This earnings season outlook

This earnings season outlook

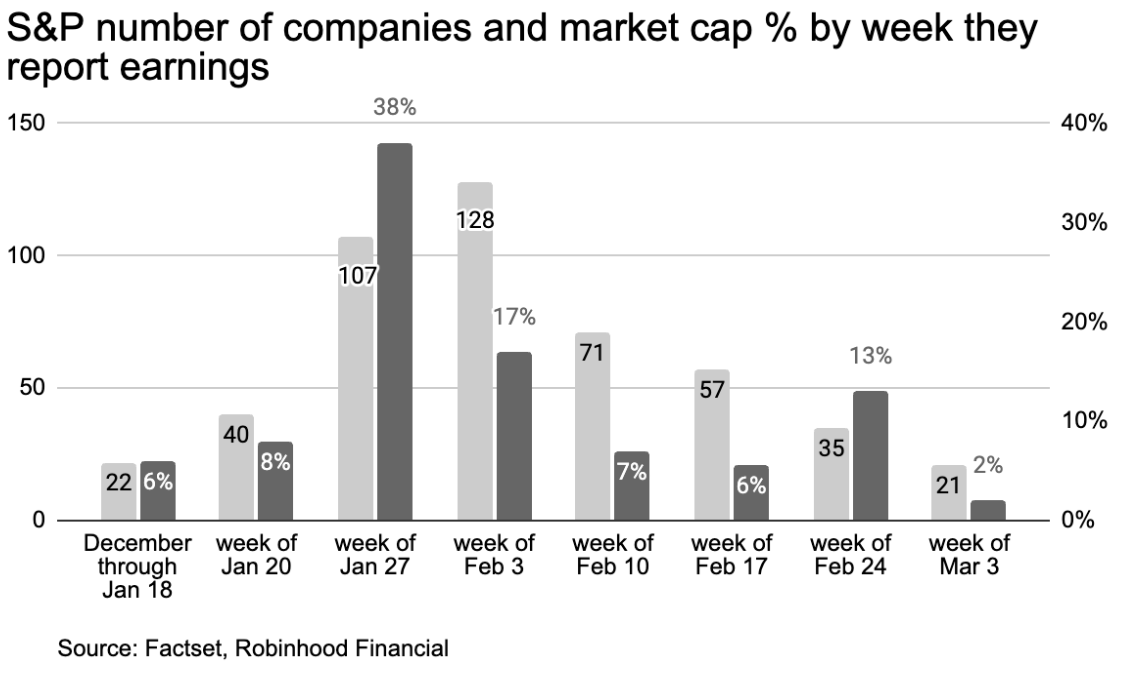

Earnings season is here. 4 times a year we, as investors, are hit with a flood of information from companies, starting a couple weeks after each quarter end and lasting for several weeks. But the stream is not consistent. In fact, next week and the one after, combined, will deliver earnings reports from over 50% of the S&P 500 companies by market cap (while the week of 2/24 is pretty impactful as well).

For context, the week of January 27th is the biggest week, and will include the likes of Apple, Amazon, Microsoft, Tesla and Meta. The following week includes Google and Eli Lilly, and the week of February 24th will give us earnings updates from Nvidia and Broadcom.

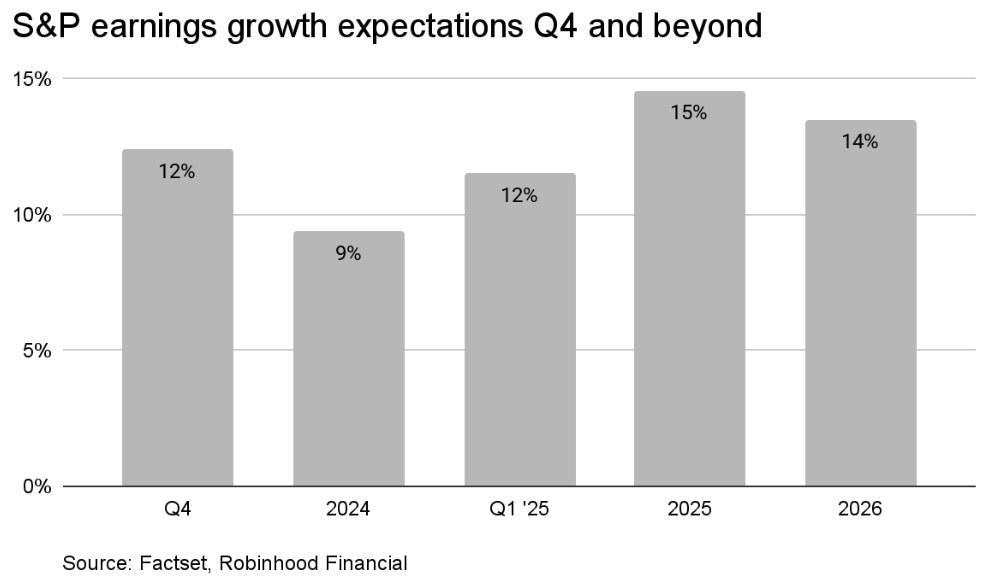

S&P 500 earnings growth for Q4 2024 is expected to come in at 12%, bringing the full year 2024 growth to 9%. Only about 10% of the companies have reported, mostly from banks, so it’s still really early—but it is currently tracking above expectations at 12.4%.

This double digit earnings growth is expected to continue for 2025 and 2026.

Beyond financials, several sectors are expected to post strong earnings growth:

Communication Services, Information Technology, and Utilities are all projected to have solid quarters.

Healthcare and Consumer Discretionary show growth, but it’s concentrated. In Healthcare, growth is mainly driven by pharmaceuticals. For Consumer Discretionary, the numbers rely heavily on Amazon—without it, growth would be flat, and if you remove automobiles, growth for the sector turns negative.

On the negative side, Materials and Energy are expected to drag overall earnings growth down. These sectors are heavily tied to global markets, so despite a decent U.S. economy, weaker demand in China and persistently challenging economic conditions in Europe are expected to keep earnings muted.

Looking through the expectations by name, the magnificent 7 is not expected to be the only game in town, like it might have been in the past.

Only 3 of the 7—NVIDIA, Amazon, and Alphabet—are among the top 10 contributors to overall S&P 500 earnings growth. The remaining contributors are Truist, Bank of America, Citigroup, JPMorgan Chase, Merck & Co., Micron Technology, and Eli Lilly.

On the bottom of the list are Exxon Mobil, Chevron, Intel, CVS, Marathon Petroleum, Philips 66, Moderna, Valero Energy, Chubb, and Everest Group.

However, expectations are everything in investing. The higher the expectations for a company, the better the actual earnings report has to be. The opposite can be true for companies that are already expected to post poor results. Many times, even a whiff of a turnaround or improvement can boost the stock price’s reaction. Of course, earnings aren’t the only thing to consider on the horizon. President Trump is already rolling out policies that can have both short and long term impacts. Congress will soon need to address the federal budget (again) as well as the deficit. Finally, interest rate policy is still a factor. The next Fed meeting on January 29th, will be closely watched given how much expectations have swung.

While earnings season is important, the balance between earnings, rates and policy will certainly shape overall outcomes for 2025.