Truth: Retirement season

Truth: Retirement season

In 2010, two of my favorite hip-hop artists, Lil Wayne and Drake, released what I think is a timeless track together, “Right Above It.”

In true hip-hop fashion, it’s braggadocious. But to me, the song is about not caring what others think, and, importantly, keeping your crew to the people that are willing to hold up a mirror when you need the truth.

And the truth right now is, you need to save. Save save save.

I’ve talked about earnings season, which is in full swing now. Tomorrow is close to the biggest day of earnings reports by market cap, including Amazon, Apple, and Meta, which together make up over 12% of the S&P 500, amongst others.

But we are also in what I like to call retirement season, which is about doing something for your future.

Retirement season is during the first quarter of each year because of two things:

Until tax day, April 15th (or the 17th for those living in Maine or Massachusetts) this year, you can contribute up to $6500 to an Individual Retirement Account (IRA) for the 2023 year.

You can also contribute for 2024, where the limit is $500 higher than last year, at $7000.

That means that, if you are financially able and haven't done any of it yet, you can put up to $13,500 into an IRA for yourself this quarter.

That’s quite a bit of money at one time. So even if it’s less than that—whatever you can do now, for 2023, and later for 2024, and you keep doing it each year, retirement savings can add up. Doing it is the most important part.

Why?

Old-school benefits like social security are expected to be less and less funded over time—meaning what you could receive in the future is at risk due to government deficits (the government is borrowing $760B this quarter alone). More here.

The cost of things usually only increases over time. Saving and investing what you can now, could lead to a more independent future you.

There is a tax benefit to saving for retirement this way vs. just in a savings account, for example. Whether it’s a potential upfront tax deduction against your income through a contribution to a traditional IRA or simply that earnings from funds in an IRA, while invested, are not subject to taxes, investments can grow without worrying about having to pay taxes on that growth .

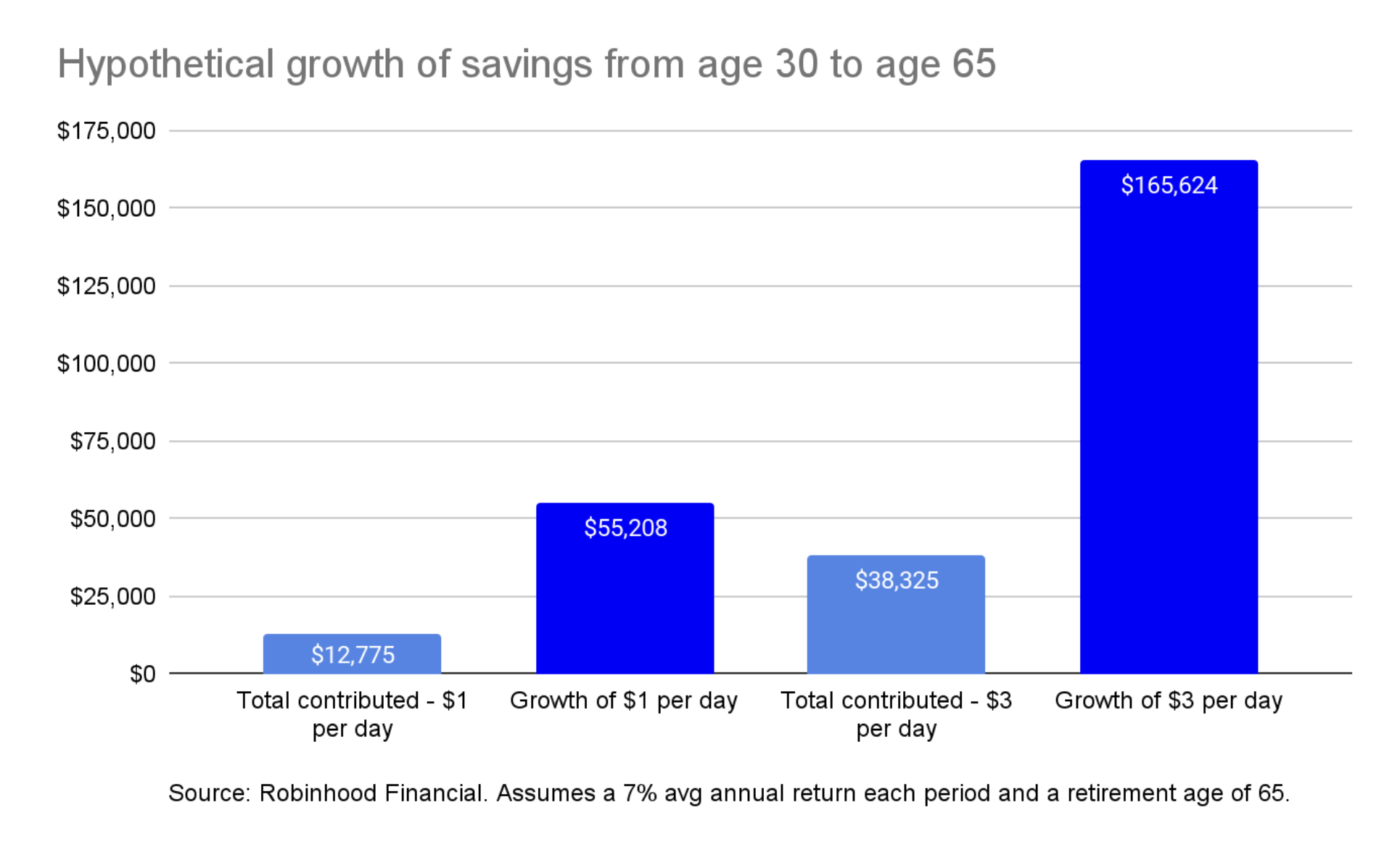

Saving the equivalent of just $1 per day into an IRA, and making sure it gets invested in a diversified way, can help reach a more relaxed retirement. In our analysis below, investing $1 per day and $3 per day from the age of 30, earning a reasonable 7% return along the way, should grow retirement savings. While this doesn’t take into account how returns can swing from year to year, it’s a decent proxy for a median outcome over time.

Can or should you still contribute to an IRA if you already have a 401k? YES. If you have both and can contribute to both each year, it’s a good idea. No need to choose between them—one doesn’t preclude you from doing the other. And more retirement savings can’t be bad.

Like the intention of that hip-hop song, the truth is we all need to save more. So, I’m making this the first of a three-part series during this retirement season, in the hopes there’s a little more truth and motivation for future you.