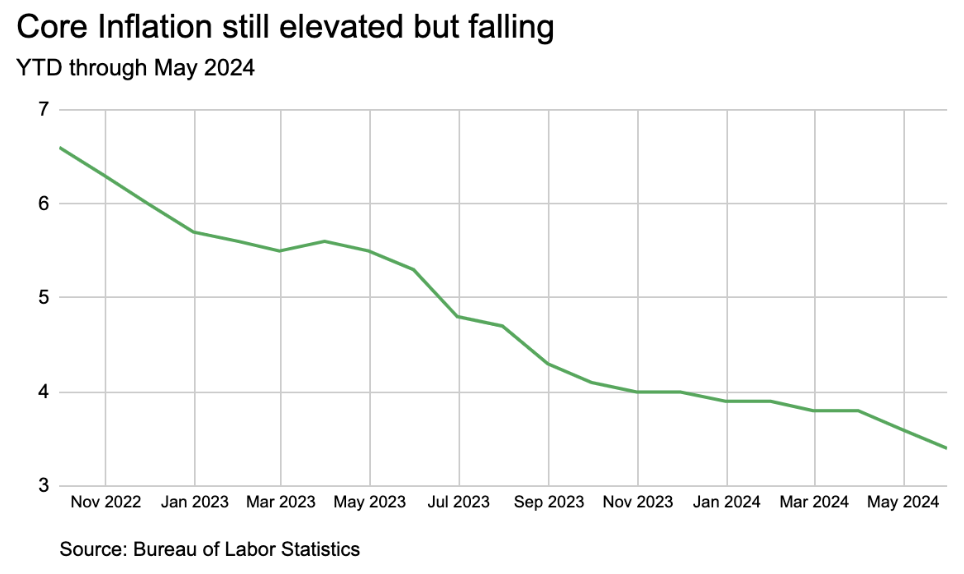

Inflation has fallen from a peak of 9% in 2023 to 3.3% on headline and 3.4% on core (ex food and energy prices). I believe inflation will continue to soften from here, reaching a sub-3% by end of year. That is progress, albeit slow.

The gradual nature, I believe, is because there is still a ton of stimulus out there—especially fiscal stimulus—that keeps the trajectory slow. Also because of this, I expect the 10-year treasury yield (which forms the base for stock valuations and mortgage rates) to stay more elevated, in the 4-5% range, even when the Fed cuts their rates, as it competes with a growing US deficit.

When it comes to inflation, we as consumers are over the cost of things and have become, by necessity or choice, more discerning on spending. This, in turn, is leading companies to listen, offering discounts and better value to improve sales. And last week’s jobs report showed unemployment slightly higher than expected, while continuing unemployment claims have also started to creep higher.

These actions should help continue to slow the economy and inflation on its falling path. I expect this week’s CPI report (Thursday) to be a touch lower than current expectations of 0.1% increase MoM and 3.1% YoY.

With inflation lower and signs that consumer spending is slowing, the Fed seems to be a step closer to beginning their own interest rate cutting cycle (like Canada and Europe have already kicked off). Note, the ending rate of the cycle won’t be close to what it was in the post GFC/COVID era. I believe R* , the natural rate of interest excluding inflation, is higher now—I see it at around 2%. I expect the first cut to be in November or December and continue to around a 4% rate by the end of 2025, from 5.25-5.5% today.

The US being a consumer economy, the key to how much it slows and inflation comes down is the job market. It is softer but still showing general strength. Recently I’ve noticed job growth is not keeping up with population growth, which has ticked unemployment higher (to 4.1%). If we get closer to 4.5% unemployment, growth concerns will outweigh inflation and the Fed will need to cut rates further.

