Why are small caps so grumpy lately?

Why are small caps so grumpy lately?

My parents had a very grumpy cat. It loved sitting in a specific spot in our house and if you walked in (unless you were a specific person), it would hiss at you. The year end market, with the exception of a few stocks, felt the same. No love from Santa as the holiday season ended—and the market was particularly “hissy” towards small-cap equities. As measured by the Russell 2000, they nosedived last month, falling 8.3%. The natural question is, what happened? TLDR: interest rates went up. But to fully understand the story, let’s take a step back.

Last year, thanks to easing inflation, the Federal Reserve cut rates by 1%, lowering the Fed Funds rate from 5.5% to 4.5%. And nothing gets small caps going more than a rate cut. Why? Let’s break it down:

Reliance on Floating-Rate Debt: Roughly 30% of the debt held by companies in the Russell 2000 is floating-rate debt, compared to just over 3% in the S&P 500. Lower rates reduce borrowing costs for these smaller firms more quickly.

Longer-Duration Focus: Roughly 1/3rd of Russell 2000 index stocks are actually unprofitable (meaning they make less than they spend), which means positive cash flows are expected further in the future, making them more sensitive to changes in long-term interest rates.

Capital-Intensive Businesses: Many small caps operate in capital-heavy sectors, like manufacturing, where borrowing and, thus, the cost of capital plays a critical role. These firms perform well during economic upswings but can struggle during downturns due to their cyclicality. The higher the opportunity cost of investing, the more these firms are impacted by long-term rate changes.

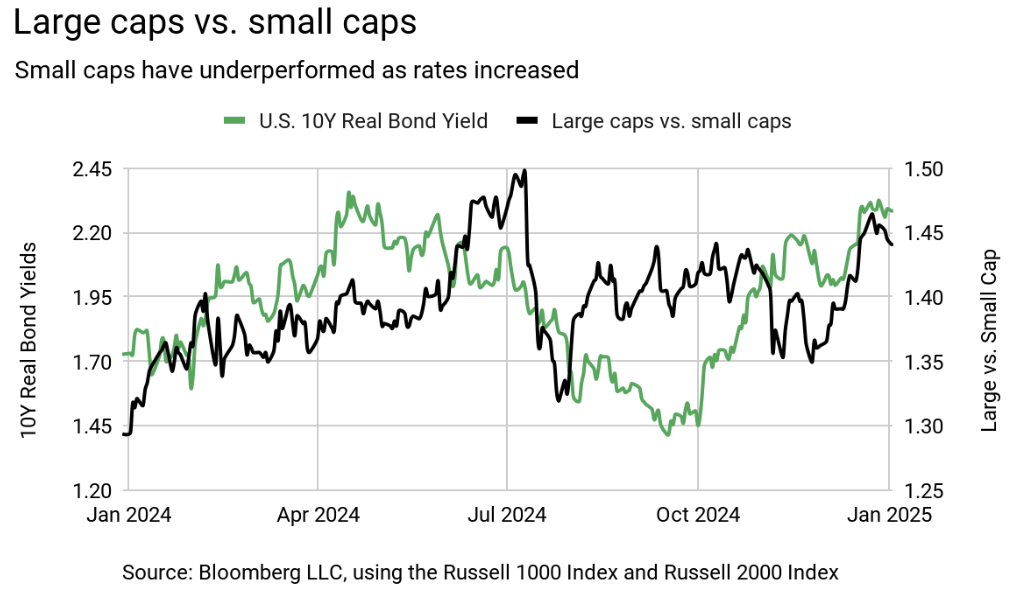

But then interest rate reality set in Despite the Fed’s rate cuts, and different to nearly all Fed rate cut cycles before, long-term real interest rates moved higher (especially in the last month)—a nightmare for small-cap performance (see chart).

Initially, real rates, which is the 10-year treasury yield minus inflation, climbed due to slowing inflation. But the December FOMC meeting revealed a shift: economic growth is expected to be firmer than anticipated, along with inflation. Typically a stronger economy means rising earnings expectations for smaller companies. However, the headline raised concerns that stronger growth could reignite core inflation, reducing the likelihood of further Fed rate cuts. Markets quickly repriced small caps to reflect these dynamics.

