2025 Outlook: It’s always and never different

2025 Outlook: It’s always and never different

In 1933, John Templeton famously wrote that the words, “this time is different” are “among the four most costly words in the annals of investing.” In writing this outlook, I believe this time is different in certain aspects. In others, respecting history (recent or longer term) may be fruitful.

Let’s dive into my base case.

Starting with the economy:

The economy should continue to exhibit its balancing act as part of its soft landing status and GDP growth. Like the three similar soft landings in history (during the 1960s, 1980s, and 1990s), margin compression will again be generally acceptable in 2025, similar to the last three years, and supportive of a continued strong labor market with good wage growth.

This will allow for an average real GDP of around 3%. In addition, the labor market should be stable in 2025, while maintaining the current and average non-recessionary unemployment level of 4.2%.

Interest rates should stay elevated—and what it means for you:

With higher growth, the progress towards lower inflation will stall out during 2025, from the current headline rate of 2.6%, ending the year at 2.3% (higher than consensus).

As a result, I expect the Fed to continue delivering rate cuts through Q1, to 4%, before pausing. This is slightly higher than the 3.75% year end rate the market is currently pricing.

As a result of these points (good growth with some inflation still around), the 10 year treasury yield should sustain a range of around 4.5%. However, there are risks for levels to be higher at around 5%, due to the deficit issues (I’ll get to those below).

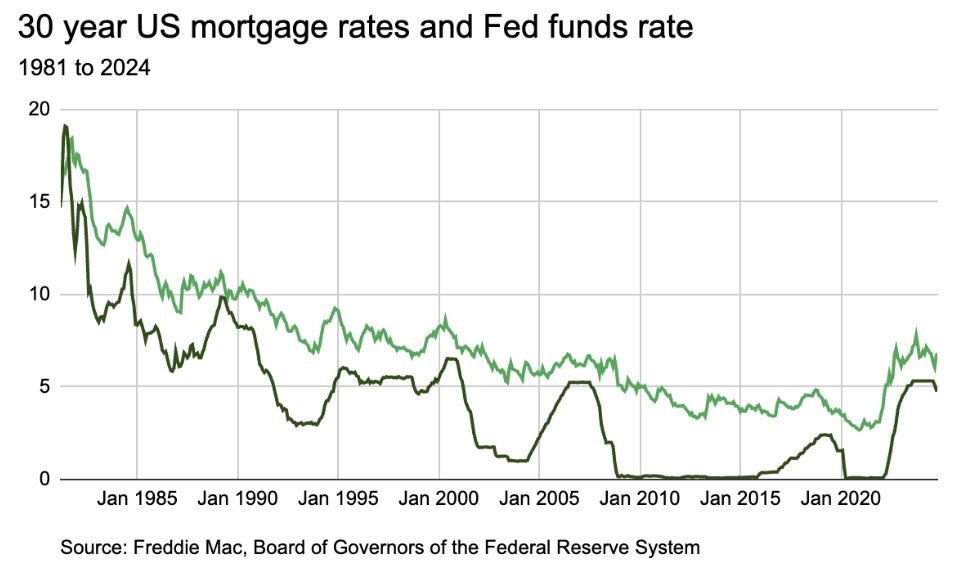

This last point is important because the interest rates on mortgages and consumer loans are based on 10 year treasury rates. If they don’t change much, or even go higher, the interest rates that impact us will not fall, despite the Fed cutting rates. As of this writing, according to Bankrate.com, the average interest rate for a 30-year fixed mortgage is 6.73%. With a lower Fed Funds but a higher 10 year, I would expect mortgage rates to hover around 6% in 2025.

Earnings and stocks to move higher in 2025—but it’s different this time. To start, three things tend to matter for the stock market:

Earnings growth

Sentiment

The direction of interest rates

So with our base case expectation that interest rates will stay within the recent range, this factor should be less impactful, and leaves the other two.

