What’s a bond vigilante?

What’s a bond vigilante?

When I hear the term vigilante, which has been making the rounds in some financial news, I immediately think of an old-timey image of a guy in a black and white striped shirt, a pirate-like mask, and a black beanie. But that’s not quite right because the intention of a vigilante is more noble than that image. The Mirriam-Webster dictionary defines a vigilante as “a member of a volunteer committee organized to suppress and punish crime summarily (as when the processes of law are viewed as inadequate).”

Bond vigilantes were so named in the 1980s, when inflation and longer term interest rates (around the 10-year mark and greater) were at a peak, and about to come down. As Edward Yardeni, of Yardeni Research declared at the time, “..if the fiscal and monetary authorities won’t regulate the economy, the bond investors will. The economy will be run by vigilantes in the credit markets.”

Of course, bond investors are not really vigilantes. I’ve worked with many of them in my career and, while they may be good people, they don’t act with an explicit intention of regulating the economy in mind. They, instead, work within the confines of perceived risk. They collectively demand an interest rate that will cover their perception of risk—the amount of future issuance the government will need to do and the possibility of future inflation.

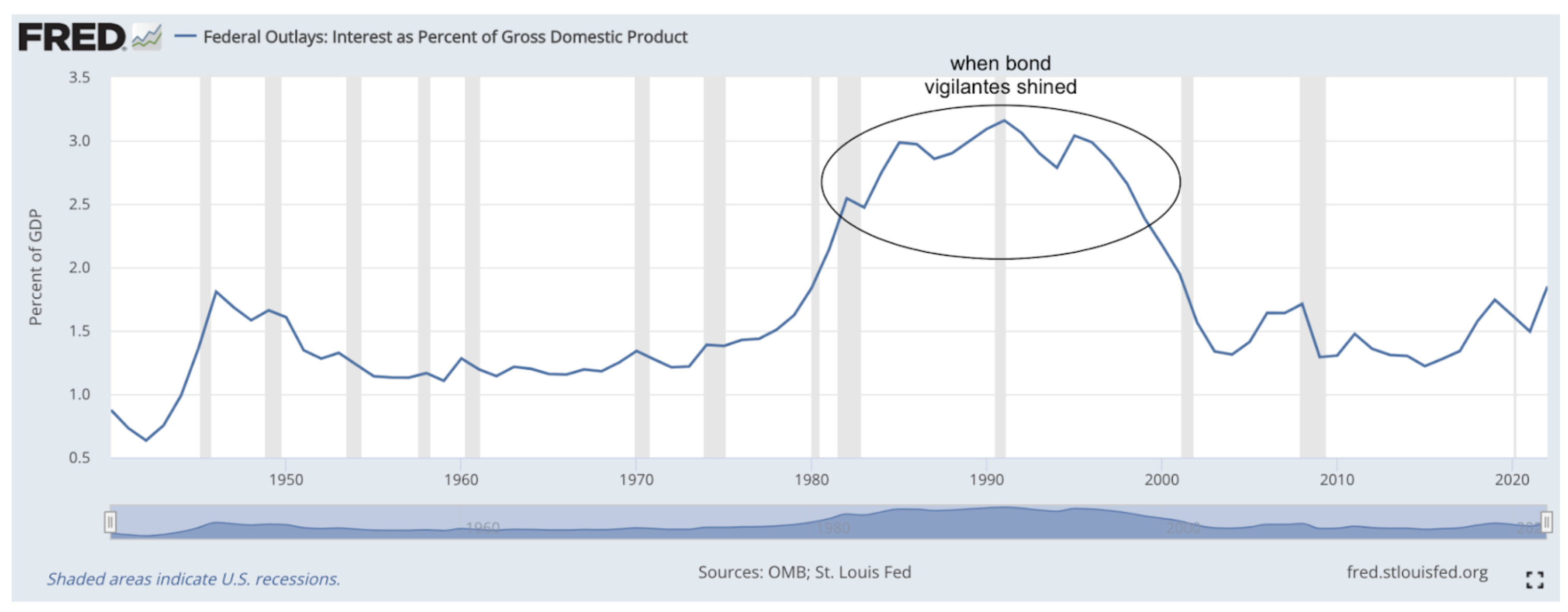

The chart below shows interest payments, as a percentage of Gross Domestic Product (GDP), the US government has paid since 1940—essentially showing how much in interest it pays on its debt. The 1981 to 2001 period shows when the bond vigilantes were most vocal, and interest payments relative to GDP were their highest.

Today, fiscal (aka US government) deficits are high. Interest rates are elevated relative to the last 15+ years. Things may not be exactly the same as the past, but they look like they are starting to rhyme. Thus, many have declared the bond vigilantes are back. Are they?

Let’s break this down a bit further.

Essentially, due to a myriad of decisions and global crises, the US government has increased its deficit, without making much more money. Total public debt as a percentage of GDP (what we produce as a country) is around 120%—-the highest level since at least 1965 (for details on the deficit, see my post on the topic from August). This means that unless they cut spending, or make more money (usually through higher taxes), the deficit will continue to exist, and even grow.

