The world’s turned upside down (and an earnings update)

The world’s turned upside down (and an earnings update)

It’s only January 18th and yet so much has been happening. Planes breaking mid-flight, public battles between hedge fund managers and elite universities, unprecedented budget debates in Congress, increased conflict in multiple parts of the Middle East, and a big difference of opinion between the markets and the Fed about the future of interest rates.

Uncertainty abounds. And while nothing is ever certain, it feels exaggerated now. Should it matter for a portfolio?

Well, in the short term, yes. Longer term, if history is a guide, it’s less likely. Take a look at some of the charts below.

Volatility is actually pretty normal. As you can see from the chart below, the market has been up 37 of the last 50 calendar years, even though the average annual intra-year decline is –10%.

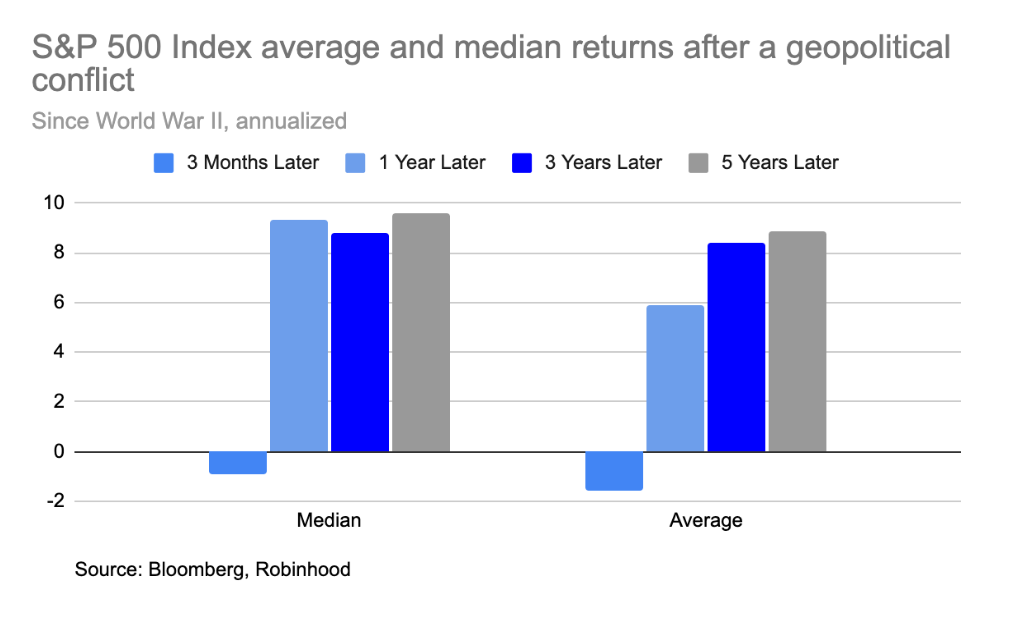

While the human toll and range of consequences from a geopolitical conflict is not something to ever discard, longer term returns after geopolitical conflicts have historically not been impacted:

This is because earnings and profit have mattered most in stock prices over time. You can see in the chart below how annual earnings growth has historically moved with markets.

So taking a long-term view on long-term investments and managing your emotions is tough but it can be the right call.

And since we are in the middle of earnings season, a word on it. So far, earnings season has been disappointing. Earnings, revenue, and forward-looking guidance have generally fallen short in some or all the ways. This supports my view that expectations for future earnings are too high. The market is still expecting close to a 12% increase in earnings for the S&P this year. I would estimate it should be close to half that. But it’s early in the season—only about 7% of S&P 500 companies have actually reported. And it’s been mostly from financial services companies. So more to come.