Bonds: get in-the-know

Bonds: get in-the-know

You know that one friend you always learn something new from? Just when you think you are in-the-know, they tell you about the coolest type of insulated coffee mug, the newest kind of detergent (that apparently looks like a dryer sheet), or a slang word you didn’t know was on the rise. They know and share, and make you feel more in-the-know yourself. And, of course, your phone then shows you the things it hears you talking about with them, reinforcing the learning (thanks, Meta ads).

We try to give the same feeling in writing these — about things that may be less cool, but necessary, in the investing realm. We shared information about bonds in our piece Stocks are dripping, but have you heard of bonds?... and while it covered a lot of ground in the world of bonds, there’s more.

My team and I debate quite a bit about whether now is a good time to own investment-grade corporate bonds or high-yield bonds, and when preferreds make the most sense. We have also noticed the proliferation of other types of bond ETFs now available — such as CLOs and mortgage-backed securities. Each of them has unique attributes and risks.

First, what’s an investment grade bond? Well, many bonds are rated by one or more of three rating agencies — S&P, Moody’s, and/or Fitch. These rating agencies are paid for by issuers of bonds (aka the borrowers) to do some diligence to rate them. AAA or Aaa are the highest ratings, given to borrowers whom the agency believes have well-supported means to pay back their debt. The ratings continue down to AA, then A, and BBB. Anything BBB (in the case of S&P) or Baa (from Moody’s) or higher is considered investment grade. Below BBB is below investment grade, aka high-yield bonds, aka “junk bonds,” as they were known in the 1980s. So in general, the rating is supposed to measure the quality of a bond.

Size-wise, investment-grade bonds make up the largest part of the bond market, including treasuries, municipal bonds, and investment-grade corporate bonds.

Municipal bonds are issued by state and local governments, where the quality helps determine the rating and the yield. Different states and local governments have different budgets, which influence said quality. The one important difference with munis is that the yield earned when investing in them is almost always tax-free at the federal level — and if you invest in bonds issued by your own state, it can mean the income earned is fully tax-free. The yields often reflect this benefit, with even the highest quality munis typically offering lower yields than treasuries. This comparison between the yields of munis to treasuries is often used to measure whether a muni is an attractive investment.

Different from munis, investment-grade corporate bonds are issued by companies to borrow money. Their prices and related yields are based on some of the same factors as treasury bonds, such as time to maturity, but also the relative quality of the issuer. If an issuer is AAA rated, for example, the interest rate and yields will be similar to treasury bonds. But if an issuer is BBB, there will be a premium in the yield an investor earns relative to treasury bonds of the same maturity. That premium is often called a credit spread and reflects the additional credit risk (risk of ability to pay back).

Another type of bond that usually has even greater credit spreads is high-yield bonds. They are below investment grade, which often means the company carries greater-than-average debt relative to their assets. Their interest coverage ratios, which look at how much interest they pay on their debt, relative to their earnings before interest and taxes, is lower than investment-grade bonds. Thus, there is a greater risk of default when an investor buys these bonds (and thus a higher yield).

So one thing to consider when looking at high yield, is if the yield an investor earns makes up for the risk taken. These types of bonds tend to be correlated with stocks — when the economy is growing, they tend to appreciate because they may, in turn, become less risky because it’s easier for companies to earn more when the economy is growing. And while in general when interest rates go up, bond values fall (and vice versa), credit spreads can widen and narrow separately. Like right now, I think spreads are not wide enough (meaning high-yield bonds do not compensate enough for their risk).