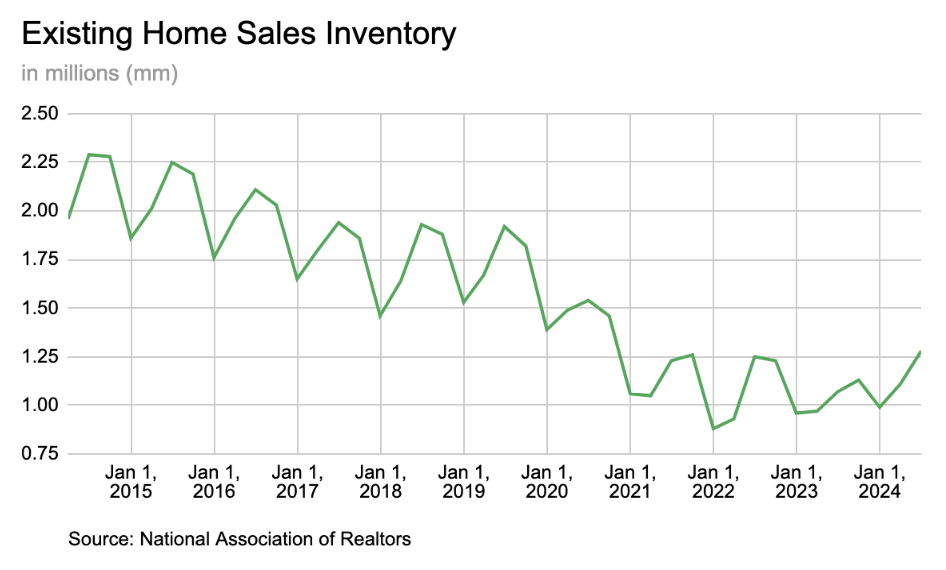

On a positive note, when the Fed does finally begin to cut rates, I believe this could actually help lower inflation further. That’s because lower rates could help lower mortgage rates some, igniting more existing home sales inventory, increasing the number of sales, lowering rental demand and thus, the cost to rent.

On to markets

Here’s where it gets interesting.

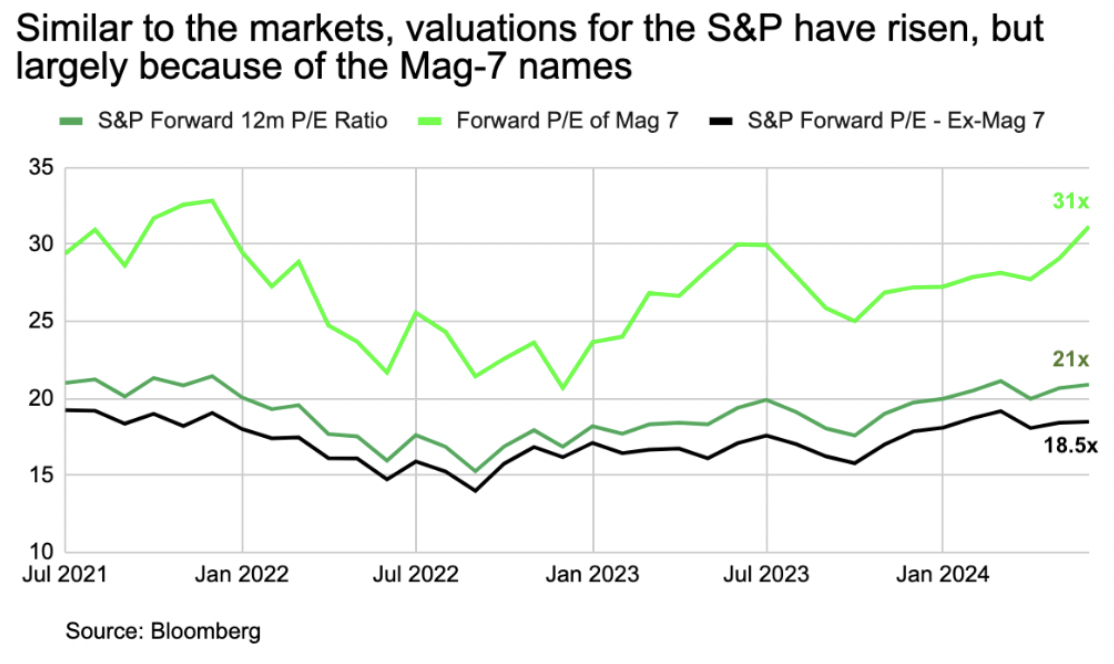

S&P 12-month forward valuations are elevated, which is driven by most of the names in the “magnificent 7.” Meaning that valuations excluding those 7 are reasonable.