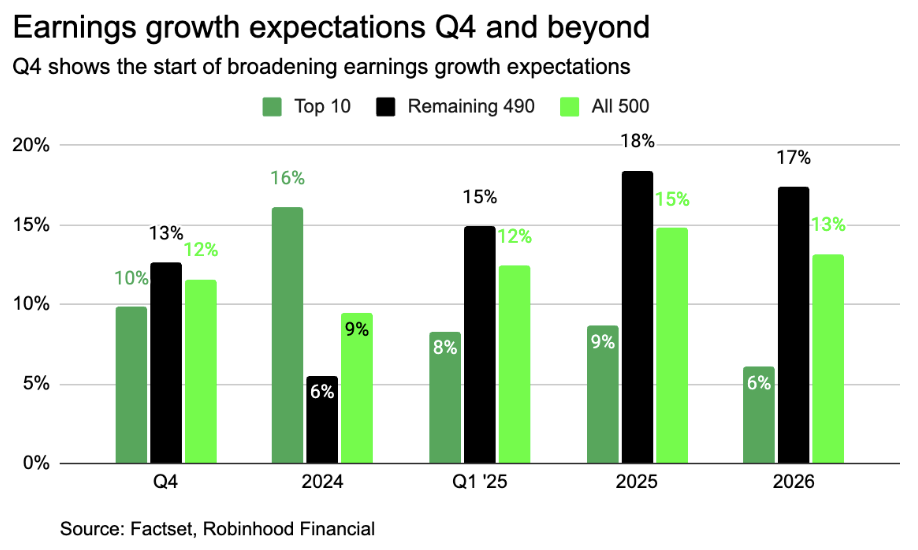

We believe current S&P 500 earnings growth expectations, which come to 15% in 2025 and 13% in 2026, as shown below, are reasonable. In particular, 2026 shows how the top 10 stocks by size are expected by the market to post only 6% earnings growth, in line with the 10 year average S&P earnings growth. This isn’t an overly optimistic expectation, especially considering additional productivity gains from AI. Note, these stocks make up 37% of the index, and have been dominant in returns the last two years.

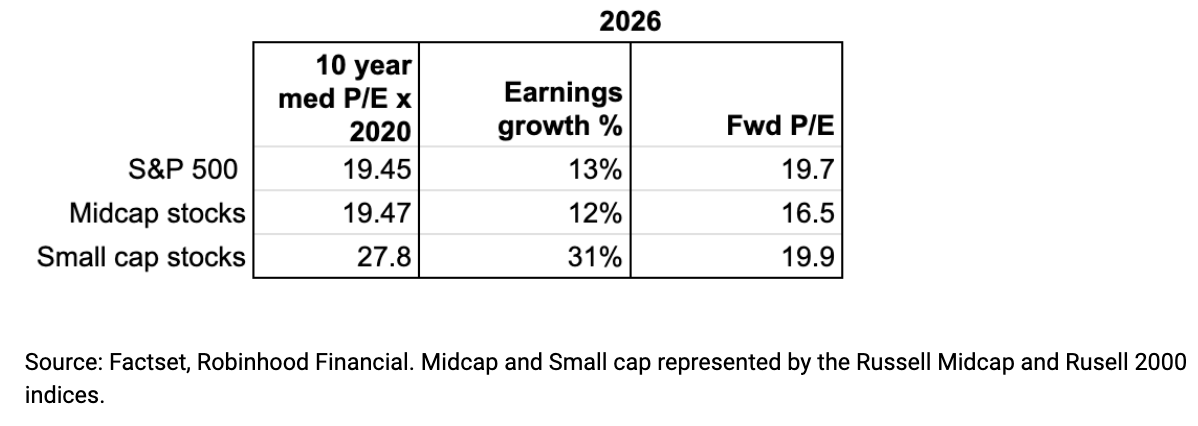

Building on this analysis, I expect the S&P to reach 6500 in 2025, and for mid-caps and small caps to post double-digit returns, of 20% plus – though we have greater confidence in mid-cap returns. I got here by applying the 10 year median P/E multiples (excluding the peak 2020 values), shown below, to 2026 expected earnings for each area. Valuation multiples for mid and small caps are much lower than their history—I believe returns in this space will come from both earnings growth and multiple expansion.