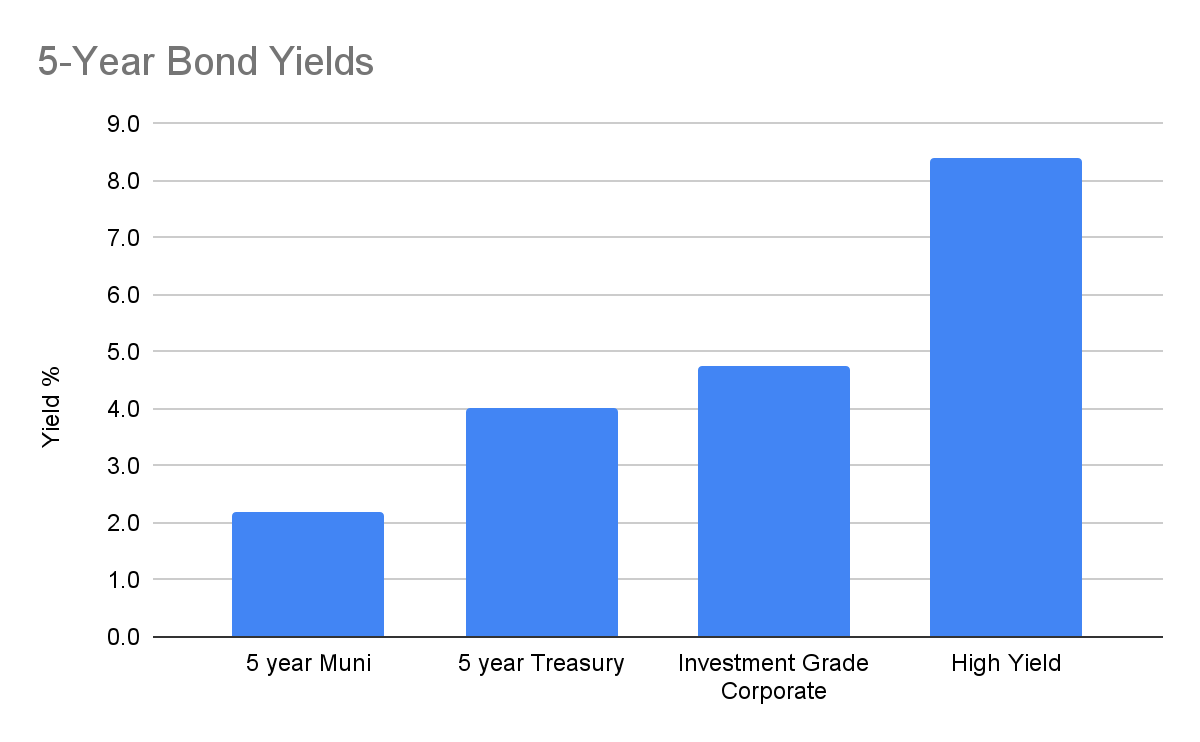

To illustrate all these points, here’s an outline of current example yields by type of bond (as of 02/14/2023) with the same maturity:

Like a lot of things, the longer something has been around, the more specialized it becomes. Bonds have been around for centuries (since the late 1600s), so people have come up with all kinds of variations to straight bonds. Some examples include:

Callable bonds: These can be issued by any kind of borrower and have a call option embedded in the bond, where the option is held by the borrower. It means the borrower can call the bonds earlier than maturity, usually at a predetermined date and price. Usually a callable bond has a premium in the yield (specifically, the yield-to-call) to compensate for giving away this option.

Putable bonds: These are the opposite, where the bond holder has the option to “put” the bonds back to the issuer, usually at a specific date and price. These are usually higher priced and thus carry a lower yield, all else equal.

Of course, bonds aren’t just backed by the revenues of governments (taxes) or companies (earnings). They can also be backed by other things:

Mortgage-backed securities (MBS) are backed by groups of mortgages, commercial and residential. They have unique characteristics, such as assumptions about repayment rates and underlying of the borrowers and can be further backed up by the US government through agencies such as Fannie Mae and Freddie Mac.

Collateralized loan obligations (CLO) are, sort of, bonds of bonds. CLOs use funds received from the issuance of debt (and equity) to acquire a diverse portfolio of typically hundreds of loans. So an investor would invest in the bonds issued by CLOs and the characteristics of these bonds would relate to one of a variety of tranches within the CLO from the underlying loans they invest in, each with a risk/return profile based on its seniority and claim priority on the cash flows produced by the underlying loan pool. Like other bonds, these tranches range from AAA to below investment grade (below BBB). Most of the underlying loans within the CLO are senior-secured loans, which means they have the first claim on all of the related company’s assets (in the event of a bankruptcy) and are intended to be the least risky investment in these companies (not to say the companies themselves are not risky). The loans typically carry floating-rate interest rates, which can be helpful in a rising rate environment (when the income rises with the rates) and less helpful in falling rate environments.

Preferreds are often known as hybrid securities. This is because they are bond-like investments with equity-like features, primarily issued by large banks and insurance companies. These securities are perpetual, meaning they have no maturity date or a very, very long one (like over 50 years) and are callable. They typically pay dividends instead of interest (so tax treatment may be different). In addition, they may offer multiple rate structures, meaning they start off with one dividend rate and at some point it changes. They can have investment-grade ratings, or below-investment grade but are always subordinated* in the capital structure. Some trade on an exchange like stocks (often around a price of $25 par value), while others trade more like bonds. Either way, they can be attractive depending on the rate you earn, the quality, the structure of the preferred, and your expectations of future interest rates.

See what I mean about more specialized aspects within the broader bond category? It can take time to absorb this all. But once you do, it can open a greater world of investment possibilities and even promote a better understanding of stock investing. Soon your bond knowledge will be bussin’ (also learned that word from that friend). *Subordinated refers to where a security sits in the capital structure of a company. In this case, the security is not first in line, but second, third, or later, in the event of a bankruptcy. Chart Source: Robinhood Financial, Bloomberg. Muni yield represented by the Bloomberg Muni 5 year yield, Treasury yield represented by the Bloomberg generic 5 year treasury yield, Investment Grade Corporate Bond yield represented by the yield on the CDX Investment Grade 5 year Index and High Yield Bond yield represented by the CDX High Yield 5 year Index. These are meant to be illustrative and not exact.