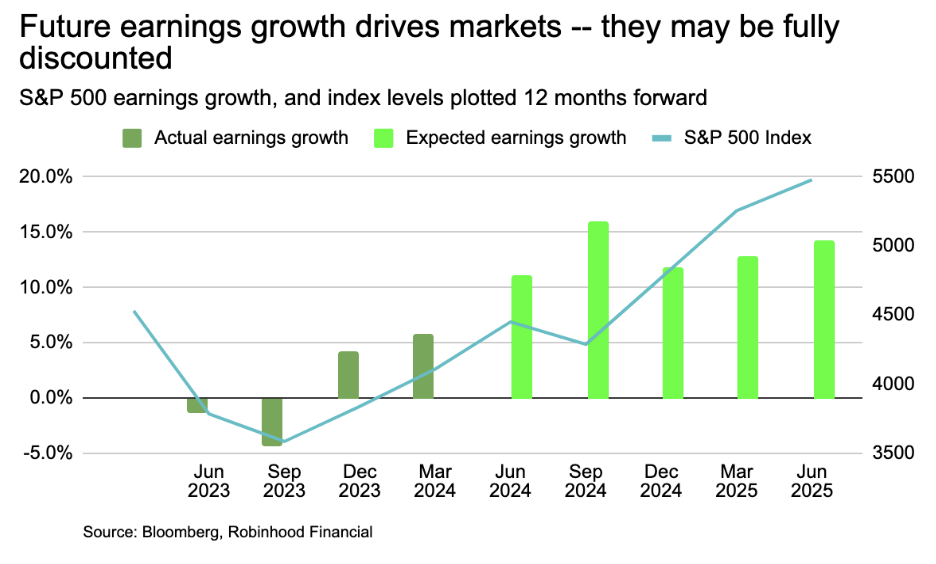

The thing about these measures is they are based on the average expectation of future earnings for each company. So built into these numbers is an aggregate opinion from across the Street about what earnings growth could be achieved over the next 12 months. If earnings growth ends up being greater than expected, it means these valuation numbers are actually lower than estimated and vice versa. Questions around valuations being high, are really a question of whether future earnings expectations are too high.

So let‘s look at consensus earnings expectations for companies in the S&P 500:

For Q2 2024, S&P 500 earnings growth is expected to be ~9% YoY. That would be the best quarter since early 2022, which could be a high bar.

Top 10 stocks are expected to provide 16% earnings growth YoY, driven by those in the Communications Services and Tech sector earnings growth, which are each expected to grow at ~18.5% and ~16%, respectively. By the way, the remaining 490 are expected to earn less than 2%.

For the full calendar year of 2024, earnings growth is expected to be 11% for the S&P. With a long-term average, annual earnings growth rate of 6%, it’s a historically higher bar. I’m skeptical, even with the top 10 in the S&P 500 bringing up the average (16% earnings growth expected), my skepticism lies in the remaining 490 stocks providing a growth rate of 7%. This is because, for the last 5 quarters in a row, the earnings growth rate for these stocks has been much lower, if not negative.

Looking ahead to 2025 earnings growth expectations, they are around 14.5%. I’m concerned that for the near term, prices could fully reflect this.

If it wasn’t for the concentration of the big 10 being around 37% of the S&P 500 index, I’d say the expected earnings growth rate would be nearly impossible.