The preference for mid-caps over small caps comes from the lower average debt levels given a higher rate environment. Small caps have 27% more leverage than large caps on average, and 7% more than mid-caps.

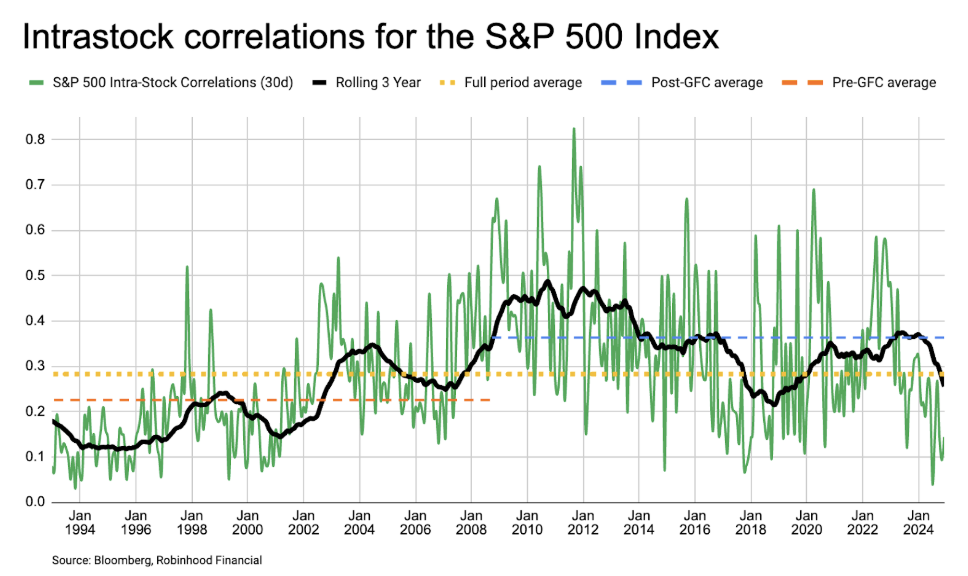

Different this time: stock specific fundamentals are in, large cap index investing is “fine.” With better valuations in mid-caps than large caps, a widening of earnings growth from the top 10, and elevated interest rates that ensure there is a cost to borrowing, large cap index investing alone will leave out opportunity. Company management decisions matter more now and there will be greater differentiation between stocks within sectors and industries. In fact, we’ve already gotten back to the pre-GFC era of lower S&P intrastock correlations; dropping from the post-GFC average of 0.38 -- to an average of 0.18 for the year, in line with the pre-GFC period range and supportive of stock specific fundamentals driving returns.

Peter Lynch famously said, “The person that turns over the most rocks wins the game.” I believe we’re in that environment now.

Of course, there are risks on the horizon–for both upside and downside directions.

Sentiment is currently high. At the end of 2023, the median 2024 S&P target from 14 major financial institutions was 4775 (4% returns at the time), with a range of 5100-4200 in the predictions, when the S&P was around 4600. Compare that to the same set of 14 for 2025, with a median target of 6600 (about 8.5% return as of this writing), with a range from 6500-7000. Not to mention, many are positive on small caps and assuming decent de-regulation. This is why my S&P 500 target isn’t higher at the moment—when the bar is high, there is less room for error.

The US deficit. Our deficit is at $1.9 trillion. According to the CBO, even with the expectation of Trump tax cuts of 2018 (TCJA) expiring over the next few years, the Federal deficit is expected to rise to $2.8 trillion by 2034.