With long-term rates still on the rise, it might seem like small caps are facing an uphill battle. But that would mean there are no positive offsets to the story.

It may not be over for small caps

Economic growth is gaining momentum, which is a positive for small caps. The manufacturing PMI improved for the second straight month in December. Increased orders and production suggest the haze over manufacturing may finally be starting to lift. Some employment data from yesterday also showed a still solid job market with higher job openings than expected. As confidence in the economy grows, earnings expectations for smaller companies are likely to rise, which should, in turn, support stronger returns.

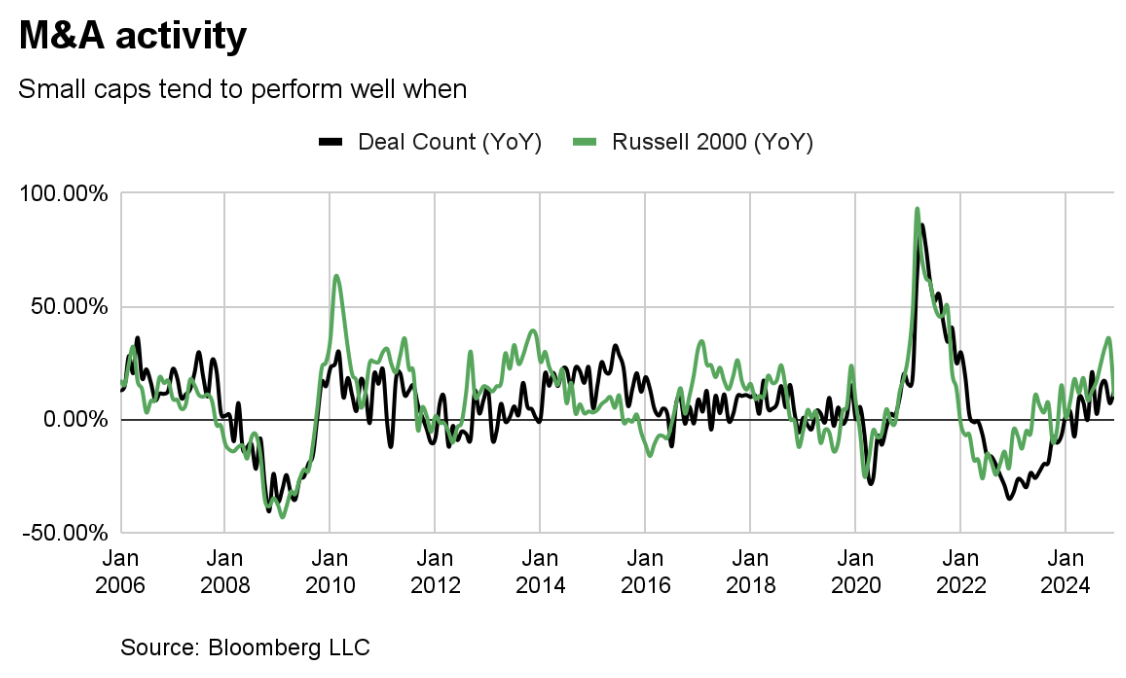

As we highlighted in a recent article, 2025 could be a strong year for mergers and acquisitions (M&A). This trend tends to favor small-cap outperformance, particularly among firms that become acquisition targets. Companies with strong balance sheets and attractive valuations compared to their peers are likely to be in high demand. In this environment, careful stock selection will be critical.

There’s also a political wildcard that could boost small caps more broadly. Many expect the Trump administration to push forward with tax reforms, which could lower costs for firms. However, we don’t anticipate cuts as dramatic as those during Trump’s first term, when the median tax rate for small-cap companies dropped from 35% to 21%. This time, any reductions will likely be more modest, as the administration has to balance rising deficits and increased spending.

Yes, rising long-term rates pose challenges for small caps, but the landscape isn’t all bad. The key for investors will be to look beyond the headlines and focus on small-cap opportunities with strong fundamentals, attractive valuations, and exposure to growth-friendly trends. In other words, be selective as you would be for holiday presents, and maybe pet cats.