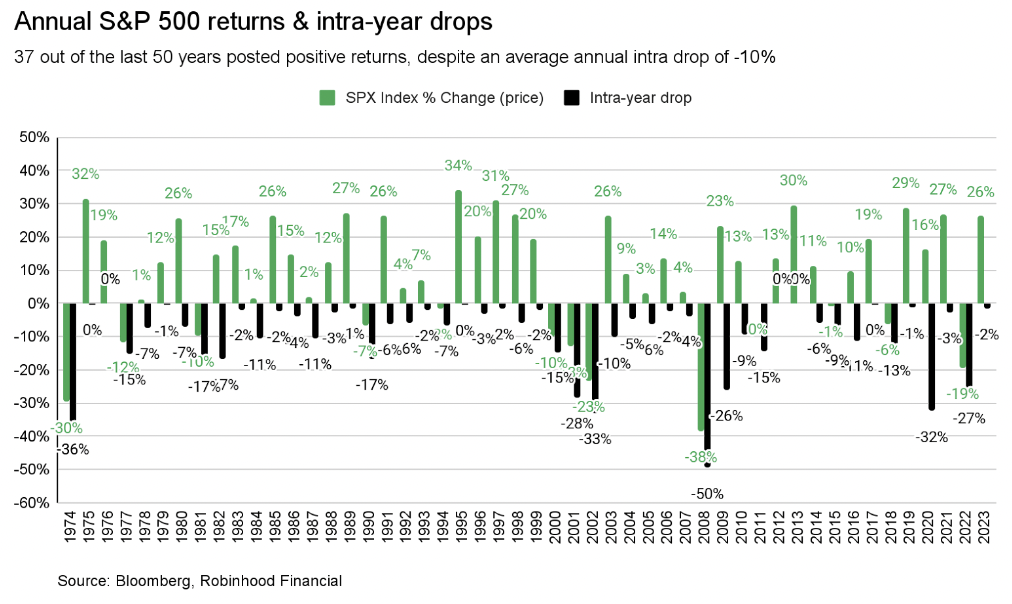

Given all of this, I expect markets to experience a correction, perhaps sometime around September, which has historically been the toughest market month. A 10% correction is quite normal. So I wouldn’t be surprised if the S&P falls to around 5,100, before bouncing up to end the year higher at around 5,800-5,900. After all, volatility is quite normal:

One risk to this view is the tech super-cycle itself. Earnings growth expectations are difficult to truly and accurately predict in this space. So it’s possible they end up being much higher for companies benefiting from the evolution of AI, bringing the year end S&P even higher to 6,100. I place a 20% probability on this. It also could mean the earnings growth we’ve seen doesn’t last, slowing the pace of growth, and seeing muted returns for a while instead. I place a 10% probability on this.

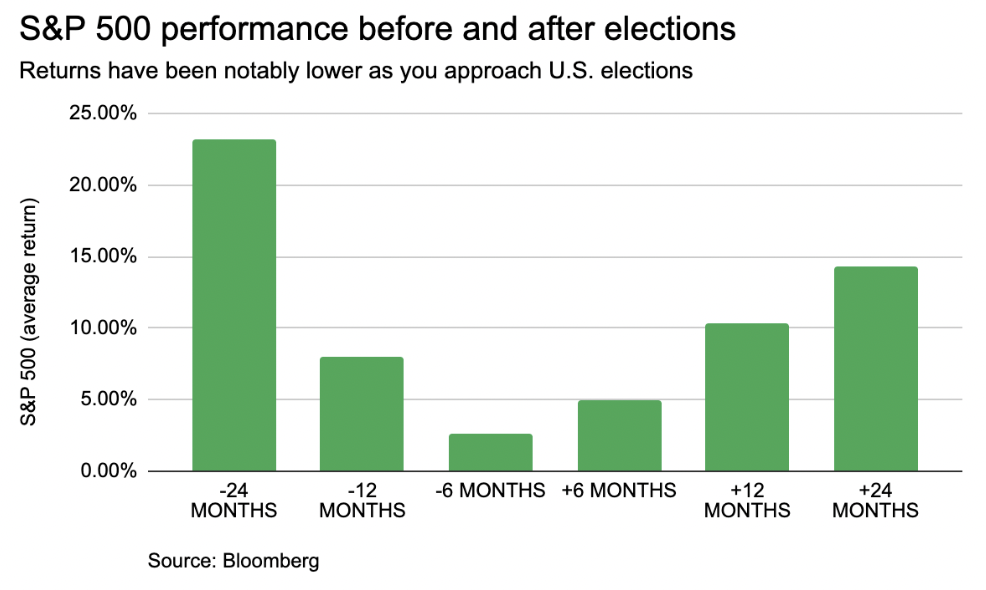

Finally, no mid-year outlook in an election year would be complete without taking a look at how it can affect volatility. Looking at S&P 500 returns before and after elections, we found returns to be lower on average heading into the election, moving higher at a greater rate after it’s decided. This further supports my view that we could see a near term market correction.

Only time will tell what actually transpires in the next 6 months.