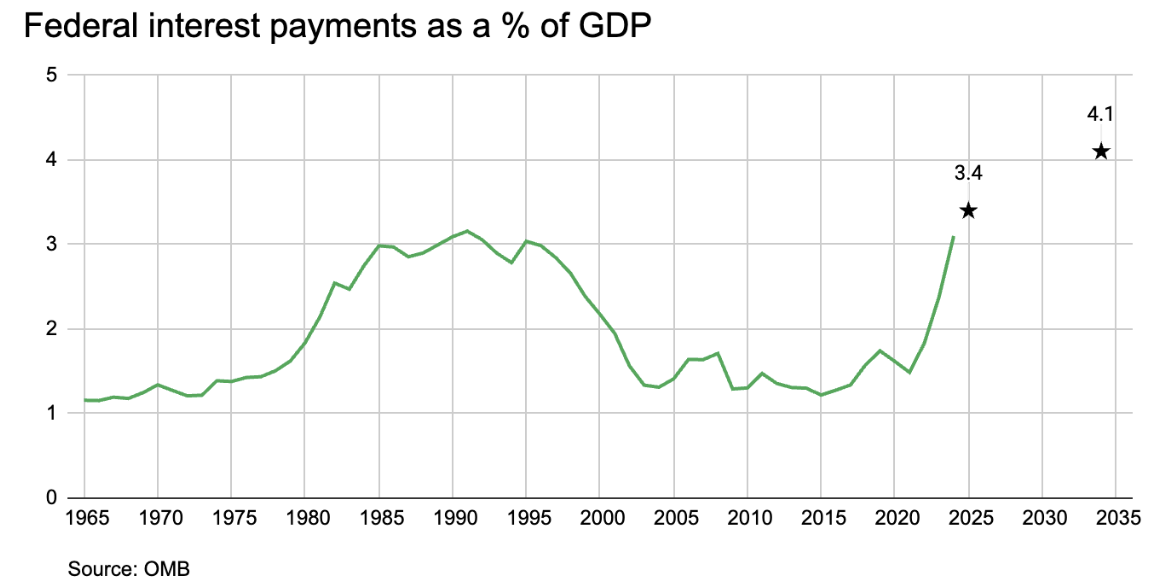

About half of government spending goes to Social Security, Medicare, and Medicaid. In addition, about $1 trillion, and rising, now goes to interest payments. As a % of GDP that is now about 3% and is estimated to rise to 4.1% by 2034 (as shown above). The last time interest payments were that high was in the 1980s and 1990s, when interest rates were practically double digits—and the bond vigilantes were out. In fact, recently, one of the largest bond shops said it would start reducing exposure to Treasuries in light of the fiscal issues.

This is why I expect it will be difficult to cut corporate taxes further (from 21% post the 2018 tax changes) or any other taxes for that matter. I also expect this could apply upward pressure to rates over the year, with risk to around 5% on the 10 year. Tariffs may be able to offset some of this, but that can only go so far before there are worse unintended consequences.

Inflation could move higher. It could happen for several reasons. If growth continues to move higher while the labor market remains strong, you could see inflation higher from increased demand for goods and services. On the other hand, inflation could also move higher from tariffs put in place under the new administration. According to the Yale Budget Lab, if tariffs were implemented as suggested by the Trump administration—broadly 10% on goods imports, with a 60% tariff on Chinese imports—“the level of consumer prices would rise by 1.4% to 5.1% before substitution. This would cost the equivalent of $1,900 to $7,600 per household in 2023 dollars.” If inflation were to rise, you would likely see the Fed reverse course, hiking rates.

Company cost-cutting increases to protect margins. According to the BLS, on average, wages account for around 70% of total employer costs. So, if companies decide that cutting costs is necessary to support profit margins, the labor market would likely soften. This is something to watch—if we get to 4.5% unemployment, I would start to rethink my calm view on the economy, but also expect lower Fed rates.

There are other possibilities to call out on the positive side as well—greater impacts from AI, a solution that moves towards a better federal budget balance and a drop in housing prices that improves the market for the better. We’ll cover these in the future. After all, it’s important to always maintain a mix of optimism and curiosity in investing. Otherwise the opportunities—and differences—can be too hard to spot.