In addition, the Federal Reserve has taken two sets of actions that has led to interest rates being higher anyway: 1) increased the Fed Funds rate by over 5.25% (to reduce inflation) and 2) started reducing the amount of US debt they initially bought during the Covid period by $95 billion per month.

Putting this together, it means the US government’s debt potentially should cost more, since interest rates are higher in general, the government has to keep issuing more of it, and they have one less natural buyer of it. The same way inventory goes on sale when a store has too much of it, bond vigilantes may step in and say, 'if you want us to buy this, it has to be a good enough deal.’ And, as I have explained before, higher rates can also mean lower stock valuations, on average.

So, are the vigilantes back? I think they’re sniffing around but not in full force yet. We’ve seen the 10-year treasury yield rise above the 4.5% mark—a level that has caught attention since its shift out of the recent range of 3.5-4.5%. This has happened especially in response to Congress not being able to pass their budget and the realization that the US may be funding several conflicts now.

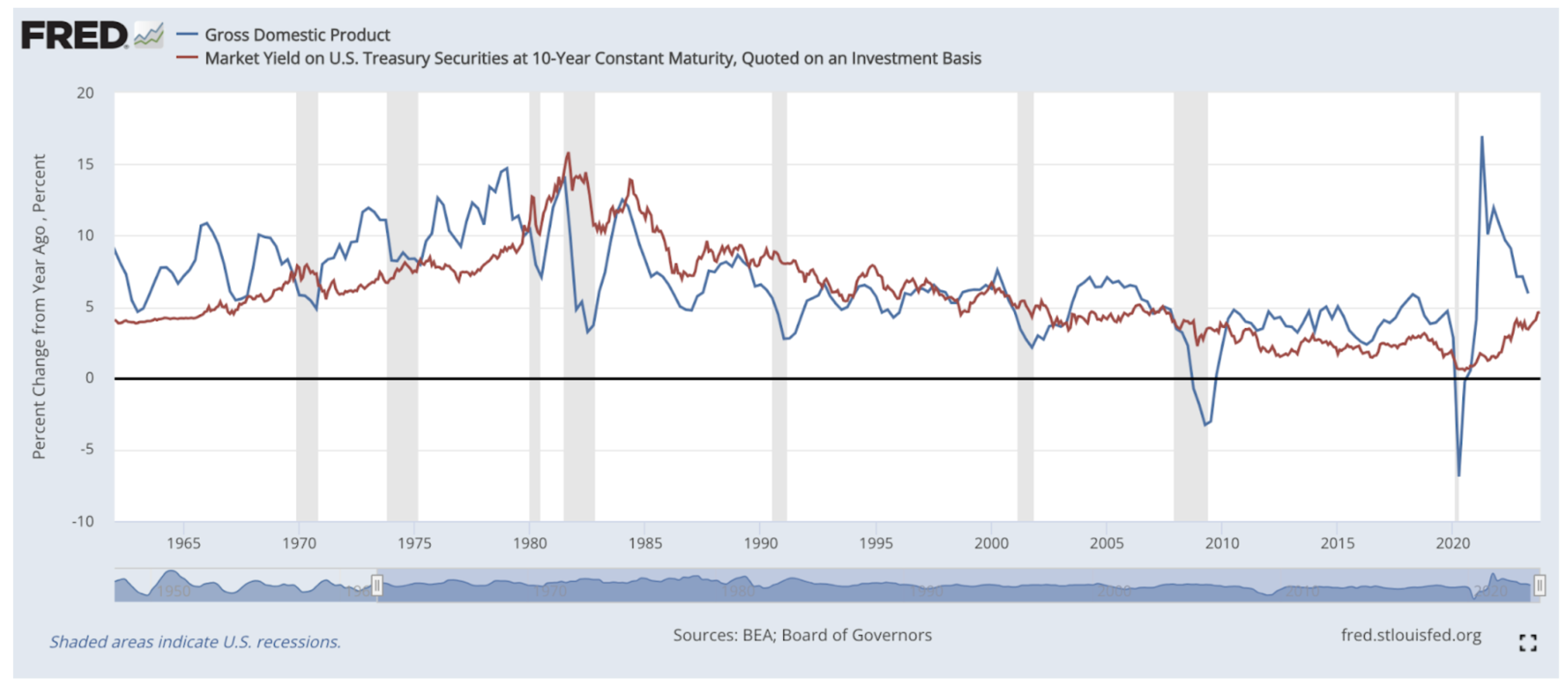

The chart below shows the vigilante voices could grow louder. When bond vigilantes were last prevalent, the red line (the 10-year treasury yield) was generally above the blue line (GDP). Then for most of the last two decades, that switched.

In the most recent period, the two lines on the right have some more traveling to do before they touch and cross to “vigilante status.” Perhaps they never do, but I’m not sure I would bet on that—or at least not yet.

Sources:

1st chart: U.S. Office of Management and Budget and Federal Reserve Bank of St. Louis, Federal Outlays: Interest as Percent of Gross Domestic Product [FYOIGDA188S], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/FYOIGDA188S, October 16, 2023.

2nd chart: U.S. Bureau of Economic Analysis, Gross Domestic Product [GDP], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/GDP, October 16, 2023.